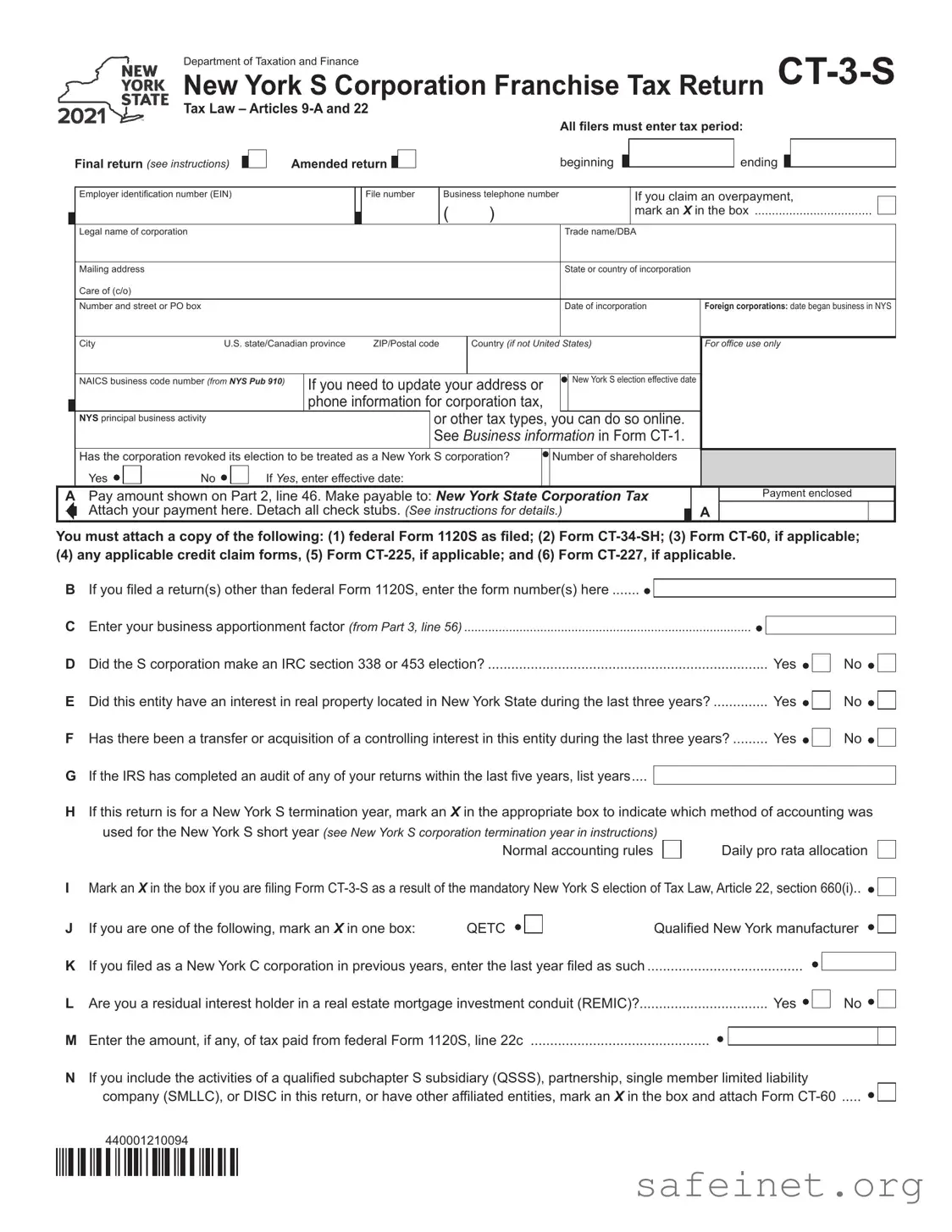

The CT-3-S form is a crucial document for S corporations operating in New York State, serving as the Franchise Tax Return for these entities. This form is essential for reporting the corporation's income, deductions, and credits, and it ensures compliance with New York tax laws as outlined in Articles 9-A and 22. When completing the CT-3-S, filers must provide key information, such as the tax period, employer identification number (EIN), and the legal name of the corporation. The form also requires details about the corporation's incorporation, mailing address, and the number of shareholders. Notably, if an overpayment is claimed, the form includes a specific section for marking this request. Additionally, corporations must attach supporting documents, including federal Form 1120S, to substantiate their claims. The CT-3-S also features sections for tax computation, including New York receipts and any applicable credits. Understanding how to accurately fill out this form is vital for S corporations to avoid penalties and ensure they meet their tax obligations effectively.

| Fact Name | Description |

|---|---|

| Form Purpose | The CT-3-S form is used by S corporations in New York to report franchise taxes. |

| Governing Laws | This form is governed by New York Tax Law, specifically Articles 9-A and 22. |

| Filing Requirements | All filers must indicate their tax period and whether the return is final or amended. |

| Identification Numbers | Corporations must provide their Employer Identification Number (EIN) and file number. |

| Documentation Needed | Filers must attach several documents, including federal Form 1120S and Form CT-34-SH. |

| Shareholder Information | The form requires information about the number of shareholders and any revocation of S corporation status. |

| Payment Instructions | If taxes are due, the form includes instructions for payment and where to attach checks. |

Completing the CT-3-S form is a critical step for New York S Corporations to ensure compliance with state tax regulations. After filling out the form, you will need to submit it along with any required attachments and payments to the appropriate tax authority. Below are the detailed steps to guide you through the process of filling out the CT-3-S form accurately.

What is the CT-3-S form?

The CT-3-S form is the New York S Corporation Franchise Tax Return. It is used by S corporations operating in New York State to report their income, calculate taxes owed, and claim any applicable credits. This form must be filed annually and includes important information about the corporation's financial activities during the tax year.

Who needs to file the CT-3-S form?

Any corporation that has elected to be treated as an S corporation under New York State law must file the CT-3-S form. This includes domestic corporations as well as foreign corporations doing business in New York. If the corporation has revoked its S election, it must indicate this on the form and may need to file a different tax return.

What information is required on the CT-3-S form?

The form requires several key pieces of information, including the corporation's legal name, trade name, mailing address, employer identification number (EIN), and the dates of the tax period. Additionally, it requires financial details such as income, deductions, and any applicable tax credits. Corporations must also attach a copy of their federal Form 1120S and other relevant documents.

How is the tax calculated on the CT-3-S form?

The tax owed is determined by calculating the New York receipts and applying the fixed dollar minimum tax, along with any recapture of tax credits. Corporations must complete the computation sections to arrive at the total tax due. If there are any overpayments, they can be credited to the next period or refunded.

What are the deadlines for filing the CT-3-S form?

The CT-3-S form is typically due on the 15th day of the third month following the end of the corporation's tax year. For corporations following a calendar year, this means the deadline is March 15. It is important to file on time to avoid late penalties and interest on any taxes owed.

What if the corporation needs to amend its CT-3-S form?

If a corporation discovers errors after filing the CT-3-S form, it can file an amended return. This involves marking the appropriate box on the form and providing the corrected information. It is essential to submit the amended return as soon as possible to rectify any discrepancies and minimize potential penalties.

Can a corporation claim credits on the CT-3-S form?

Yes, the CT-3-S form allows corporations to claim various tax credits, such as the special additional mortgage recording tax credit. Corporations must follow the instructions for claiming these credits and attach any necessary forms to support their claims. Proper documentation is crucial for ensuring that credits are accurately applied.

Incorrect EIN: Entering an invalid or incorrect Employer Identification Number (EIN) can lead to significant delays in processing your return.

Missing Signatures: Failing to sign the form can result in rejection. Ensure that all required signatures are provided.

Omitting Required Attachments: Not including necessary documents, such as federal Form 1120S or Form CT-34-SH, may lead to processing issues.

Incorrect Tax Period: Selecting the wrong tax period can cause confusion. Double-check the dates before submission.

Errors in Financial Information: Inputting incorrect figures for income or deductions can lead to miscalculations. Review all numbers carefully.

Neglecting to Indicate Amended Returns: If you are submitting an amended return, make sure to mark the appropriate box. This is crucial for correct processing.

Ignoring Instructions: Not following the specific instructions provided for each section can result in incomplete or inaccurate submissions. Always refer to the guidelines.

The CT-3-S form is an essential document for New York S corporations to report their franchise tax. Along with this form, several other documents may be required to ensure compliance and accurate reporting. Below is a list of commonly used forms and documents that often accompany the CT-3-S.

Ensuring that these documents are completed accurately and submitted on time can help avoid potential penalties and ensure compliance with New York tax laws. Always check for the latest requirements and consult with a tax professional if needed.

The CT-3-S form is similar to the IRS Form 1120S, which is the U.S. Income Tax Return for an S Corporation. Both forms are used by S corporations to report income, deductions, and credits to the IRS and state tax authorities. They require similar information, such as shareholder details, income sources, and tax calculations. The CT-3-S, however, specifically addresses New York State tax requirements, while the 1120S focuses on federal obligations.

Another related document is the CT-34-SH, which is the New York S Corporation Shareholder’s Information Schedule. This form is used to report each shareholder's share of the corporation’s income, deductions, and credits. Both the CT-3-S and CT-34-SH work together to ensure accurate reporting of S corporation income and its distribution among shareholders. While the CT-3-S provides the overall tax return for the corporation, the CT-34-S details the tax implications for individual shareholders.

The CT-60 form, known as the New York State Corporation Tax Credit Form, is also similar. It is used to claim various tax credits available to corporations in New York. Like the CT-3-S, the CT-60 requires detailed information about the corporation’s financial activities. The CT-3-S may reference the CT-60 when calculating tax credits that affect the overall tax liability of the S corporation.

The CT-225 form, which is the New York State Investment Tax Credit Claim Form, shares similarities with the CT-3-S as it pertains to tax credits. This form is specifically for claiming investment tax credits. Both forms require accurate financial data and calculations to determine the correct tax obligations. The CT-3-S may include information from the CT-225 if the corporation is eligible for investment credits.

Form CT-227, the New York State Voluntary Contributions Form, is another document related to the CT-3-S. It is used to report voluntary contributions made by the corporation to specific funds. Both forms require details about the corporation’s financial activities and the amounts involved. The CT-3-S will reference any contributions reported on the CT-227 when determining the overall tax liability.

The CT-400 form is the New York State Estimated Tax for Corporations. This document is similar in that it is used by corporations to report estimated tax payments. Both the CT-3-S and CT-400 require information on the corporation’s income and tax calculations. While the CT-3-S is a final tax return, the CT-400 is used throughout the year to manage estimated tax obligations.

Lastly, the Form CT-1, which is the New York State Corporation Tax Return, is related to the CT-3-S. This form is used for corporations that do not qualify as S corporations. While the CT-3-S is specific to S corporations and their unique tax treatment, both forms involve similar types of financial reporting and tax calculations, making them comparable in terms of structure and purpose.

When filling out the CT-3-S form, there are several important practices to keep in mind. Below is a list of things you should do and avoid to ensure accurate completion.

This form is designed for all New York S corporations, regardless of size. Small businesses can also benefit from using this form to report their taxes.

In New York, S corporations are required to file the CT-3-S form annually, just like C corporations must file their respective forms.

While S corporations may have different tax obligations, they are not entirely exempt from franchise tax. They may still owe a minimum tax based on their New York receipts.

Although both forms are related to S corporations, the CT-3-S is specific to New York state tax requirements, while the 1120S is for federal tax purposes.

It is mandatory to attach specific documents, such as the federal Form 1120S and other relevant forms, when filing the CT-3-S.

There are specific deadlines for filing the CT-3-S, typically aligned with the corporation's tax year. Missing these deadlines can result in penalties.

If there are errors or changes needed after submission, corporations can file an amended CT-3-S to correct any issues.

Here are some important points to keep in mind when filling out and using the CT-3-S form for New York S Corporation Franchise Tax Return: