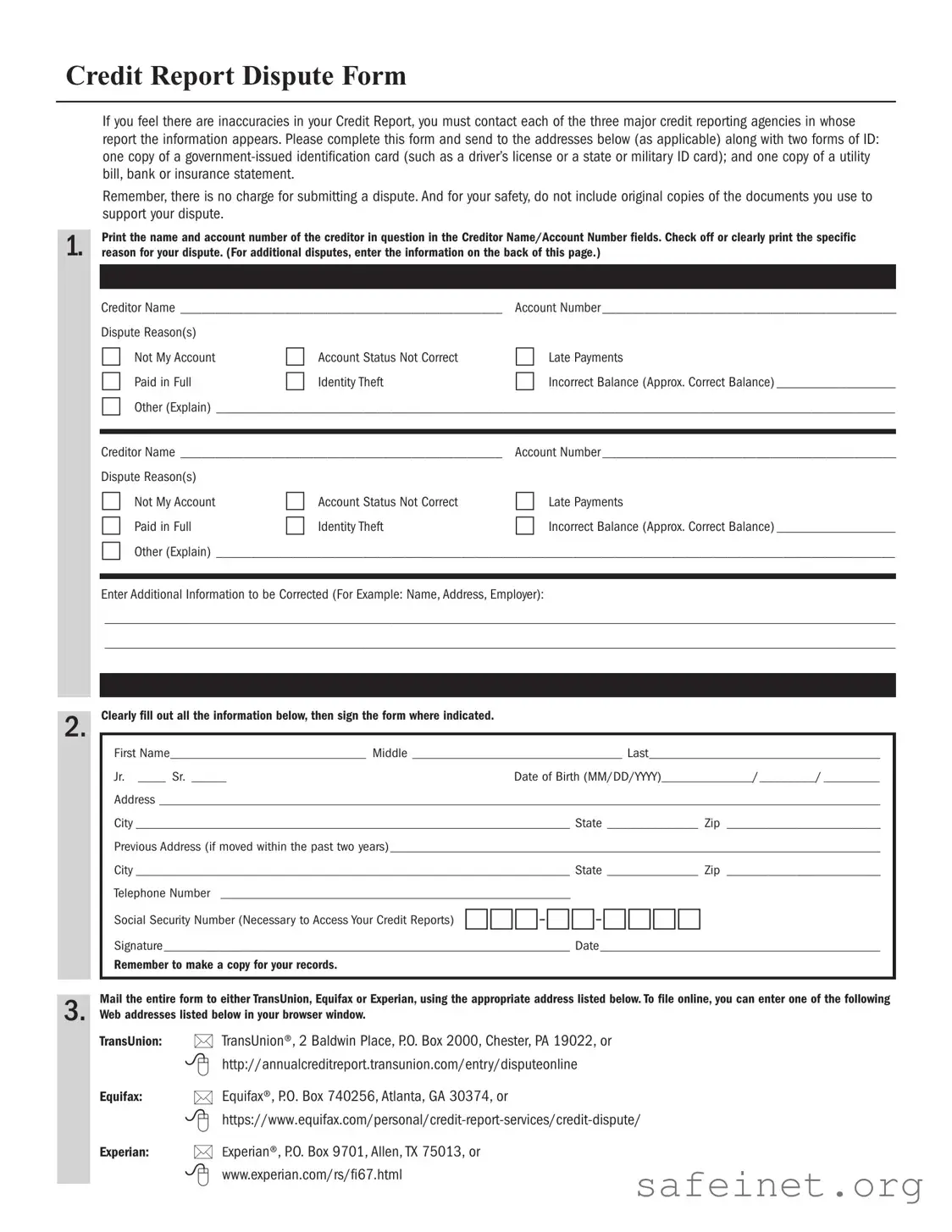

The Credit Report Dispute form serves as a vital tool for individuals seeking to address inaccuracies in their credit reports. This form allows consumers to formally challenge errors that may negatively impact their credit scores and financial health. Typically, the form requires personal identification details, including the consumer’s name, address, and Social Security number, to ensure accurate processing. Additionally, it prompts individuals to specify the disputed items, providing space for a detailed explanation of the inaccuracies. Supporting documentation may also be included to substantiate claims. By submitting this form to credit reporting agencies, consumers initiate a process that can lead to corrections and improved credit standings. Understanding the components and proper usage of the Credit Report Dispute form is essential for anyone looking to maintain a fair and accurate credit history.

| Fact Name | Details |

|---|---|

| Purpose | The Credit Report Dispute form is used to challenge inaccuracies on your credit report. |

| Who Can Use It | Consumers who believe their credit report contains errors can file a dispute using this form. |

| Filing Process | The form can typically be submitted online, by mail, or over the phone, depending on the credit reporting agency. |

| Required Information | Personal identification details, a description of the dispute, and supporting documentation may be required. |

| Response Time | Credit reporting agencies are generally required to investigate disputes within 30 days of receiving the form. |

| State-Specific Forms | Some states have specific forms or additional requirements; check local regulations for details. |

| Governing Laws | The Fair Credit Reporting Act (FCRA) governs the process of disputing errors on credit reports. |

| Impact on Credit Score | Filing a dispute does not affect your credit score, but the outcome may influence it. |

| Documentation | It’s important to keep copies of all documents submitted with your dispute for your records. |

| Follow-Up | If the dispute is resolved in your favor, the credit reporting agency must provide you with an updated credit report. |

Once you have the Credit Report Dispute form in hand, it’s time to fill it out accurately. This process will help you address any inaccuracies in your credit report. Follow these steps to ensure your dispute is clear and effective.

Once you’ve submitted your dispute, the credit reporting agency will investigate the matter. They typically have 30 days to respond. Keep an eye on your mail or email for updates regarding your dispute.

What is a Credit Report Dispute form?

A Credit Report Dispute form is a document you can use to challenge inaccuracies or errors on your credit report. If you notice incorrect information, such as wrong account details or outdated entries, this form helps you formally request a correction from the credit reporting agency.

How do I obtain a Credit Report Dispute form?

You can typically find the Credit Report Dispute form on the websites of major credit reporting agencies like Experian, TransUnion, and Equifax. They often provide an online version that you can fill out directly, or you can download a printable form if you prefer to submit it by mail.

What information do I need to provide on the form?

When filling out the form, include your personal information such as your name, address, and Social Security number. Clearly identify the specific items you are disputing and provide any supporting documentation that backs up your claim. This could include bank statements, letters, or any other relevant evidence.

How long does it take to resolve a dispute?

Once you submit your dispute, the credit reporting agency typically has 30 days to investigate. They will contact the creditor to verify the information. After the investigation, you should receive a response detailing the outcome of your dispute. If changes are made, you’ll get an updated credit report.

What happens if my dispute is not resolved in my favor?

If your dispute is not resolved in your favor, you have the right to add a statement to your credit report explaining your position. This statement will be included in your report, which can help potential lenders understand your side of the story when they review your credit history.

Can I dispute more than one item at a time?

Yes, you can dispute multiple items on the same form. However, it may be more effective to submit separate disputes for each item. This way, you can provide specific details and supporting documents for each issue, which can help ensure a thorough investigation.

Not Providing Sufficient Information: Many individuals fail to include all necessary details when filling out the dispute form. This can lead to delays or even rejection of the dispute. Always ensure that you include your full name, address, Social Security number, and any relevant account numbers.

Using Vague Language: It's common for people to describe their disputes in a general way. Instead of saying "this is wrong," specify what is wrong and why. Clear and detailed explanations help the credit bureau understand the issue better.

Neglecting to Include Supporting Documentation: Supporting documents can significantly strengthen your case. Failing to attach proof, such as payment receipts or correspondence with creditors, may weaken your dispute.

Submitting Multiple Disputes for the Same Issue: Some individuals mistakenly submit several disputes for the same error. This can confuse the credit bureau and may result in delays. It’s best to consolidate your concerns into a single, comprehensive dispute.

Ignoring Deadlines: Timeliness is crucial in the dispute process. Some people overlook the deadlines for submitting disputes. Always check the relevant timelines to ensure your dispute is filed promptly.

When disputing information on a credit report, several other forms and documents may be necessary to support your claim. These documents can help clarify your position and provide additional evidence to the credit reporting agency. Below is a list of commonly used forms and documents in conjunction with the Credit Report Dispute form.

Gathering these documents can enhance the effectiveness of your dispute. Each piece of evidence plays a crucial role in building a strong case for correcting inaccuracies on your credit report.

The Credit Report Dispute form is similar to a Consumer Complaint form. Both documents allow individuals to voice concerns about inaccuracies or unfair treatment. A Consumer Complaint form typically addresses issues with products or services, while the Credit Report Dispute form focuses specifically on errors in credit reporting. Each form serves as a tool for consumers to seek resolution and ensure their rights are upheld.

Another document similar to the Credit Report Dispute form is the Identity Theft Affidavit. This affidavit is used when someone’s personal information has been misused, affecting their credit report. Like the dispute form, it requires detailed information about the fraudulent activity and aims to rectify the inaccuracies. Both documents empower consumers to take action against unauthorized actions that harm their credit standing.

The Fair Credit Reporting Act (FCRA) Request for Information is also akin to the Credit Report Dispute form. This request is made when a consumer seeks clarification on their credit report. While the dispute form challenges specific entries, the FCRA request focuses on obtaining more information about the report itself. Both documents are essential for consumers wanting to understand and correct their credit history.

The Request for Credit Report form shares similarities with the Credit Report Dispute form as well. This document is used to obtain a copy of one’s credit report, which is necessary before disputing any inaccuracies. Both forms are part of the process of managing one’s credit health, allowing consumers to stay informed and take necessary actions based on their findings.

Lastly, the Debt Validation Letter is comparable to the Credit Report Dispute form. When a consumer receives a collection notice, they can send a Debt Validation Letter to request proof of the debt. This letter serves to ensure that the debt is legitimate, much like how the dispute form ensures that the credit report is accurate. Both documents protect consumer rights and help maintain financial integrity.

When filling out a Credit Report Dispute form, it’s crucial to approach the process carefully to ensure your concerns are addressed effectively. Here’s a list of things you should and shouldn’t do:

By following these guidelines, you can improve the chances of a successful dispute and ensure your credit report accurately reflects your financial history.

Understanding the Credit Report Dispute form is essential for anyone looking to correct inaccuracies in their credit report. However, several misconceptions can lead to confusion. Here are eight common misunderstandings about the form:

Many people believe that only significant mistakes warrant a dispute. In reality, even minor inaccuracies can affect your credit score and should be corrected.

This is false. Filing a dispute using the Credit Report Dispute form is free. Consumers are entitled to challenge errors without incurring any costs.

While a dispute can lead to corrections, it does not guarantee that the disputed item will be removed. The credit reporting agency will investigate and make a determination based on the findings.

This misconception suggests that a single dispute is all you get. In fact, if new errors appear or if the initial dispute does not resolve the issue, you can file additional disputes.

While some disputes may take longer than others, the Fair Credit Reporting Act mandates that credit bureaus investigate disputes within 30 days. Many disputes are resolved much quicker.

This is not true. Individuals can file disputes on their own using the Credit Report Dispute form without needing legal assistance.

Consumers have the right to dispute inaccuracies. It is not limited to lenders or financial institutions. Individuals should actively monitor their credit reports and take action when necessary.

On the contrary, if you have more evidence or details to support your claim, you can submit that information during the dispute process.

By dispelling these misconceptions, individuals can better navigate the process of correcting their credit reports and ensure their financial health is accurately represented.

When filling out and using a Credit Report Dispute form, it’s important to keep several key points in mind to ensure a smooth process. Here are some essential takeaways:

By keeping these points in mind, you can navigate the dispute process more effectively and work towards correcting any inaccuracies in your credit report.