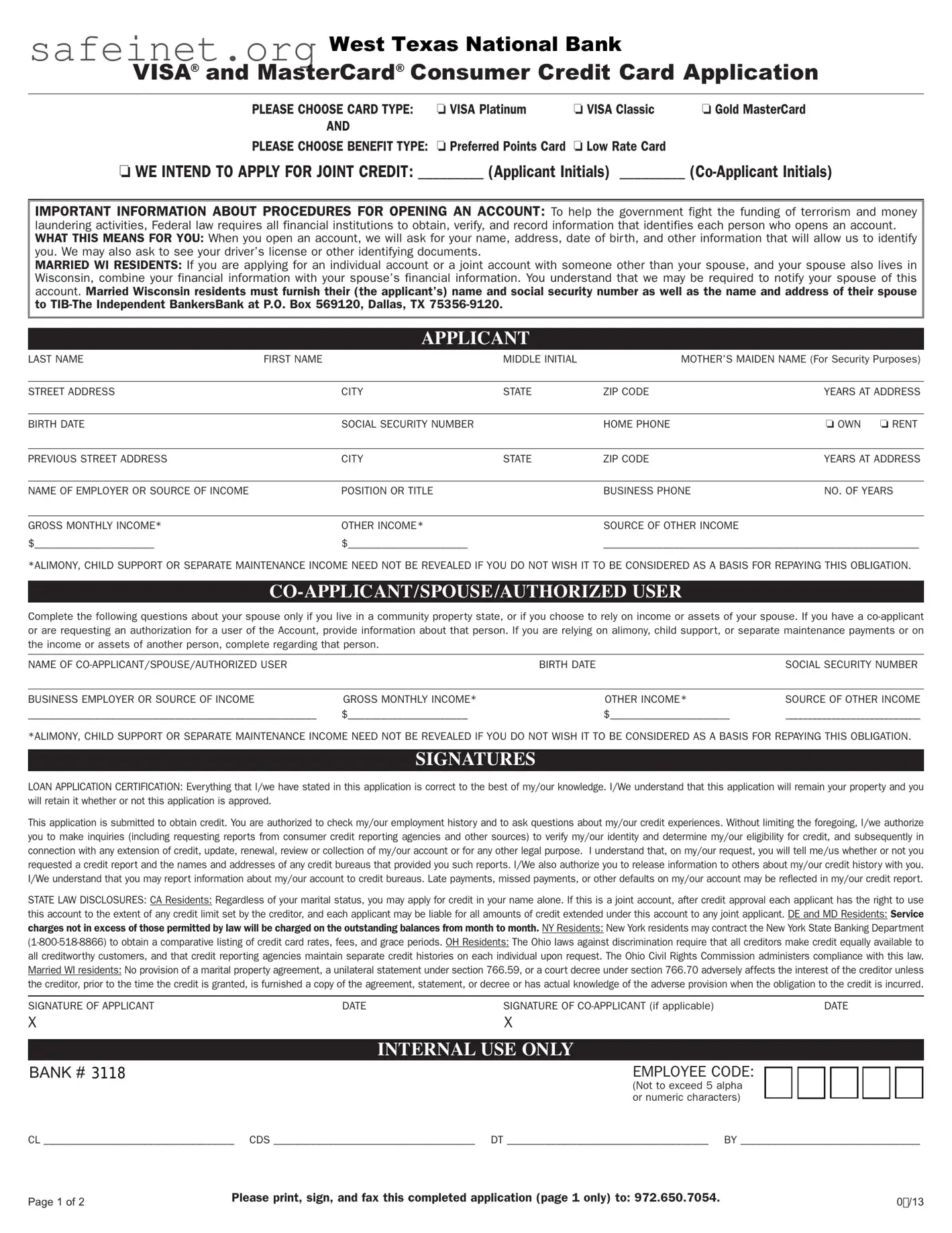

The Credit Card Application form is a crucial tool for those looking to secure a credit card. It requires applicants to select between various card types, such as VISA Platinum, VISA Classic, and Gold MasterCard, as well as benefits like Preferred Points or Low Rate Cards. Applicants must provide personal information including their names, addresses, social security numbers, and financial details, ensuring their identity and financial status are verified. For married residents of Wisconsin, additional information about spouses is mandated, further intertwining personal financial information. Furthermore, the form informs applicants that federal laws require banks to verify identities to combat money laundering and terrorism financing. This includes the possibility of presenting identification documents like a driver's license. The application underscores the importance of accurate information, noting that all stated details must be true to the best of the applicant's knowledge. It also includes crucial state-specific disclosures regarding credit application rights and responsibilities. Understanding these components not only facilitates a smoother application process but also equips individuals with the knowledge needed to make informed financial decisions.

VISA and MasterCardWest TexasConsumerNationalCreditBankCard Application

®®

|

|

|

|

PLEASE CHOOSE CARD TYPE: |

❏ VISA Platinum |

❏ VISA Classic |

❏ Gold MasterCard |

AND

PLEASE CHOOSE BENEFIT TYPE: ❏ Preferred Points Card ❏ Low Rate Card

❏WE INTEND TO APPLY FOR JOINT CREDIT: _________ (Applicant Initials) _________

IMPORTANT INFORMATION ABOUT PROCEDURES FOR OPENING AN ACCOUNT: To help the government fight the funding of terrorism and money laundering activities, Federal law requires all financial institutions to obtain, verify, and record information that identifies each person who opens an account. WHAT THIS MEANS FOR YOU: When you open an account, we will ask for your name, address, date of birth, and other information that will allow us to identify you. We may also ask to see your driver’s license or other identifying documents.

MARRIED WI RESIDENTS: If you are applying for an individual account or a joint account with someone other than your spouse, and your spouse also lives in Wisconsin, combine your financial information with your spouse’s financial information. You understand that we may be required to notify your spouse of this

account. Married Wisconsin residents must furnish their (the applicant’s) name and social security number as well as the name and address of their spouse to

LAST NAME |

FIRST NAME |

|

MIDDLE INITIAL |

MOTHER’S MAIDEN NAME (For Security Purposes) |

|

|

|

|

|

|

|

STREET ADDRESS |

|

CITY |

STATE |

ZIP CODE |

YEARS AT ADDRESS |

|

|

|

|

|

|

BIRTH DATE |

|

SOCIAL SECURITY NUMBER |

|

HOME PHONE |

❏ OWN ❏ RENT |

|

|

|

|

|

|

PREVIOUS STREET ADDRESS |

|

CITY |

STATE |

ZIP CODE |

YEARS AT ADDRESS |

|

|

|

|

|

|

NAME OF EMPLOYER OR SOURCE OF INCOME |

|

POSITION OR TITLE |

|

BUSINESS PHONE |

NO. OF YEARS |

|

|

|

|

|

|

GROSS MONTHLY INCOME* |

|

OTHER INCOME* |

|

SOURCE OF OTHER INCOME |

|

$______________________ |

|

$______________________ |

|

__________________________________________________________ |

|

*ALIMONY, CHILD SUPPORT OR SEPARATE

Complete the following questions about your spouse only if you live in a community property state, or if you choose to rely on income or assets of your spouse. If you have a

NAME OF |

|

BIRTH DATE |

SOCIAL SECURITY NUMBER |

|

|

|

|

BUSINESS EMPLOYER OR SOURCE OF INCOME |

GROSS MONTHLY INCOME* |

OTHER INCOME* |

SOURCE OF OTHER INCOME |

_____________________________________________________ |

$______________________ |

$______________________ |

____________________________ |

|

SIGNATURES |

|

|

*ALIMONY, CHILD SUPPORT OR SEPARATE MAINTENANCE INCOME NEED NOT BE REVEALED IF YOU DO NOT WISH IT TO BE CONSIDERED AS A BASIS FOR REPAYING THIS OBLIGATION.

LOAN APPLICATION CERTIFICATION: Everything that I/we have stated in this application is correct to the best of my/our knowledge. I/We understand that this application will remain your property and you will retain it whether or not this application is approved.

This application is submitted to obtain credit. You are authorized to check my/our employment history and to ask questions about my/our credit experiences. Without limiting the foregoing, I/we authorize you to make inquiries (including requesting reports from consumer credit reporting agencies and other sources) to verify my/our identity and determine my/our eligibility for credit, and subsequently in connection with any extension of credit, update, renewal, review or collection of my/our account or for any other legal purpose. I understand that, on my/our request, you will tell me/us whether or not you requested a credit report and the names and addresses of any credit bureaus that provided you such reports. I/We also authorize you to release information to others about my/our credit history with you. I/We understand that you may report information about my/our account to credit bureaus. Late payments, missed payments, or other defaults on my/our account may be reflected in my/our credit report.

STATE LAW DISCLOSURES: CA Residents: Regardless of your marital status, you may apply for credit in your name alone. If this is a joint account, after credit approval each applicant has the right to use

this account to the extent of any credit limit set by the creditor, and each applicant may be liable for all amounts of credit extended under this account to any joint applicant. DE and MD Residents: Service

charges not in excess of those permitted by law will be charged on the outstanding balances from month to month. NY Residents: New York residents may contract the New York State Banking Department

SIGNATURE OF APPLICANT |

|

DATE |

|

SIGNATURE OF |

|

|

|

|

DATE |

|||||

X |

|

|

|

X |

|

|

|

|

|

|

|

|

|

|

BANK # 3118 |

|

|

INTERNAL USE ONLY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EMPLOYEE CODE: |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

(Not to exceed 5 alpha |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

or numeric characters) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

CL ___________________________________ |

CDS _____________________________________ |

DT _____________________________________ |

BY _________________________________ |

|||||||||||

Page 1 of 2 |

Please print, sign, and fax this completed application (page 1 only) to: 972.650.7054. |

0/13 |

||||||||||||

|

|

|

|

|||||||||||

VISA® and MasterCard® Consumer Credit Card Application

|

PREFERRED POINTS CARD |

|

LOW RATE CARD |

|

|

|

|

|

|

Interest Rates and Interest Charges |

|

|

||

|

|

|

|

|

|

2.90% introductory APR for six months. |

|

2.90% introductory APR for six months. |

|

Annual Percentage Rate |

After that, your APR will be 15.24%. |

|

After that, your APR will be 10.24%. |

|

(APR) for Purchases |

|

|||

|

This APR will vary with the market based on |

|

This APR will vary with the market based on |

|

|

the Prime Rate.a |

|

the Prime Rate.b |

|

|

2.90% introductory APR for six months. |

|

2.90% introductory APR for six months. |

|

APR for Balance Transfers |

After that, your APR will be 15.24%. |

|

After that, your APR will be 10.24%. |

|

and Cash Advances |

|

|||

This APR will vary with the market based on |

|

This APR will vary with the market based on |

||

|

the Prime Rate.a |

|

the Prime Rate.b |

|

Penalty APR and |

19.24% – This APR will vary with the market based on the Prime Rate.c |

|||

This APR may be applied if you allow your Account to become 60 days past due. |

||||

When It Applies |

How Long Will the Penalty Apply? If your APR is increased for the reason stated above, the |

|||

|

Penalty APR will apply until you make three consecutive minimum payments when due. |

|||

|

|

|

||

How to Avoid Paying Interest |

Your due date is at least 25 days after the close of each billing cycle. We will not charge you |

|||

on Purchases |

any interest on purchases if you pay your entire balance by the due date each month. |

|||

|

|

|

|

|

For Credit Card Tips from |

To learn more about factors to consider when |

applying for or using a credit card, visit the website |

||

the Consumer Financial |

||||

of the Consumer Financial Protection Bureau at |

||||

Protection Bureau |

||||

|

|

|

||

|

|

|

|

|

|

|

|

|

|

Fees |

|

|

|

|

|

|

|

|

|

Annual Fee |

None |

|

None |

|

|

|

|

|

|

Transaction Fees: |

|

|

|

|

Balance Transfer |

Either $10 or 3% of the amount of each balance transfer or each cash advance, whichever |

|||

and Cash Advance |

is greater. |

|

|

|

International Transaction |

2% of each transaction in U.S. dollars. |

|

|

|

|

|

|

|

|

Penalty Fees: |

|

|

|

|

Late Payment |

$25 |

|

|

|

Returned Payment |

$25 |

|

|

|

|

|

|

|

|

Other Fees: |

|

|

|

|

Up to $10 for agent assisted payments. |

|

|

||

|

|

|

|

|

How We Will Calculate Your Balance: We use a method called “average daily balance (including new purchases).” See your account agreement for more details.

Prime Rate: After the introductory rate, the APR will vary based on changes in the Index, the Prime Rate (the base rate on corporate loans posted by at least 70% of the ten largest U.S. banks) published in the Wall Street Journal. The Index will be adjusted on the 25th day of each month or the business day preceding the 25th day if that day falls on a weekend or a holiday recognized by the Board of Governors of the Federal Reserve System. Changes in the Index will take effect beginning with the first billing cycle in the month following a change in the Index. Increases or decreases in the Index will cause the APR and periodic rate to fluctuate, resulting in increased or decreased Interest Charges on the Account. As of December 24, 2012, the Index was 3.25%.

aWe add 11.99% to the Prime Rate to determine the APR for Purchases, Balance Transfers, and Cash Advances. The Account will never have an APR over 21%.

bWe add 6.99% to the Prime Rate to determine the APR for Purchases, Balance Transfers, and Cash Advances. The Account will never have an APR over 21%.

cWe add 15.99% to the Prime Rate to determine the Penalty APR. The Account will never have an APR over 21.00%.

If at least one box at the top of the application is not checked, or, if too many boxes are inadvertently checked, you will be deemed to have selected the VISA Platinum card with the Low Rate option.

If you do not qualify for a VISA Platinum Card and you qualify for a VISA Classic Card, you will automatically be offered a VISA Classic Card.

The issuer and administrator of the credit card program is

The information about the Cost described in this table is accurate as of January 1, 2013.

This information may change after that date. To find out what may have changed, call us at

or write

Page 2 of 2 |

Please print and save this page for your records. |

01/13 |

|

|

| Fact Name | Description |

|---|---|

| Card Types Offered | The application allows you to choose between VISA Platinum, VISA Classic, and Gold MasterCard options. |

| Identification Requirement | Federal law mandates financial institutions to collect identifying information, such as name and address, to prevent illicit activities. |

| Married Wisconsin Residents | If applying individually or jointly with someone other than your spouse, financial information must be combined with your spouse's, and you may need to notify them. |

| State-Specific Laws | California residents can apply for credit in their name alone, while Ohio requires equal credit availability regardless of marital status. |

| Application Certification | Applicants must certify that all information provided is accurate. The application remains the property of the issuer regardless of approval. |

Completing a credit card application is an essential step for those seeking financial options. This process involves providing personal information, employment details, and financial data. Below are the steps you need to take to fill out the Credit Card Application form accurately and thoroughly.

Once the application is complete, it is important to ensure that all information is accurate before submission. This information allows the bank to evaluate your application and verify your identity, paving the way for potential credit approval.

1. What information do I need to provide on the credit card application form?

When applying for a credit card, you'll need to provide personal details such as your name, address, date of birth, and Social Security number. Information about your financial situation is also required, including your employer, position, and gross monthly income. If you're married and live in Wisconsin, you must also provide your spouse's information. Additionally, be prepared to show identification, like a driver’s license, to verify your identity.

2. What are the advantages of choosing between the different card types available?

The application offers several card types, including VISA Platinum, VISA Classic, and Gold MasterCard. Each option has its own benefits. For example, the VISA Platinum card may offer a lower introductory APR, making it advantageous for individuals seeking to minimize interest costs. On the other hand, if you're someone who values rewards, the Preferred Points Card might be the best fit for you. Consider your spending habits and financial needs when selecting a card type.

3. What happens to my application once I submit it?

Your application will be reviewed by the bank to assess your creditworthiness. The bank retains the application whether it's approved or denied. They may conduct background checks, including employment verification and credit history inquiries, to ensure all provided information is accurate. You will usually receive a decision promptly; however, it may take longer in certain situations depending on the complexity of your application.

4. Can I apply for joint credit, and what does that entail?

Yes, you can apply for joint credit on the application form by designating a co-applicant. This means both applicants will share the account and be responsible for the charges. It's essential that both parties agree on financial matters surrounding the account. If one applicant has a stronger credit history, the joint application could lead to better terms, such as lower interest rates. However, keep in mind that any defaults on the account will impact both individuals' credit scores.

5. What should I know about the interest rates and charges?

Interest rates can vary based on the card type you choose. For instance, introductory APR rates may be as low as 2.90% for the first six months, but after that, the rate will depend on the Prime Rate. You should also be aware of potential fees, like transaction or annual fees. Understanding these charges will help you decide the best card for your financial situation and prevent surprises down the road. Always read the terms carefully before making a decision.

Missing Required Information: Failure to provide essential details such as name, address, or Social Security number can lead to delays or denials. Make sure all sections are filled out completely.

Inaccurate Personal Details: Providing incorrect information about your birth date or address can create issues with identity verification. Double-check all entries to ensure accuracy.

Incorrect Card Selection: If you neglect to check the appropriate boxes for card type and benefit type, you may receive a card that doesn't meet your needs. Be sure to clearly indicate your choices.

Ignoring Eligibility Requirements: Not understanding that certain criteria apply for specific card types can result in wasted time. Review the qualifications and terms carefully.

Neglecting to Review Terms: Failing to read the terms and conditions may lead to unexpected fees and rates. Take the time to familiarize yourself with costs associated with the card.

Incorrect Co-Applicant Information: If applying jointly, ensure that the co-applicant's information is accurate and complete. Any discrepancies may need to be rectified later.

Not Providing Income Details: Omitting information about gross monthly income could hinder financial assessments. It’s vital to disclose everything honestly, including other sources of income if applicable.

When applying for a credit card, there are several other forms and documents that may frequently accompany the Credit Card Application form. Each of these documents serves a specific purpose in facilitating the application process and ensuring that both the applicant and the bank have a clear understanding of the financial relationship being established. Below are some of the commonly used forms and documents in conjunction with the Credit Card Application:

These documents collectively play a vital role in the credit application process, ensuring that banks can make informed lending decisions while protecting both the institution and the applicant. Properly completing and submitting these forms is essential for a smooth application experience.

The loan application form is similar to the credit card application form in that both documents collect essential personal and financial information from the applicant. This includes identity verification details such as name, address, date of birth, and Social Security number. Both forms also require applicants to disclose their employment status and income level, allowing lenders to assess the applicant's creditworthiness for loan approval. Both documents have sections for co-applicants, indicating that multiple parties can apply for credit jointly.

The mortgage application form is akin to the credit card application form as it requires a comprehensive financial profile from the borrower. Similar to credit card applications, mortgage applications gather information regarding the applicant's income, employment, and credit history. Both forms include disclosures about joint applications, community property laws, and potential obligations each party holds. Therefore, these documents ensure the lender has a complete picture of the borrower's financial situation in order to make informed decisions.

Auto loan applications share similarities with credit card application forms by focusing on financial and personal data necessary for credit evaluation. Like credit card applications, auto loan applications require the applicant to provide employment information, gross monthly income, and any co-applicants' details. Both formats emphasize legal implications regarding the accuracy of the information supplied, thus protecting both the lender and the borrower by ensuring shared responsibility for the loan.

The personal loan application form resembles a credit card application form in its need for personal identification and financial disclosure. Just like the credit card application, this form includes details about the applicant’s monthly income and employment status. Both forms also highlight that applicants should be truthful in their declarations, as lenders may perform background checks and credit inquiries to affirm the provided information.

The health insurance application form also mirrors the credit card application in terms of the necessary personal health information and demographic details required from applicants. Both forms usually ask for age, address, and Social Security number, which aids in identity verification. Health insurance applications similarly assess the applicant's eligibility based on medical history, which, like financial assessments in credit card applications, determines the applicant's risk profile.

A rental application form shares similar features with the credit card application form due to the extensive personal information needed. Applicants must provide identification details, income verification, and rental history, akin to the financial disclosures required in credit card applications. Both documents emphasize the necessity of accurate information, as landlords and lenders depend on this data to make informed decisions regarding approval.

The student loan application form is comparable to a credit card application because both aim to evaluate the applicant's financial stability and credibility. Applicants must provide personal identification and financial information, including expected income or funding sources. Both documents often request a co-signer or parental information if the applicant is not financially independent, addressing shared financial responsibility.

The business loan application form mirrors the credit card application form by requiring detailed financial information, including business income and credit history. Both forms assess the applicant's financial health, ensuring that lenders have critical details to evaluate their ability to repay debt. Documentation such as organizational structure and financial statements are commonly required to establish credibility, paralleling the thorough assessment necessary in credit card applications.

The line of credit application shares similarities with credit card applications through their information-gathering processes that determine creditworthiness. Both forms collect essential identification and financial data while also offering sections for joint applications. The emphasis on income stability and overall credit health in both formats illustrates the importance of understanding the applicant's financial reliability.

Finally, the installment loan application has similarities with the credit card application, as both require comprehensive personal and financial information to assess eligibility. Each form documents income sources and necessary disclosures regarding co-applicants. Furthermore, each application obligates the applicant to provide truthful statements, reinforcing the importance of accountability in the credit process.

When filling out a Credit Card Application form, make sure to follow these important guidelines:

Understanding the credit card application form is essential for anyone looking to apply for credit. Unfortunately, several misconceptions may lead to confusion. Here are nine common misunderstandings:

Awareness of these misconceptions can empower individuals as they navigate the credit card application process. It’s always wise to read through the terms and ask questions if something is unclear.

When filling out the Credit Card Application form, consider the following key takeaways:

Taking the time to carefully complete the application and understand its requirements can lead to a smoother process and better credit management.