The Credit Application form plays a crucial role for businesses and individuals seeking to establish credit with suppliers, vendors, or financial institutions. It serves as a comprehensive tool that captures essential details about the applicant’s identity and financial status. Key sections of the form include the company name, contact information, and billing address, providing basic identification alongside space for financial inquiries, such as the desired credit line. Applicants are asked to reveal their business structure—be it a corporation, partnership, or proprietorship—along with pertinent financial information, like annual sales and the duration of business operation. For businesses operating less than five years, a personal guarantee section becomes necessary, emphasizing the importance of accountability. Furthermore, the form requires banking details and trade references to facilitate credit assessment. Finally, included terms and conditions outline the responsibilities regarding payment and the creditor's rights, ensuring applicants are informed about the obligations they enter into. The Credit Application form is more than just paperwork; it sets the foundation for a future credit relationship between the borrower and lender.

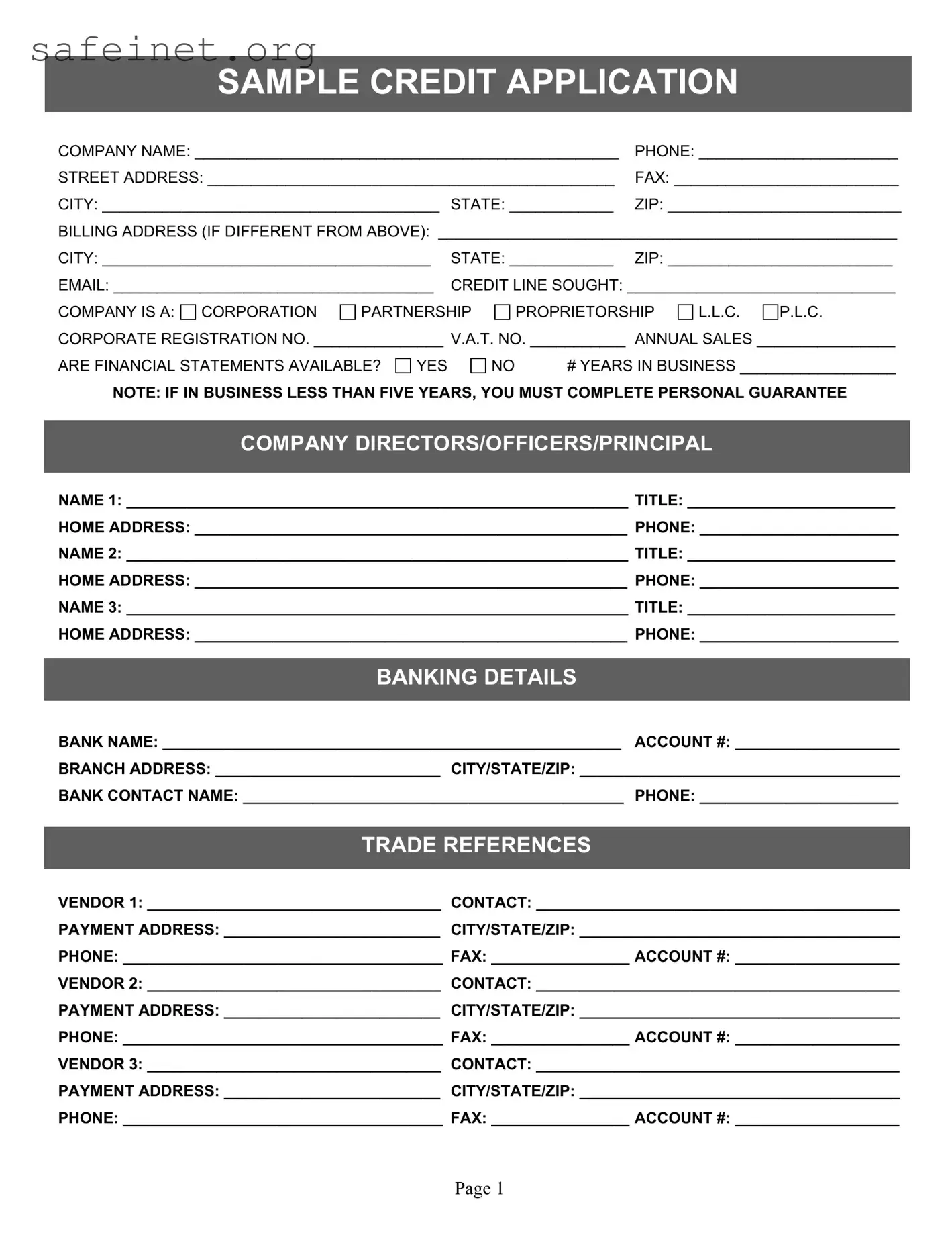

SAMPLE CREDIT APPLICATION

COMPANY NAME: _________________________________________________ |

PHONE: _______________________ |

|

STREET ADDRESS: _______________________________________________ |

FAX: __________________________ |

|

CITY: _______________________________________ |

STATE: ____________ |

ZIP: ___________________________ |

BILLING ADDRESS (IF DIFFERENT FROM ABOVE): _____________________________________________________ |

||

CITY: ______________________________________ |

STATE: ____________ |

ZIP: __________________________ |

EMAIL: _____________________________________ |

CREDIT LINE SOUGHT: _______________________________ |

|

COMPANY IS A: CORPORATION |

PARTNERSHIP |

|

PROPRIETORSHIP |

L.L.C. |

P.L.C. |

|

CORPORATE REGISTRATION NO. _______________ V.A.T. NO. ___________ ANNUAL SALES ________________ |

||||||

ARE FINANCIAL STATEMENTS AVAILABLE? |

YES |

NO |

# YEARS IN BUSINESS __________________ |

|||

NOTE: IF IN BUSINESS LESS THAN FIVE YEARS, YOU MUST COMPLETE PERSONAL GUARANTEE

COMPANY DIRECTORS/OFFICERS/PRINCIPAL

NAME 1: __________________________________________________________ TITLE: ________________________

HOME ADDRESS: __________________________________________________ PHONE: _______________________

NAME 2: __________________________________________________________ TITLE: ________________________

HOME ADDRESS: __________________________________________________ PHONE: _______________________

NAME 3: __________________________________________________________ TITLE: ________________________

HOME ADDRESS: __________________________________________________ PHONE: _______________________

BANKING DETAILS

BANK NAME: _____________________________________________________ ACCOUNT #: ___________________

BRANCH ADDRESS: __________________________ CITY/STATE/ZIP: _____________________________________

BANK CONTACT NAME: ____________________________________________ PHONE: _______________________

TRADE REFERENCES

VENDOR 1: __________________________________ CONTACT: __________________________________________

PAYMENT ADDRESS: _________________________ CITY/STATE/ZIP: _____________________________________

PHONE: _____________________________________ FAX: ________________ ACCOUNT #: ___________________

VENDOR 2: __________________________________ CONTACT: __________________________________________

PAYMENT ADDRESS: _________________________ CITY/STATE/ZIP: _____________________________________

PHONE: _____________________________________ FAX: ________________ ACCOUNT #: ___________________

VENDOR 3: __________________________________ CONTACT: __________________________________________

PAYMENT ADDRESS: _________________________ CITY/STATE/ZIP: _____________________________________

PHONE: _____________________________________ FAX: ________________ ACCOUNT #: ___________________

Page 1

CONDITIONS (TERMS ARE NET 30 DAYS UPON CREDIT APPROVAL)

TERMS OF SALE, INCLUDING TERMS OF PAYMENT AND CHARGES, FOR EACH PURCHASE ARE AGREED TO BE THOSE SPECIFIED ON THE FACE OF EACH INVOICE. THE CUSTOMER HEREBY AGREES TO PAY ALL COSTS OF COLLECTION OR LEGAL FEES SHOULD SUCH ACTION BE NECESSARY DUE TO

DISPUTES: ANY DISPUTE OR CONTROVERSY ARISING FROM THIS AGREEMENT WILL BE RESOLVED BY ARBITRATION BY THE AMERICAN ARBITRATION ASSOCIATION AT ORANGE COUNTY, CALIFORNIA. THE LANGUAGE OF THE ARBITRATION SHALL BE ENGLISH. THE NUMBER OF ARBITRATORS SHALL BE ONE. THE PARTIES AGREE THE AMERICAN ARBITRATION ASSOCIATION’S EXPEDITED RULES SHALL APPLY AND THEY WAIVE ALL RIGHT TO ANY HEARING REQUIRING WITNESS PRODUCTION. THE ARBITRATOR SHALL ISSUE AN AWARD BASED UPON THE WRITTEN DOCUMENTARY EVIDENCE SUPPLIED BY THE PARTIES. THE ARBITRATOR’S AWARD SHALL BE BINDING AND FINAL. THE LOSING PARTY SHALL PAY ALL ARBITRATION EXPENSES, INCLUDING ALL ATTORNEY’S FEES.

I HAVE READ AND UNDERSTAND THE ABOVE TERMS AND CONDITIONS, AND HEREBY AGREE TO THEM:

APPLICANT’S NAME: ______________________________________ TITLE: ________________________________

DATE: ______________________________________ APPLICANT’S SIGNATURE: ___________________________

FOR PROPRIETORS, PARTNERS,

I AUTHORIZE THE SELLER AND THEIR ASSIGNS TO OBTAIN A CONSUMER CREDIT REPORT ON MY CREDIT HISTORY.

DATE: ______________________________________ APPLICANT’S SIGNATURE: ____________________________

PERSONAL GUARANTEE

THE UNDERSIGNED, FOR CONSIDERATION DO HEREBY INDIVIDUALLY AND PERSONALLY GUARANTEE THE FULL AND PROMPT PAYMENT OF ALL INDEBTEDNESS HERETOFORE OR HEREAFTER INCURRED BY THE ABOVE BUSINESS. THIS GUARANTEE SHALL NOT BE AFFECTED BY THE AMOUNT OF CREDIT EXTENDED OR ANY CHANGE IN THE FORM OF SAID INDEBTEDNESS. NOTICE OF THE ACCEPTANCE OF THIS GUARANTEE, EXTENSION OF CREDIT, MODIFICATION IN TERMS OF PAYMENT, AND ANY RIGHT OR DEMAND TO PROCEED AGAINST THE PRINCIPAL DEBTOR IS HEREBY WAIVED. THIS GUARANTEE MAY ONLY BE REVOKED BY WRITTEN NOTICE WHICH SHALL BE SENT TO THE CREDITOR’S CREDIT OFFICE BY CERTIFIED MAIL. ANY REVOCATION DOES NOT REVOKE THE OBLIGATION OF THE GUARANTORS TO PROVIDE PAYMENT FOR INDEBTEDNESS INCURRED PRIOR TO THE REVOCATION. I AUTHORIZE THE SELLER AND THEIR ASSIGNS TO OBTAIN A CONSUMER CREDIT REPORT AND TO CONTACT MY REFERENCES AS NECESSARY. AS GUARANTOR, I AM ALSO BOUND BY THE ABOVE ARBITRATION CLAUSE.

GUARANTOR’S NAME: _____________________________________ |

SIGNATURE: __________________________ |

HOME ADDRESS: _____________________________ CITY/STATE/ZIP: ____________________________________ |

|

DATE: _______________________________________ TAX I.D. OR S.S. NO: _________________________________ |

|

GUARANTOR’S NAME: _____________________________________ |

SIGNATURE: __________________________ |

HOME ADDRESS: _____________________________ CITY/STATE/ZIP: ____________________________________

DATE: _______________________________________ TAX I.D. OR S.S. NO: _________________________________

Page 2

| Fact Name | Description |

|---|---|

| Identification of Company | The form requires the applicant to provide the company name, which is essential for establishing creditworthiness. |

| Contact Information | Applicants must include phone numbers, fax numbers, and email addresses, allowing the creditor to easily communicate. |

| Business Structure | The form requires identification of the business structure (corporation, partnership, proprietorship, LLC, or PLC) to assess liability and financial responsibilities. |

| Credit Line Sought | Applicants indicate the amount of credit they are seeking, which will guide the creditor's lending decisions. |

| Personal Guarantee Requirement | If the company is under five years old, a personal guarantee from owners is mandatory, ensuring personal accountability. |

| Arbitration Clause | The form includes a clause stating that disputes will be resolved through arbitration in Orange County, CA, emphasizing efficiency in conflict resolution. |

| Financial Statements | The company must disclose whether financial statements are available, which assists the creditor in evaluating the financial health of the business. |

| Legal Implications | The terms of the form relate to collecting legal fees and costs in case of non-payment, highlighting the seriousness of financial obligations. |

Completing a Credit Application is an essential step to secure the financial resources your business may need. Once you gather all necessary information, the process can be straightforward. Follow these steps to ensure that your application is filled out accurately and completely.

Once completed, double-check all entries for accuracy. Mistakes can lead to delays or issues with your application. Afterward, submit your application following any specific instructions provided by the creditor. This first step toward securing credit for your business can open up many opportunities for growth and success.

1. What is the purpose of the Credit Application Form?

The Credit Application Form serves as a formal request for credit from a supplier or lender. By completing this form, a business provides essential information about its financial status, including banking details and trade references. These details allow the creditor to assess the applicant's creditworthiness and determine the appropriate credit line to extend.

2. What information do I need to provide on the form?

The form requires several key pieces of information. You will need to provide your company name, phone number, street address, and email. Additionally, specify your billing address if it differs from the physical address. You must also indicate the credit line sought and the structure of your business (e.g., corporation or partnership). Other essential details include financial statements, company directors or officers' information, banking details, and trade references, among others.

3. Are financial statements necessary for all applicants?

Financial statements are required unless your business has been operating for more than five years. If your business is newer, including personal guarantees is essential to help establish your creditworthiness. This requirement ensures that creditors can verify your financial stability when considering your credit application.

4. What happens after I submit the Credit Application Form?

After submission, the creditor processes your application. They may contact your bank and trade references to confirm the information provided. Depending on their evaluation, the creditor will determine whether to grant credit, adjusting the credit line based on their findings. This process usually takes a short period, but delays can occur based on the responsiveness of the references contacted.

5. What are the terms of credit once approved?

The terms typically state that payments are due within 30 days of credit approval. Each invoice will outline specific terms regarding payment and any associated charges. It is critical to adhere to these terms, as failure to pay on time may lead to additional fees or even legal action, with the applicant liable for any collection costs incurred by the creditor.

6. What is the significance of the arbitration clause in the application?

The arbitration clause establishes that any disputes arising from the agreement will be resolved through arbitration rather than court litigation. Designed to streamline conflict resolution, the clause specifies that the American Arbitration Association will manage the process, adding a layer of predictability to any potential disputes. This means that any issues must be resolved outside of courtroom settings, typically resulting in fewer legal expenses for both parties.

7. Do I need to provide a personal guarantee?

If your business does not have a lengthy credit history, a personal guarantee is likely required. This is a formal agreement by the owners or principal individuals to be personally responsible for the business's debts. Even if the company defaults, the guarantor will remain liable for the outstanding debts, illustrating a level of commitment to the creditor regarding repayment.

Incomplete Information: Failing to fill in all required fields can lead to delays. Ensure every section is completed, including names and addresses.

Wrong Contact Details: Entering incorrect phone numbers or email addresses may prevent your application from being processed. Double-check for accuracy.

Missing Financial Statements: Not providing available financial statements can hinder your creditworthiness assessment. Include these if asked for.

Forgetting Personal Guarantees: If your business is less than five years old, you must complete personal guarantees. Omitting them can result in application rejection.

Not Specifying Credit Line: Indicating the amount of credit needed is essential. Skipping this part leaves lenders uncertain about your needs.

Ignoring Terms and Conditions: Failing to read the terms can lead to unexpected obligations later. Always review this section before signing.

Disregarding Trade References: Including outdated or incorrect vendor information may cause issues. Ensure you list current contacts for references.

In the process of applying for credit, several documents often accompany the Credit Application form. Each document serves a specific purpose, contributing to a comprehensive assessment of the business’s financial health and creditworthiness.

Understanding the purpose and importance of each accompanying document can enhance the likelihood of a successful credit application. Being well-prepared not only streamlines the process but also builds trust with potential creditors.

The credit application form shares similarities with a loan application form, as both documents aim to assess a borrower’s creditworthiness. Each form requires an applicant to provide personal and financial information, including income details, debt obligations, and employment history. While a credit application focuses on establishing a credit line for business purposes, a loan application often seeks funding for specific projects or personal use. Additionally, both documents typically require signatures that authorize credit checks and the disclosure of sensitive financial information.

Another document resembling the credit application is the lease application form used in residential and commercial real estate. Both forms collect detailed information on an applicant's financial history, including income verification and references. This helps landlords or property management companies evaluate whether a potential tenant can reliably meet rental payment obligations. In both cases, accurate and transparent information is crucial, as any discrepancies can lead to denial, whether for credit or tenancy.

The service agreement can also be compared to the credit application form. Service agreements often include clauses regarding payment terms, responsibilities, and obligations of both parties involved. Similarly, the credit application outlines the terms of credit, including repayment obligations and consequences for defaulting on payments. Each document establishes a legal understanding that is key to ensuring both parties honor their commitments and provides recourse if issues arise.

A business loan agreement stands alongside the credit application form in terms of purpose and content. Both documents assess creditworthiness and include similar core data, such as business structure, ownership details, and financial projections. While the credit application seeks to simply extend credit, the business loan agreement outlines the terms of a specific loan, detailing interest rates, repayment schedules, and collateral involved. Each document plays a vital role in facilitating financial transactions while protecting the interests of the lender.

Finally, a personal guarantee form aligns closely with the credit application, especially regarding liability. When a business owner personally guarantees company debts, this document specifies their commitment to cover any outstanding debts if the business defaults. Like the credit application, it requires personal financial details and signatures to validate the commitment. Both documents help mitigate risk for lenders, ensuring they have multiple avenues for recourse should financial troubles arise.

When filling out a credit application form, paying close attention can make a significant difference in the outcome. Here are seven essential do's and don'ts to consider during this important process:

Being thorough and honest when completing your credit application can not only facilitate a smoother process but also impact the type of credit you are extended. Remember, clarity and accuracy are your best allies in this endeavor.

When it comes to credit application forms, many misconceptions can lead to confusion. Understanding what is true and what is not can help streamline the process of applying for credit. Here are ten common misconceptions, along with explanations to clarify each one:

By debunking these myths, individuals and businesses can navigate the credit application process with greater confidence and clarity. Understanding the requirements and expectations can lead to a smoother experience when applying for credit.

When filling out and using the Credit Application form, the following key takeaways can enhance your experience and ensure accuracy:

By keeping these points in mind, you can ensure a smoother process and establish a solid foundation for your credit relationship.