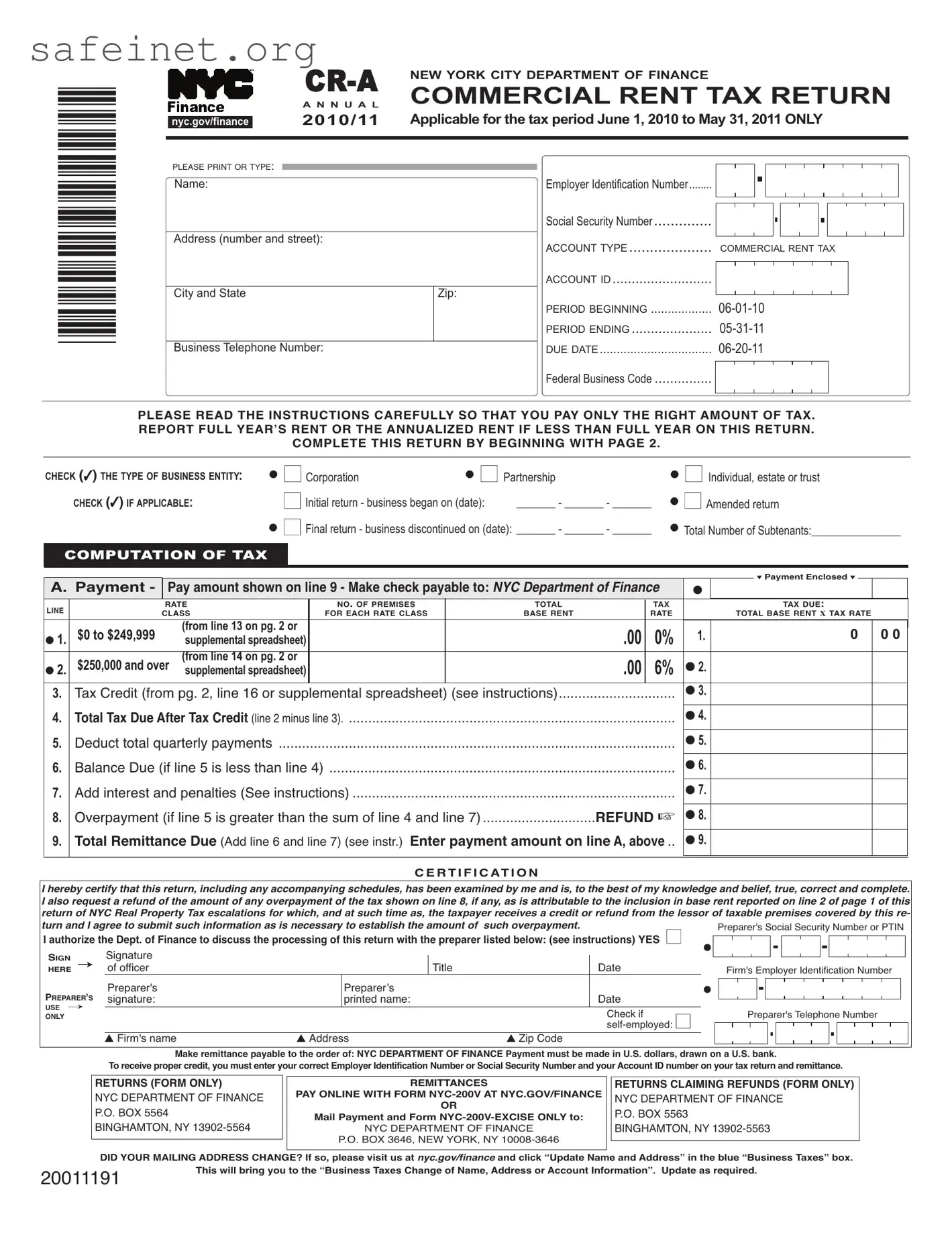

The Cr A form, officially known as the Annual Commercial Rent Tax Return, serves as an essential tool for businesses operating within New York City. It covers the tax period from June 1, 2010, to May 31, 2011, and outlines the necessary steps for businesses to report their annual commercial rents accurately. The form requires various crucial details, including the name, address, and type of business entity, along with tax identification information such as the Employer Identification Number or Social Security Number. It focuses on computing the tax due based on the total base rent paid over the specified period, establishing different tax rates for rentals below and above $250,000. Moreover, the Cr A form invites businesses to check boxes that indicate if the return is initial, final, or amended, reflecting changes in business operations. Providing deductions for any rent applied to residential use or received from subtenants is also critical for accurate tax calculation. The form includes a certification section where the business owner affirms the accuracy of the provided information. For those seeking refunds or adjustments, additional instructions guide them on how to proceed correctly. This form ultimately plays a pivotal role in ensuring compliance with tax obligations while allowing businesses to navigate their reporting needs effectively.

*20011191*

|

|

|

|

NEW YORK CITY DEPARTMENT OF FINANCE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

A N N U A L |

COMMERCIAL RENT TAX RETURN |

|

||||||||||||||||||||||||||

|

|

2010/11 |

ApplicableforthetaxperiodJune1,2010toMay31,2011ONLY |

|

||||||||||||||||||||||||||||

|

nyc.gov/finance |

|

|

|||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PLEASE PRINT OR TYPE: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name: |

|

|

|

|

Employer Identification Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

Social Security Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Address (number and street): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

ACCOUNT TYPE |

COMMERCIAL RENT TAX |

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ACCOUNT ID |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City and State |

|

|

|

Zip: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

PERIOD BEGINNING |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

PERIOD ENDING |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Business Telephone Number: |

|

|

DUE DATE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Federal Business Code ...............

PLEASE READ THE INSTRUCTIONS CAREFULLY SO THAT YOU PAY ONLY THE RIGHT AMOUNT OF TAX. REPORT FULL YEAR’S RENT OR THE ANNUALIZED RENT IF LESS THAN FULL YEAR ON THIS RETURN.

COMPLETE THIS RETURN BY BEGINNING WITH PAGE 2.

CHECK (✓)THE TYPE OF BUSINESS ENTITY:

CHECK (✓)IF APPLICABLE:

COMPUTATION OF TAX

● ■Corporation |

● ■ Partnership |

|

■Initial return - business began on (date): |

_______ - _______ - _______ |

|

● ■Final return - business discontinued on (date): _______ - _______ - _______

●■ Individual, estate or trust

●■Amended return

●Total Number of Subtenants:________________

|

|

|

|

|

|

|

|

|

|

|

|

|

▼ Payment Enclosed ▼ |

|

|

|

A. Payment - |

Pay amount shown on line 9 - Make check payable to: NYCDepartmentofFinance |

● |

|

|

|

|

||||||||

|

|

|

|

|

|||||||||||

|

LINE |

|

RATE |

|

NO. OF PREMISES |

|

TOTAL |

|

TAX |

|

|

TAX DUE: |

|||

|

|

CLASS |

|

FOR EACH RATE CLASS |

|

BASE RENT |

|

RATE |

|

TOTAL BASE RENT X TAX RATE |

|||||

|

● 1. |

$0 to $249,999 |

|

(from line 13 on pg. 2 or |

|

|

|

|

.00 |

0% |

1. |

0 |

0 0 |

||

|

|

supplemental spreadsheet) |

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$250,000 and over |

(from line 14 on pg. 2 or |

|

|

|

|

.00 |

6% |

● 2. |

|

|

|

|

|

|

● 2. |

supplemental spreadsheet) |

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

3. |

Tax Credit (from pg. 2, line 16 or supplemental spreadsheet) (see instructions) |

|

● 3. |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

4. |

TotalTaxDueAfterTaxCredit(line 2 minus line 3) |

|

|

● 4. |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5. |

Deduct total quarterly payments |

|

|

|

|

● 5. |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6. |

Balance Due (if line 5 is less than line 4) |

......................................................................................... |

|

|

|

|

● 6. |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

7. |

Add interest and penalties (See instructions) |

|

|

● 7. |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

8. |

Overpayment (if line 5 is greater than the sum of line 4 and line 7) |

............................. |

REFUND ☞ |

● 8. |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

9. |

Total Remittance Due (Add line 6 and line 7) (see instr.) Enter payment amount on lineA,above.. |

● 9. |

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CERTIFICATION

I hereby certify that this return, including any accompanying schedules, has been examined by me and is, to the best of my knowledge and belief, true, correct and complete. I also request a refund of the amount of any overpayment of the tax shown on line 8, if any, as is attributable to the inclusion in base rent reported on line 2 of page 1 of this return of NYC Real Property Tax escalations for which, and at such time as, the taxpayer receives a credit or refund from the lessor of taxable premises covered by this re- turn and I agree to submit such information as is necessary to establish the amount of such overpayment.

I authorize the Dept. of Finance to discuss the processing of this return with the preparer listed below: (see instructions)YES ■ |

|

Preparer's Social Security Number or PTIN |

|||||||||||||||||||||||||||||||||||

● |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

Signature |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

HERESIGN → of officer |

|

|

Title |

|

Date |

|

|

Firm's Employer Identification Number |

|||||||||||||||||||||||||||||

|

|

|

Preparer's |

|

Preparer’s |

|

|

● |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

PREPARER'S |

signature: |

|

printed name: |

|

Date |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

USE → |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

Check if |

|

|

|

|

Preparer's Telephone Number |

||||||||||||||||||||||||||

ONLY |

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

▲ Firm's name |

▲ Address |

▲ Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Make remittance payable to the order of: NYC DEPARTMENT OF FINANCE Payment must be made in U.S. dollars, drawn on a U.S. bank.

Toreceivepropercredit,youmustenteryourcorrectEmployerIdentificationNumberorSocialSecurityNumberandyourAccountIDnumberonyourtaxreturnandremittance.

RETURNS (FORM ONLY)

NYC DEPARTMENT OF FINANCE P.O. BOX 5564 BINGHAMTON, NY

REMITTANCES

PAY ONLINE WITH FORM

OR

Mail Payment and Form

NYC DEPARTMENT OF FINANCE

P.O. BOX 3646, NEW YORK, NY

RETURNS CLAIMING REFUNDS (FORM ONLY)

NYC DEPARTMENT OF FINANCE

P.O. BOX 5563

BINGHAMTON, NY

DID YOUR MAILING ADDRESS CHANGE? If so, please visit us at nyc.gov/finance and click “Update Name and Address” in the blue “Business Taxes” box.

20011191 |

This will bring you to the “Business Taxes Change of Name, Address or Account Information”. Update as required. |

|

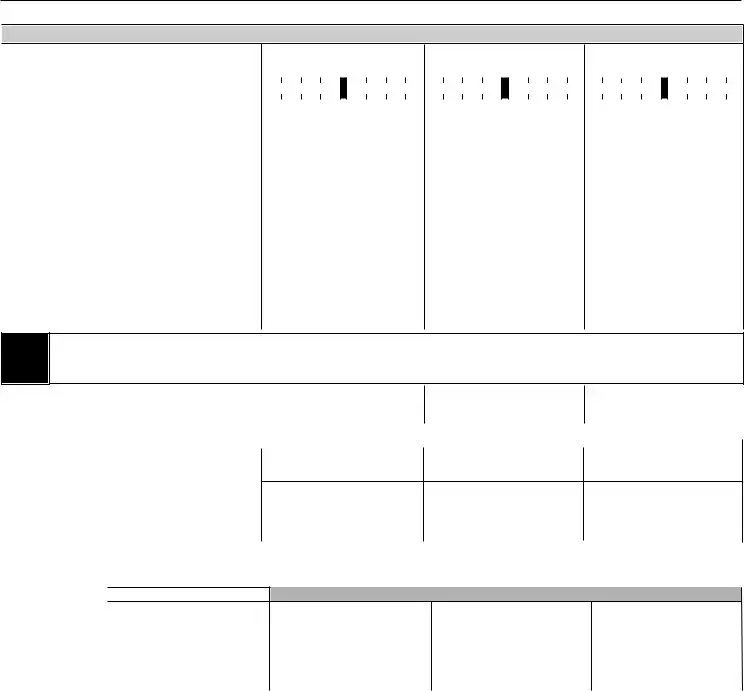

Form |

Page 2 |

USETHISPAGEIFYOUHAVETHREEORLESSPREMISES/SUBTENANTSOR,MAKECOPIESOFTHISPAGETOREPORTAD- DITIONAL PREMISES/SUBTENANTS. IF YOU WISH TO REPORT MORE THAN THREE PREMISES/SUBTENANTS, AND CHOOSE TO USE A SPREADSHEET, YOU MUST USE THE FINANCE SUPPLEMENTAL SPREADSHEET, WHICHYOUCAN DOWNLOADFROMOURWEBSITEATWWW.NYC.GOV/CRTINFO.

EACH LINE MUST BEACCURATELYCOMPLETED. YOUR DEDUCTION WILLBE DISALLOWED IF INACCURATE INFORMATION IS SUBMITTED.

LINE |

DESCRIPTION |

PREMISES 1 |

PREMISES 2 |

PREMISES 3 |

||||

● 1a. |

Street Address ......................................................... 1a. |

|

|

|

|

|

|

|

1b. Zip Code ..................................................................1b. |

________________________________________________________________________________________ |

|||||||

1c. |

Block and 1d. Lot Number...................................1c/1d. ________________________________________________________________________________________ |

|||||||

|

|

|

1c. BLOCK |

1d. LOT |

1c. BLOCK |

1d. LOT |

1c. BLOCK |

1d. LOT |

● 2. |

Gross Rent Paid (see instructions) |

2. |

________________________________________________________________________________________ |

3. |

Rent Applied to Residential Use |

3. |

________________________________________________________________________________________ |

4a. SUBTENANT'S NAME |

4a. |

________________________________________________________________________________________ |

|

●4b. Employer Identification Number (EIN) for

|

partnerships or corporations |

4b. |

● 4b. EIN _____________________ ● 4b. EIN_____________________ ● 4b. EIN ____________________ |

4c. Social Security Number for individuals |

4c. |

● 4c. SSN_____________________ ● 4c. SSN ____________________ ● 4c. SSN ____________________ |

|

4d. RENT RECEIVED FROM SUBTENANT |

|

|

|

|

(see instructions if more than one subtenant) |

4d. |

___________________________________________________________________________________________________ |

5a. |

Other Deductions (attach schedule) |

5a. |

________________________________________________________________________________________ |

5b. |

Commercial Revitalization Program |

|

|

|

special reduction (see instructions) |

5b. |

________________________________________________________________________________________ |

6. |

Total Deductions (add lines 3, 4d, 5a and 5b) |

6. |

________________________________________________________________________________________ |

7.Base Rent Before Rent Reduction (line 2 minus line 6) ....7. ________________________________________________________________________________________

4If the line 7 amount represents rent for less than the full year, proceed to line 10a, or

NOTE 4If the line 7 amount plus the line 5b amount is $249,999 or less and represents rent for a full year, transfer line 9 to line 13, or 4If the line 7 amount plus the line 5b amount is $250,000 or more and represents rent for a full year, transfer line 9 to line 14

8. |

35% Rent Reduction (35% X line 7) |

8. |

________________________________________________________________________________________ |

|||||||

9. |

Base Rent Subject to Tax (line 7 minus line 8) |

9. |

________________________________________________________________________________________ |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

COMPLETE LINES 10a, 11 AND 12 ONLY IF YOU RENTED PREMISES FOR LESS THAN THE FULL YEAR |

|||||||||

10a. Number of Months at Premises during the tax period |

|

|

|

|

|

|

|

|

|

|

10a. # of months |

10b. |

From: |

10a. # of months |

10b. From: |

10a. # of months |

10b. From: |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10c. |

To: |

|

10c. To: |

|

|

10c. To: |

|

|

|

|

|

|

|

|

|

|

|

11.Monthly Base Rent before rent reduction

(line 7 plus line 5b divided by line 10a) |

11. ________________________________________________________________________________________ |

12.Annualized Base Rent before rent reduction

(line 11 X 12 months) |

12. ________________________________________________________________________________________ |

■If the line 12 amount is $249,999 or less, transfer the line 9 amount (NOT THE LINE 12AMOUNT) to line 13

■If the line 12 amount is $250,000 or more, transfer the line 9 amount (NOT THE LINE 12AMOUNT) to line 14

*20021191*

RATE CLASS |

TAX RATE |

13.($0 - 249,999)............0%.....13. ______________________________________________________________________________________

14.($250,000 or more)... 6%.....14. ______________________________________________________________________________________

15.Tax Due before credit

(line 14 multiplied by 6%) |

15. |

16.Tax Credit (see worksheet below) .16. ______________________________________________________________________________________

Note: The tax credit only applies if line 7 plus line 5b (or line 12, if applicable) is at least $250,000, but is less than $300,000. All others enter zero.

Tax Credit Computation Worksheet

■If the line 7 amount represents rent for the full 12 month period, your credit is calculated as follows:

Amount on line 15 X ($300,000 minus the sum of lines 7 and 5b) = _____________ = your credit

$50,000

■If the line 7 amount represents rent for less than the full 12 month period, your credit is calculated as follows:

Amount on line 15 X ($300,000$50,000minus line 12) = _____________ = your credit

TRANSFER THE AMOUNTS FROM LINES 13 THROUGH 16 TO THE CORRESPONDING LINES ON PAGE 1

20021191 |

|

|

| Fact Name | Details |

|---|---|

| Form Identification | CR-A is the Annual Commercial Rent Tax Return for New York City. |

| Tax Period | This form is applicable for the tax period from June 1, 2010, to May 31, 2011. |

| Filing Requirement | All commercial tenants in New York City must file this form if their rent exceeds the exemption threshold. |

| Payment Methods | Payments can be made via check or online using the NYC Department of Finance website. |

| Tax Rates | The tax rates are 0% for rents up to $249,999 and 6% for rents of $250,000 or more. |

| Penalties | Late payments may incur interest and penalties as specified in the instructions. |

| Certification Requirement | Filers must certify that the information provided on the return is true and complete. |

| Additional Deductions | There are provisions for deductions related to subtenants and other expenses. |

Filling out the CR-A form is a critical step for ensuring your compliance regarding commercial rent tax in New York City. Once the form is filled out accurately, you can submit it along with any taxes owed or applicable claims for refunds. Follow the steps below to complete the form efficiently.

What is the CR A form and who must file it?

The CR A form is an Annual Commercial Rent Tax Return used by businesses in New York City. Specifically, this form applies to taxpayers who are obligated to report and pay the commercial rent tax for the period from June 1, 2010, to May 31, 2011. Businesses that rent commercial properties and whose annual rent exceeds a certain threshold must file this form to determine their tax liability. This includes corporations, partnerships, and individual entities engaged in business operations within the city.

How do I calculate the tax due using the CR A form?

Tax liability is determined based on the total base rent paid for the commercial premises. The form provides two tax rate classifications: for rents less than $250,000, the tax rate is 0%, while for rents of $250,000 or more, the tax rate is 6%. To calculate the tax due, first report the total base rent on the appropriate line. If applicable, any tax credits can be factored in as well. Deduct the eligible credits from the total tax due to arrive at the final amount owed.

What is required if my business has multiple commercial premises?

If your business operates from three or fewer commercial premises, you can report all relevant details directly on the form. However, if you have more than three premises, you must use a supplemental spreadsheet available from the NYC Department of Finance's website. Accurate reporting is crucial, as any misinformation may lead to disallowed deductions. Make sure to include gross rent, subtenant information, and other relevant amounts as instructed.

What should I do if I made an error on my submitted CR A form?

If an error is discovered after submission, you have the option to file an amended CR A form. Indicate clearly that it is an amended return and provide the corrected information. It is advisable to attach a detailed explanation of the amendments to clarify the changes made. By doing so, you help ensure that your tax information is accurate and minimizes the risk of penalties associated with incorrect filings.

Where do I send the completed CR A form and payment?

After completing the CR A form, send the return along with any payment to the designated addresses as outlined in the instructions. For returns only, mail the form to the New York City Department of Finance, P.O. Box 5564, Binghamton, NY 13902-5564. If you are submitting a payment, use Form NYC-200V and mail it along with the payment to the New York City Department of Finance, P.O. Box 3646, New York, NY 10008-3646. Online payment options are also available at the NYC Department of Finance website.

Ignoring Instructions: Many individuals overlook the importance of reading the instructions carefully. Instructions provide essential details on how to accurately complete the form.

Incorrect Business Type: Selecting the wrong type of business entity can lead to problems. Ensure the correct box is checked to reflect whether the business is a corporation, partnership, or individual.

Missing Tax Period Dates: Failing to fill out the correct tax period dates is a frequent mistake. Make sure to enter the applicable dates consistently throughout the form.

Inaccurate Employer Identification Number (EIN): Entering an incorrect EIN or Social Security Number can cause submission errors. Double-check these numbers for accuracy.

Calculation Errors: Mistakes in calculations, especially when determining the total tax due, are common. Review all calculations thoroughly to ensure they are correct.

Not Reporting Full-Year Rent: Some individuals mistakenly report only partial rents. Report the full year’s rent unless specified otherwise.

Tax Credit Misunderstanding: Confusion over eligibility for tax credits may lead to incorrect entries. Review the details about tax credits to ensure correct application.

Omitting Signature: Neglecting to sign the certification section invalidates the form. Remember to sign and date the return.

Improper Payment Submission: Payments must be made in U.S. dollars and from a U.S. bank. Ensure the payment process is correctly followed.

Failing to Update Address: If the mailing address has changed and is not updated, it can lead to important correspondence being lost. Update the address as necessary.

The CR-A form is an essential document for filing the annual commercial rent tax in New York City. However, it is often accompanied by other forms and documents to provide complete information and assist in the proper processing of the tax return. Here are five commonly used documents alongside the CR-A form:

Using these additional forms can streamline the filing process and ensure that all necessary information is submitted correctly. This coordination helps avoid potential issues or delays in processing your commercial rent tax return.

The Form CR-A, used for the Annual Commercial Rent Tax Return in New York City, bears similarities to the IRS Form 1040, which is the standard individual income tax return. Both forms require the taxpayer to provide personal information, such as names, addresses, and social security numbers, to ensure proper identification. They also mandate a detailed reporting of income—CR-A focuses on commercial rent, while Form 1040 includes all sources of personal income. This structured approach ensures that the correct tax amount is calculated based on the reported figures.

Another document comparable to the Form CR-A is the IRS Form 1065, which is utilized by partnerships to report income and deductions. Similar to the CR-A, this form necessitates a thorough accounting of revenues and expenses. Partnerships must disclose the individual income of each partner, much like CR-A requires businesses to report rents received from subtenants. Both forms emphasize transparency in financial reporting to ensure compliance with tax regulations.

The New York State Form IT-201, the Resident Income Tax Return, shares an overarching objective with the CR-A: both facilitate the collection of necessary tax information from taxpayers. IT-201 asks for comprehensive personal and financial data, including income sources and exemptions. This emphasis on detailed disclosures parallels the CR-A's need for meticulous reporting of commercial rents and deductions, ensuring an accurate assessment of tax obligations.

Form NYC-200V, used for filing certain business taxes in New York City, aligns closely with the CR-A in terms of administrative procedure. Both forms involve computations related to tax liabilities and require adherence to specific deadlines. The experience of preparing these forms aims to minimize errors and encourage timely submissions, enhancing overall compliance with tax deadlines.

The IRS Schedule C, Profit or Loss from Business, is another document similar to the CR-A. Schedule C requires business owners to report their income and expenses, offering an overview of profitability. Both documents require a detailed breakdown of financial activities to evaluate tax responsibilities accurately. Crucially, they each serve to document business performance for tax purposes, highlighting the interconnectedness of business reporting across different jurisdictions.

The Sales and Use Tax Return, often required by states, resembles the CR-A as both forms collect substantial financial information from businesses. Just like the CR-A assesses the commercial rent tax due based on reported receipts, the Sales and Use Tax Return calculates taxes based on sales made. Both require careful compilation of financial data to prevent penalties or overpayment, fostering accuracy in tax reporting.

The Form 941, the Employer’s Quarterly Federal Tax Return, provides another parallel to the CR-A. While Form 941 focuses on employment taxes, both require meticulous record-keeping and submission of relevant account information on a recurring basis. The attention to detail necessary for both submissions speaks to the importance of accountability in financial reporting for tax obligations.

The New York City Business Corporation Tax Return (Form NYC-1127) also shares a structural similarity with the CR-A. Both forms require entities conducting business in New York City to provide detailed tax information, including financial summaries and deductions. This consistency in required information emphasizes compliance with local tax laws to ensure accurate tax calculations and to limit the risk of audits.

Lastly, the IRS Form 990, used by tax-exempt organizations to report financial information, has commonalities with the CR-A regarding transparency and public accountability. While Form 990 aims to inform the public about the financial health of nonprofits, it similarly requires detailed disclosures of financial activities. Both forms function to uphold the principles of financial integrity in their respective contexts, ensuring that stakeholders can access essential financial information.

When filling out the CR-A form for the New York City Department of Finance, it’s important to approach the process carefully. Here’s a list of dos and don’ts to help ensure your submission is accurate and complete.

Misconception 1: The Cr A form is only for large businesses.

This is not true. The Cr A form applies to all commercial entities renting space in New York City, regardless of size. Even small businesses must complete the form if their rent meets the tax thresholds.

Misconception 2: Rental payments made by subtenants do not need to be reported.

It is essential to report the rent received from subtenants. Failure to do so can lead to penalties, as this information is integral to calculating the total rental income for the commercial rent tax.

Misconception 3: Only corporations need to file a Cr A form.

This is incorrect. The form must be filed by all types of business entities, including partnerships, individuals, estates, and trusts. Each type of entity is responsible for accurately reporting their rental income.

Misconception 4: The Cr A form can be submitted without any deductions.

While it is possible to file without claiming deductions, many taxpayers are eligible for deductions that can reduce their tax liability. It is advisable to review the form's instructions to ensure all applicable deductions are claimed.

Misconception 5: The due date for filing is always consistent.

The due date depends on the specific tax period covered by the Cr A form. For the period of June 1, 2010, to May 31, 2011, it has a distinct deadline. Taxpayers should always check the specific due dates for each applicable tax year.

Misconception 6: No payment is necessary if a refund is anticipated.

Misconception 7: Submission errors will not affect the tax outcome.

This is a dangerous assumption. Errors in reporting rental amounts or miscalculations can lead to increased fines or penalties. Accuracy is critical for compliance and to ensure that the correct amount is reported to avoid future complications.

When filling out the CR A form for the Commercial Rent Tax return, keep these key takeaways in mind: