The Court Inventory Form serves as a crucial document in managing the estate of a deceased individual in New York's Surrogate’s Court. This form is used to report and summarize the assets of the estate for tax purposes, providing a clear overview of the total valuation of all possessions, from real estate and bank accounts to stocks and insurance policies. Its structure enables fiduciaries or attorneys to certify the details essential for the probate process. Attached documentation, such as a detailed asset list or relevant tax forms, ensures that all financial components are accounted for. It is also necessary to disclose specific information, such as the decedent's date of death and the fiduciary's details, clarifying roles and responsibilities. By breaking down the estate into sections—like non-probate assets, jointly owned property, and transfers during the decedent's life—the form helps streamline the probate process. Compliance with requirements detailed in Rule §207.20(a) is essential to avoid delays or complications. Whether the estate includes residential properties or investment portfolios, the Court Inventory Form provides a comprehensive snapshot, aiding in the transparent and fair distribution of assets.

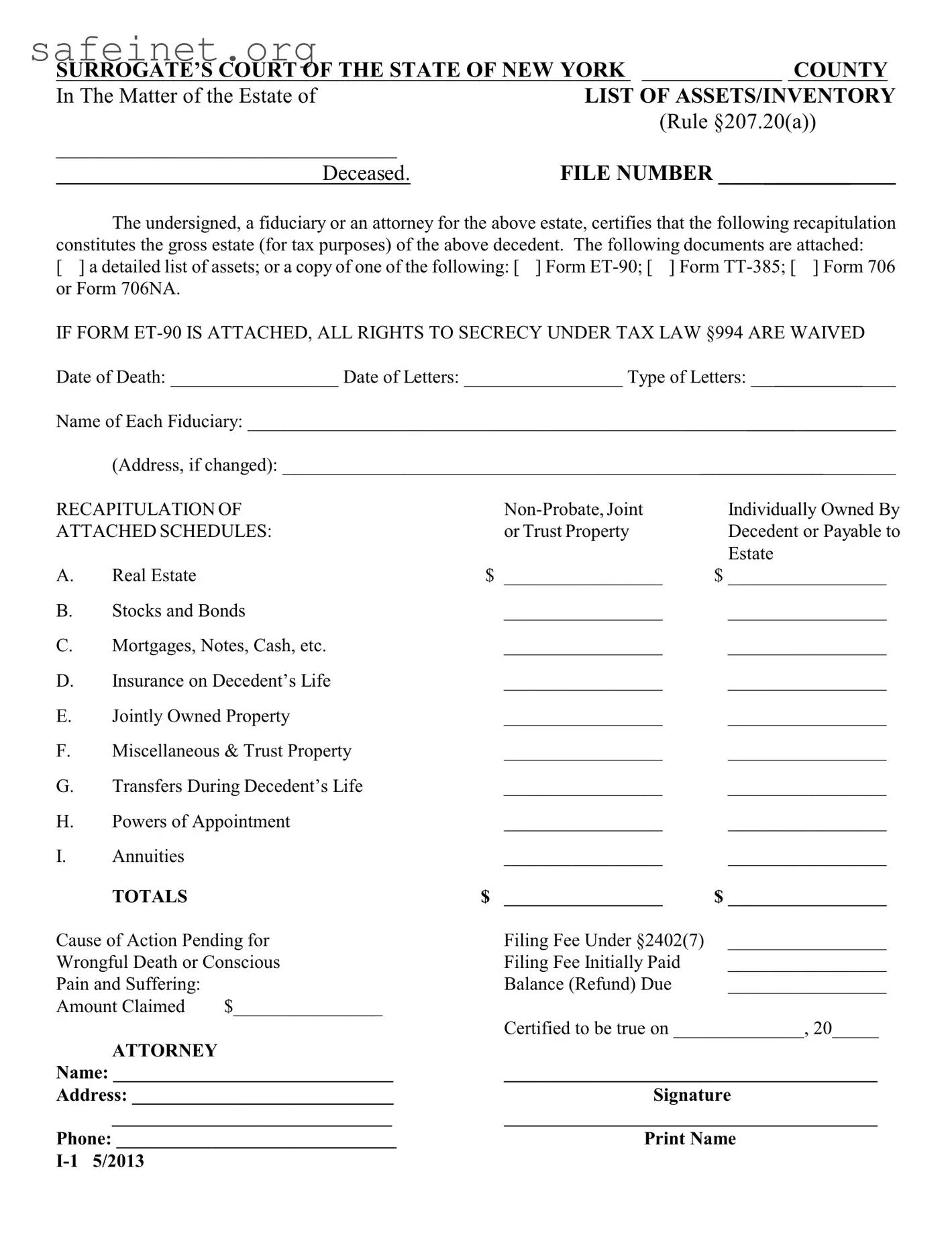

SURROGATE’S COURT OF THE STATE OF NEW YORK |

|

COUNTY |

|

In The Matter of the Estate of |

LIST OF ASSETS/INVENTORY |

||

|

|

(Rule §207.20(a)) |

|

_______________________________ |

|

|

|

Deceased. |

FILE NUMBER ________________________ |

||

The undersigned, a fiduciary or an attorney for the above estate, certifies that the following recapitulation constitutes the gross estate (for tax purposes) of the above decedent. The following documents are attached:

[ ] a detailed list of assets; or a copy of one of the following: [ ] Form

IF FORM

Date of Death: __________________ Date of Letters: _________________ Type of Letters: _________________________

Name of Each Fiduciary: _____________________________________________________________________________________

(Address, if changed): _______________________________________________________________________________

RECAPITULATION OF |

|

Individually Owned By |

|||

ATTACHED SCHEDULES: |

|

or Trust Property |

Decedent or Payable to |

||

|

|

|

|

|

Estate |

A. |

Real Estate |

|

$ |

_________________ |

$ _________________ |

B. |

Stocks and Bonds |

|

_________________ |

_________________ |

|

C. |

Mortgages, Notes, Cash, etc. |

|

_________________ |

_________________ |

|

D. |

Insurance on Decedent’s Life |

|

_________________ |

_________________ |

|

E. |

Jointly Owned Property |

|

_________________ |

_________________ |

|

F. |

Miscellaneous & Trust Property |

|

_________________ |

_________________ |

|

G. |

Transfers During Decedent’s Life |

|

_________________ |

_________________ |

|

H. |

Powers of Appointment |

|

_________________ |

_________________ |

|

I. |

Annuities |

|

|

_________________ |

_________________ |

|

TOTALS |

|

$ |

_________________ |

$ _________________ |

Cause of Action Pending for |

|

Filing Fee Under §2402(7) |

_________________ |

||

Wrongful Death or Conscious |

|

Filing Fee Initially Paid |

_________________ |

||

Pain and Suffering: |

|

|

Balance (Refund) Due |

_________________ |

|

Amount Claimed |

$________________ |

|

|

|

|

|

|

|

|

Certified to be true on ______________, 20_____ |

|

|

ATTORNEY |

|

|

|

|

Name: ______________________________ |

|

________________________________________ |

|||

Address: ____________________________ |

|

Signature |

|||

|

______________________________ |

|

________________________________________ |

||

Phone: ______________________________ |

|

Print Name |

|||

5/2013 |

|

|

|

|

|

GROSS ASSETS

(Attach Additional Page If Necessary)

A. |

REAL ESTATE (Individually owned property) |

|

|

Description |

Date of Death Value |

____________________________________________ |

_______________________________ |

|

____________________________________________ |

_______________________________ |

|

____________________________________________ |

_______________________________ |

|

B. |

STOCKS AND BONDS (Individually Owned) |

|

|

|

Description, Including Face Amount of Bonds |

|

|

|

and Number of Shares |

|

Date of Death Value |

____________________________________________ |

___________________________________ |

____________________________________________ |

___________________________________ |

____________________________________________ |

___________________________________ |

C. MORTGAGES, NOTES AND CASH (Including Bank Deposits) (Jointly owned property should be reported at E and trust property at F)

Description |

Date of Death Value |

____________________________________________ |

____________________________________ |

____________________________________________ |

____________________________________ |

____________________________________________ |

____________________________________ |

D. INSURANCE ON DECEDENT’S LIFE

(1)Payable to Estate

Description |

Date of Death Value |

|

_________________________________________ |

_________________________________ |

|

_________________________________________ |

_________________________________ |

|

(2) |

Payable to Named Beneficiary |

|

Description |

Date of Death Value |

|

_________________________________________ |

__________________________________ |

|

_________________________________________ |

__________________________________ |

|

E.JOINTLY OWNED PROPERTY (Real and Personal Property)

(1)Real Estate

|

|

Joint |

|

Description |

Tenant |

Date of Death Value |

|

________________________________ |

_________________ |

_______________________ |

|

________________________________ |

_________________ |

_______________________ |

|

(2) |

Stocks and Bonds |

|

|

|

|

Joint |

|

Description |

Tenant |

Date of Death Value |

|

________________________________ |

_________________ |

________________________ |

|

________________________________ |

_________________ |

________________________ |

|

(3)Mortgages, Notes and Cash

|

Joint |

|

Description |

Tenant |

Date of Death Value |

________________________________ |

_________________ |

_________________________ |

________________________________ |

_________________ |

_________________________ |

F.OTHER MISCELLANEOUS PROPERTY

(1)Individually Owned

Description |

|

Date of Death Value |

________________________________ |

__________________ |

_________________________ |

________________________________ |

__________________ |

_________________________ |

(2)Firearms (Check appropriate box)

[ |

] Yes, see attached Firearms Inventory Form |

Date of Death Value |

[ |

] None |

___________________________________ |

(3)Assets Passing to the Estate from Employment

|

Description |

Date of Death Value |

|

____________________________________________ |

___________________________________ |

||

____________________________________________ |

___________________________________ |

||

|

(4) |

Trust Property |

|

|

Description |

Date of Death Value |

|

____________________________________________ |

___________________________________ |

||

____________________________________________ |

___________________________________ |

||

G. |

TRANSFERS DURING DECEDENT’S LIFE |

|

|

|

Description |

Date of Death Value |

|

_____________________________________________ |

___________________________________ |

||

_____________________________________________ |

___________________________________ |

||

H. |

POWERS OF APPOINTMENT |

|

|

|

Description |

Date of Death Value |

|

_____________________________________________ |

___________________________________ |

||

_____________________________________________ |

___________________________________ |

||

I. |

ANNUITIES |

|

|

|

Description |

Date of Death Value |

|

_____________________________________________ |

___________________________________ |

||

_____________________________________________ |

___________________________________ |

||

CAUSE OF ACTION for decedent’s wrongful death and for conscious pain and suffering, as well as any other type of action.

|

Court in which |

Index |

Amount |

Description |

Action Pending |

Number |

Demanded |

__________________ |

____________________ |

_______________ |

_________________ |

__________________ |

____________________ |

_______________ |

_________________ |

| Fact Name | Fact Description |

|---|---|

| Governing Law | The form is governed by Rule §207.20(a) of the Surrogate’s Court of New York. |

| Purpose | This form lists the assets of a deceased individual for estate management and tax purposes. |

| Fiduciary Certification | The fiduciary or attorney must certify the accuracy of the information provided. |

| Document Attachment | A detailed list of assets must be attached, along with specific forms (ET-90, TT-385, 706, or 706NA). |

| Secrecy Waiver | If Form ET-90 is attached, all rights to secrecy under Tax Law §994 are waived. |

| Date Requirements | The form requires the Date of Death and Date of Letters for proper processing. |

| Asset Categories | It outlines categories like Real Estate, Stocks, Bonds, Mortgages, and Insurance. |

| Total Assets | The total gross assets must be calculated and documented in specific sections. |

| Cause of Action | The form allows indication of any pending cause of action, including wrongful death claims. |

| Certification Date | The attorney must certify the form, including the date of signature for validation. |

The next steps involve accurately completing the Court Inventory form to ensure all necessary information is provided for the decedent's estate. This completion requires attention to detail and careful representation of assets according to established guidelines.

What is the purpose of the Court Inventory form?

The Court Inventory form is designed to provide a clear and organized summary of the assets of a deceased individual's estate. It serves as a vital record for tax purposes and helps the court identify the total value of the estate. This form must be accurately completed by a fiduciary or an attorney representing the estate.

Who is required to complete the Court Inventory form?

Typically, a fiduciary or an appointed attorney for the estate must complete this form. A fiduciary could be an executor or administrator tasked with managing the estate. It’s their job to accurately account for all assets and liabilities of the deceased person.

What information is needed to fill out the Court Inventory form?

To complete the form, you will require detailed information about the deceased's assets, including but not limited to real estate, stocks, bonds, bank accounts, insurance policies, and any jointly owned properties. Information regarding outstanding debts and transfers made during the decedent's life is also necessary.

Are there any documents required to accompany the Court Inventory form?

Yes, you need to attach specific documents such as a detailed list of assets or, alternatively, copies of certain forms like Form ET-90, Form TT-385, or Form 706/706NA. The completion of the form ensures transparency and accuracy in the accounting of the estate.

What should I do if there are changes to the beneficiary's address?

If there are changes to the address of a fiduciary or beneficiary, it’s crucial to include the updated address on the form. Maintaining accurate contact information helps streamline communication with the court and ensures that all parties are notified of any important developments.

What happens if I fail to complete the Court Inventory form accurately?

Inaccurate or incomplete forms can lead to delays in the proceedings. The court may request revisions or additional documentation, which can prolong the process of estate settlement. In some cases, it may even lead to legal complications, so it’s critical to fill out the form with care and precision.

Where should the completed Court Inventory form be submitted?

The completed Court Inventory form should be submitted to the Surrogate’s Court in the appropriate county where the estate is being administered. It’s important to ensure it’s filed by any deadlines set by the court to avoid potential complications.

Not Including All Assets: Failing to list all assets, including both probate and non-probate assets, can lead to incomplete inventory submissions.

Incorrect Valuation: Listing incorrect values for assets can create issues during the administrative and tax processes associated with the estate.

Missing Documentation: Forgetting to attach required documents, such as Form ET-90 or a detailed asset list, may delay the inventory process.

Improper Signatures: Not signing the form where indicated or having unauthorized individuals sign can invalidate the submission.

Incorrect or Missing Dates: Failing to provide accurate dates of death or letters can hinder the processing of the court inventory.

Listing Jointly Owned Property Incorrectly: Not reporting jointly owned property in the correct section can lead to valuation problems and misunderstandings.

Forgetting to Include Personal Property: Neglecting to incorporate personal or miscellaneous property can result in an incomplete inventory.

Inaccurate Cause of Action Information: Providing incorrect details about ongoing legal actions related to the decedent can complicate estate management.

Not Updating Fiduciary Information: Failing to provide current contact information for the fiduciary can frustrate communication with the court.

Not Reviewing the Completed Form: Skipping a final review of the inventory form before submission can lead to overlooked errors.

The Court Inventory form is a vital document in the Surrogate’s Court of New York. It lists the assets of a deceased person's estate for tax purposes. Several other forms and documents often accompany the Court Inventory to provide a fuller picture of the estate's financial situation. Here are a few of those documents:

Including these documents with the Court Inventory form ensures a comprehensive understanding of the estate's financial landscape. This clarity is crucial for heirs and beneficiaries navigating the next steps.

The Form ET-90 is similar to the Court Inventory form in that both serve as mechanisms to report the assets and financial matters of a deceased person’s estate. The ET-90, specifically, is used to report information to the New York State Department of Taxation and Finance. This document necessitates a detailed declaration of the deceased's assets for tax purposes, paralleling the Court Inventory form's focus on a comprehensive asset list. Each document aims to ensure accurate reporting and compliance with state regulations regarding the estate.

The Form TT-385 also shares similarities with the Court Inventory form. It is utilized to assess the estate of a deceased for the taxation process. Like the inventory form, TT-385 compiles pertinent asset information and aids in determining the estate's overall value for tax obligations. The requirements laid out in both documents emphasize thoroughness in asset disclosure to fulfill legal and tax-related responsibilities.

Form 706, or the United States Estate (and Generation-Skipping Transfer) Tax Return, mirrors certain elements of the Court Inventory form by providing a detailed account of the decedent’s gross estate for federal tax assessment. While Form 706 primarily serves federal tax purposes, it still requires asset enumeration that is akin to the asset listing required in the Court Inventory form. Both documents function as necessary reports that help administer estate settlement and tax assessments within their respective jurisdictions.

Similarly, Form 706NA, designated for non-resident aliens, aligns with the Court Inventory form in that it documents the gross estate for tax evaluation at the federal level. Although this form is tailored for a specific demographic, like the Court Inventory, it emphasizes the importance of a complete asset inventory, ensuring adequate compliance with tax regulations upon the decedent's passing.

The Last Will and Testament documents also bear resemblance to the Court Inventory form. These documents serve to outline the distribution of the deceased’s assets upon death, which mandates an understanding of what assets exist within the estate. In both cases, the listing of assets is an essential component, establishing clarity and order in handling the estate and its beneficiary designations.

The Asset Disclosure Statement functions similarly to the Court Inventory form by providing a comprehensive list of the assets held by the deceased at the time of death. This document plays an important role in ensuring transparency among interested parties and authorities, promoting an accurate understanding of the estate's financial standing, just like the inventory form does within the probate process.

The Declaration of Homestead can also be compared to the Court Inventory form. The Declaration of Homestead helps ascertain what property is protected under homestead laws, which often is an essential part of the estate. Both documents require detailed information about real property, emphasizing a clear picture of available assets that need to be managed after death.

Lastly, the Financial Affidavit shares elements with the Court Inventory form, as both documents require a detailed breakdown of assets, liabilities, and other financial obligations. The purpose of the Financial Affidavit is often to establish economic circumstances for legal proceedings, while the Court Inventory focuses on calculating the deceased's estate value. Nonetheless, both provide a comprehensive approach to understanding the financial landscape, whether during life or posthumously.

When filling out the Court Inventory form, it is important to follow certain guidelines to ensure accuracy and compliance. Below are essential points to consider:

Misconceptions about the Court Inventory form can lead to confusion for those managing an estate. Understanding these misconceptions is crucial for accurate preparation.

Completing the Court Inventory form requires careful attention to detail. Here are some key takeaways to ensure you meet all the necessary requirements:

Following these steps will help streamline the process and reduce potential issues with your estate filing.