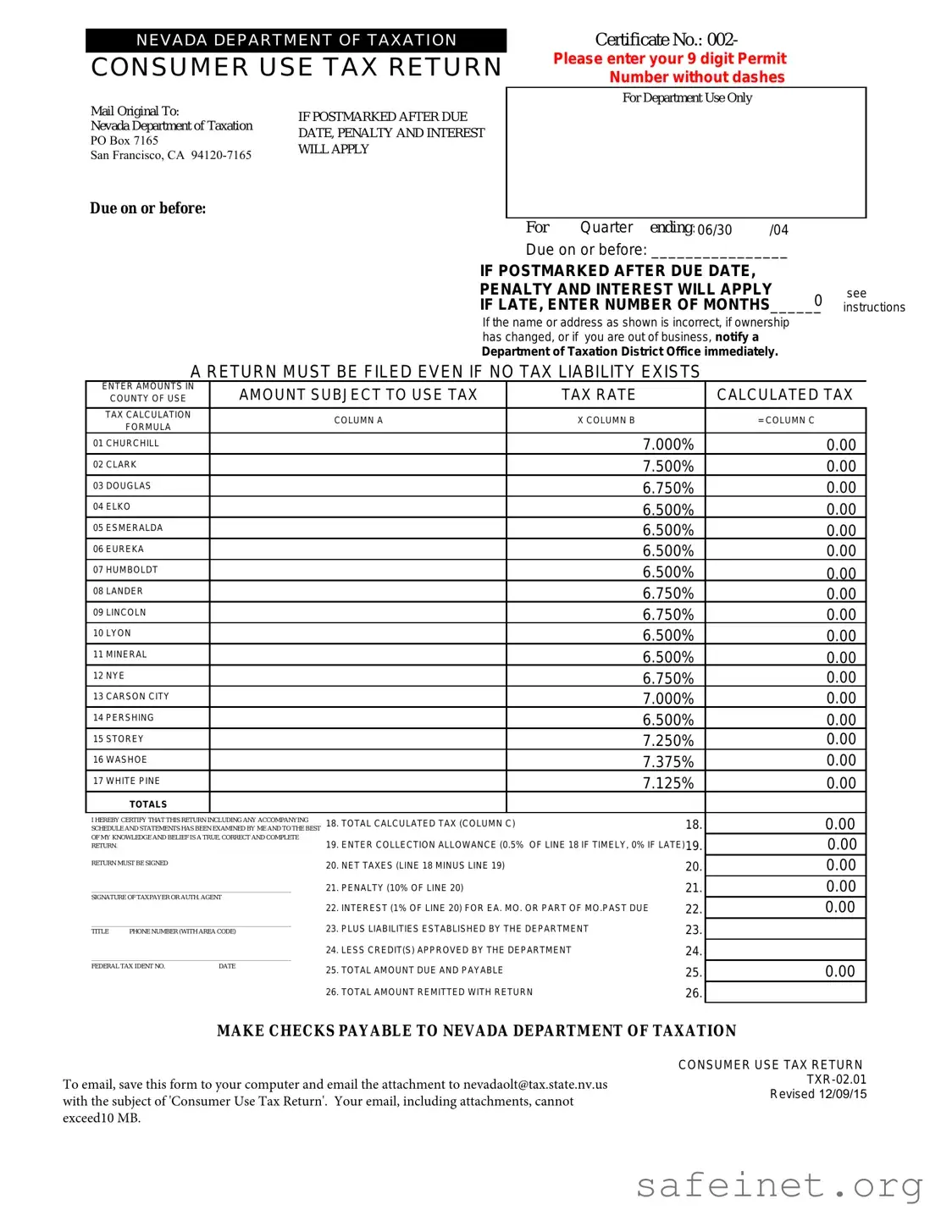

The Consumer Use Tax Return form for Nevada is an essential document for individuals and businesses that have made purchases subject to use tax without paying Nevada sales tax. This form must be submitted to the Nevada Department of Taxation by the due date indicated on the form. It includes critical sections such as the amount subject to use tax, applicable tax rates for different counties, and the total calculated tax. Taxpayers must report their total purchases, calculate the tax owed, and sign the return to certify its accuracy. If the return is postmarked late, penalties and interest will apply, emphasizing the importance of timely submission. The form also allows for the reporting of any prior liabilities or credits, ensuring that taxpayers have a clear understanding of their tax obligations. Completing this return accurately is crucial, as it affects both compliance and potential penalties.

NEVADA DEPARTMENT OF TAXATION

CONSUMER USE TAX RETURN

Mail Original To: |

IF POSTMARKED AFTER DUE |

Nevada Department of Taxation |

DATE, PENALTY AND INTEREST |

|

PO Box 7165 |

||

WILL APPLY |

||

San Francisco, CA |

||

|

Due on or before:

Certificate No.: 002-

Please enter your 9 digit Permit Number without dashes

For Department Use Only

For Quarter ending: 06/30 /04

Due on or before: ________________

IF POSTMARKED AFTER DUE DATE, PENALTY AND INTEREST WILL APPLY

IF LATE, ENTER NUMBER OF MONTHS 0

______

If the name or address as shown is incorrect, if ownership has changed, or if you are out of business, notify a

Department of Taxation District Office immediately.

see instructions

A RETURN MUST BE FILED EVEN IF NO TAX LIABILITY EXISTS

ENTER AMOUNTS IN |

AMOUNT SUBJECT TO USE TAX |

|

TAX RATE |

|

|

CALCULATED TAX |

|

COUNTY OF USE |

|

|

|

||||

|

|

|

|

|

|

|

|

TAX CALCULATION |

|

COLUMN A |

|

X COLUMN B |

|

|

= COLUMN C |

FORMULA |

|

|

|

|

|||

|

|

|

|

|

|

|

|

01 CHURCHILL |

|

|

|

|

7.000% |

0.00 |

|

02 CLARK |

|

|

|

|

7.500% |

0.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

03 DOUGLAS |

|

|

|

|

6.750% |

0.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

04 ELKO |

|

|

|

|

6.500% |

0.00 |

|

|

|

|

|

|

|||

05 ESMERALDA |

|

|

|

|

6.500% |

0.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

06 EUREKA |

|

|

|

|

6.500% |

0.00 |

|

|

|

|

|

|

|||

07 HUMBOLDT |

|

|

|

|

6.500% |

0.00 |

|

|

|

|

|

|

|||

08 LANDER |

|

|

|

|

6.750% |

0.00 |

|

|

|

|

|

|

|||

09 LINCOLN |

|

|

|

|

6.750% |

0.00 |

|

|

|

|

|

|

|||

10 LYON |

|

|

|

|

6.500% |

0.00 |

|

|

|

|

|

|

|

|

|

11 MINERAL |

|

|

|

|

6.500% |

0.00 |

|

|

|

|

|

|

|||

12 NYE |

|

|

|

|

6.750% |

0.00 |

|

|

|

|

|

|

|||

13 CARSON CITY |

|

|

|

|

7.000% |

0.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 PERSHING |

|

|

|

|

6.500% |

0.00 |

|

|

|

|

|

|

|||

15 STOREY |

|

|

|

|

7.250% |

0.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16 WASHOE |

|

|

|

|

7.375% |

0.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

17 WHITE PINE |

|

|

|

|

7.125% |

0.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTALS |

|

|

|

|

|

|

|

I HEREBY CERTIFY THAT THIS RETURN INCLUDING ANY ACCOMPANYING |

18. TOTAL CALCULATED TAX (COLUMN C) |

|

|

18. |

0.00 |

||

SCHEDULE AND STATEMENTS HAS BEEN EXAMINED BY ME AND TO THE BEST |

|

|

|||||

OF MY KNOWLEDGE AND BELIEF IS A TRUE, CORRECT AND COMPLETE |

19. ENTER COLLECTION ALLOWANCE (0.5% OF LINE 18 IF TIMELY, 0% IF LATE)19. |

0.00 |

|||||

RETURN. |

|

||||||

RETURN MUST BE SIGNED |

|

20. NET TAXES (LINE 18 MINUS LINE 19) |

|

|

20. |

0.00 |

|

|

|

|

|

||||

_______________________________________________________________ |

21. PENALTY (10% OF LINE 20) |

|

|

21. |

0.00 |

||

SIGNATURE OF TAXPAYER OR AUTH. AGENT |

22. INTEREST (1% OF LINE 20) FOR EA. MO. OR PART OF MO.PAST DUE |

22. |

0.00 |

||||

|

|

||||||

_______________________________________________________________ |

23. PLUS LIABILITIES ESTABLISHED BY THE DEPARTMENT |

|

23. |

|

|||

TITLE PHONE NUMBER (WITH AREA CODE) |

|

|

|||||

_______________________________________________________________ |

24. LESS CREDIT(S) APPROVED BY THE DEPARTMENT |

|

24. |

|

|||

FEDERAL TAX IDENT NO. |

DATE |

25. TOTAL AMOUNT DUE AND PAYABLE |

|

|

25. |

0.00 |

|

|

|

|

|

||||

|

|

26. TOTAL AMOUNT REMITTED WITH RETURN |

|

|

26. |

|

|

MAKE CHECKS PAYABLE TO NEVADA DEPARTMENT OF TAXATION

*001063004000000*To email, save this form to your computer and email the attachment to [email protected] with the subject of 'Consumer Use Tax Return'. Your email, including attachments, cannot exceed10 MB.

CONSUMER USE TAX RETURN

CONSUMER USE TAX RETURN INSTRUCTIONS

COLUMN A. Amount subject to Use Tax: Enter total purchases subject to use tax on appropriate county line. All purchases of tangible personal property on which no Nevada sales tax has been paid must be entered here.

COLUMN C. Calculated Tax: Multiply taxable amount(s) (Column A) by tax rate(s) (Column B) and enter in Column C.

Note: If you have a contract exemption, give contract exemption number.

TOTALS: Enter total amount of Column A.

LINE 18. Total calculated tax from column C

LINE 19. Collection allowance: Compute 1/2% (or .005) X Line 18 if return and taxes are paid as postmarked on or before the due date as shown on the face of the return. If not postmarked by the due date the collection allowance is not allowed.

LINE 20. Net Taxes Due: Subtract Line 19 from Line 18.

LINE 21. If this return will not be postmarked, and the taxes paid on or before the due date as shown on the face of this

return, a 10% penalty will be assessed. Enter 10% (or .10) times Line 20.

LINE 22. If this return will not be postmarked and the taxes paid on or before the due date as shown on the face of this return, enter 1.5% times line 20 for each month or fraction of a month late, prior to 7/1/99. After 7/1/99, use 1% for each month or fraction of a month late.

LINE 23. Enter any amount due for prior reporting periods for which you have received a Department of Taxation debit notice. Monthly notices received from the Department are not cumulative.

LINE 24. Enter amount due to you for overpayment made in prior reporting periods for which you have received a Department of Taxation credit notice. Monthly notices received from the Department are not cumulative. Do not take the credit if you have applied for a refund.

NOTE: Only credits established by the Department may be used.

LINE 25. Total Taxes Due and Payable: Add Line 20, 21, 22, and 23. Subtract amount on Line 24. Enter total.

LINE 26. Total Amount Remitted: Enter total amount paid with this return.

PLEASE COMPLETE THE SIGNATURE PORTION OF THE RETURN AND RETURN IN THE ENVELOPE PROVIDED.

If you have questions concerning this return, please call one of the Department of Taxation offices listed below.

Carson City (775) |

Las Vegas (702) |

Reno (775) |

CONSUMER USE TAX RETURN INSTRUCTIONS

Revised 12/09/15

| Fact Name | Fact Description |

|---|---|

| Governing Law | The Consumer Use Tax Return is governed by Nevada Revised Statutes (NRS) 372.185. |

| Filing Requirement | A return must be filed even if there is no tax liability. |

| Due Date | The return is due on or before the specified date for the quarter ending. |

| Penalties | If postmarked after the due date, penalties and interest will apply. |

| Collection Allowance | A collection allowance of 0.5% is available if the return is timely filed. |

| Tax Calculation | Calculated tax is determined by multiplying the taxable amount by the applicable tax rate. |

| Signature Requirement | The return must be signed by the taxpayer or an authorized agent. |

| Contact Information | Questions can be directed to the Department of Taxation offices in Carson City, Las Vegas, or Reno. |

| Email Submission | The form can be emailed to [email protected] with specific subject line instructions. |

Filling out the Consumer Use Tax Return form for Nevada is an essential task for individuals and businesses that have made purchases subject to use tax. Completing this form accurately ensures compliance with state tax laws. Below are the steps to guide you through the process of filling out the form.

What is the Consumer Use Tax Return in Nevada?

The Consumer Use Tax Return is a form that individuals and businesses in Nevada must complete if they have purchased tangible personal property without paying Nevada sales tax. This form ensures that the appropriate use tax is reported and paid to the state. It applies to items purchased from out-of-state sellers or online vendors where sales tax was not collected at the time of purchase.

When is the Consumer Use Tax Return due?

The return is due on or before the last day of the month following the end of each quarter. For example, if you are filing for the quarter ending June 30, the return must be postmarked by July 31. It's crucial to submit the form on time to avoid penalties and interest charges. If the return is postmarked after the due date, penalties will apply.

How do I calculate the amount of use tax I owe?

To calculate the use tax, first, determine the total amount of your purchases that are subject to use tax. This amount should be entered in Column A of the form. Then, multiply that figure by the applicable tax rate for your county, which is listed in Column B. The result will be entered in Column C as the calculated tax. Ensure you review the tax rates for your specific county, as they can vary.

What if I have no tax liability?

Even if you have no tax liability, you are still required to file a Consumer Use Tax Return. It is essential to report that no taxes are due by completing the form and submitting it. This helps maintain compliance with state tax laws and avoids potential issues in the future.

What should I do if my information has changed?

If there are any changes to your name, address, or business ownership, you must notify the Department of Taxation immediately. This can be done by contacting a District Office. Keeping your information current ensures that you receive any important notifications and helps avoid complications with your tax filings.

Failing to enter the correct Permit Number. Ensure that you include the 9-digit number without dashes.

Not filing a return even if there is no tax liability. A return must be submitted regardless of whether taxes are owed.

Neglecting to check for incorrect name or address. If there are changes in ownership or if you are out of business, notify the Department of Taxation immediately.

Incorrectly calculating the taxable amount. Ensure that all purchases subject to use tax are accurately reported in Column A.

Forgetting to apply the correct tax rate. Use the appropriate rate for your county as listed in the form.

Failing to sign the return. The form must be signed by the taxpayer or an authorized agent.

Missing the postmark deadline. If the return is postmarked after the due date, penalties and interest will apply.

Not calculating the collection allowance correctly. This is only applicable if the return is timely filed.

Overlooking prior liabilities or credits. Make sure to enter any amounts due from previous reporting periods.

Failing to include the total amount remitted with the return. Ensure that you accurately report the total payment.

The Consumer Use Tax Return form is an essential document for individuals and businesses in Nevada to report and pay taxes on goods purchased without paying sales tax. However, several other forms and documents often accompany this return. Understanding these additional documents can help ensure compliance and streamline the tax filing process.

By being aware of these additional forms and documents, you can better navigate the tax landscape in Nevada. This knowledge not only aids in compliance but also helps you take advantage of any exemptions or refunds you may be eligible for.

The Consumer Use Tax Return form from Nevada shares similarities with the Sales Tax Return form. Both documents require taxpayers to report tax liabilities on transactions involving tangible personal property. While the Sales Tax Return focuses on sales tax collected from customers, the Consumer Use Tax Return is designed for individuals or businesses that have purchased items without paying sales tax. This distinction is crucial for ensuring compliance with state tax regulations.

Another document akin to the Consumer Use Tax Return is the Property Tax Return. Both forms serve to report tax obligations, but they pertain to different types of taxes. The Property Tax Return is used to declare ownership of real property and assess its value for taxation purposes. In contrast, the Consumer Use Tax Return addresses the use tax on goods purchased out of state or online, emphasizing the responsibility of the buyer rather than the seller.

The Business License Application is also similar in that it requires individuals or businesses to provide specific information to comply with state regulations. Both documents necessitate accurate reporting of business activities, although the Business License Application focuses on obtaining permission to operate legally within the state. The Consumer Use Tax Return, however, centers on tax liabilities related to purchases made without sales tax being paid.

The Annual Income Tax Return can be compared to the Consumer Use Tax Return as both require taxpayers to report their financial activities to the state. While the Income Tax Return assesses overall income and applicable taxes, the Consumer Use Tax Return specifically targets tax obligations arising from purchases of tangible goods. Each document plays a vital role in the broader context of state taxation.

The Excise Tax Return is another document that parallels the Consumer Use Tax Return. Both forms involve reporting taxes owed to the state, but they apply to different circumstances. The Excise Tax Return is primarily concerned with specific goods, such as alcohol or tobacco, and the taxes imposed on their sale. Conversely, the Consumer Use Tax Return addresses the tax responsibilities of individuals or businesses for items purchased without sales tax.

The Franchise Tax Return is similar in function to the Consumer Use Tax Return, as both require reporting of tax liabilities. The Franchise Tax Return is applicable to businesses operating as corporations or limited liability companies, focusing on the privilege of doing business in the state. The Consumer Use Tax Return, on the other hand, is geared towards individuals and businesses that have made purchases without sales tax, emphasizing the tax owed on those transactions.

The Nonprofit Organization Tax Exemption Application shares a connection with the Consumer Use Tax Return in terms of compliance with tax regulations. Both documents require detailed information about the organization’s activities. The Tax Exemption Application seeks to establish eligibility for tax-exempt status, while the Consumer Use Tax Return ensures that nonprofits report any taxable purchases accurately, maintaining transparency with the state.

The Use Tax Registration form is closely related to the Consumer Use Tax Return. Both documents are essential for individuals and businesses that need to report use tax obligations. The Use Tax Registration form is typically completed to establish a taxpayer's responsibility for paying use tax, while the Consumer Use Tax Return is filed to report the actual tax owed based on purchases made. Together, they facilitate compliance with state tax laws.

Finally, the Tax Credit Application can be compared to the Consumer Use Tax Return. Both documents involve reporting to the state, but they serve different purposes. The Tax Credit Application allows taxpayers to claim credits for various eligible expenses or activities, potentially reducing their overall tax liability. In contrast, the Consumer Use Tax Return focuses on reporting tax owed for purchases made without sales tax, ensuring that all tax obligations are met.

When filling out the Consumer Use Tax Return for Nevada, it’s important to follow guidelines to ensure accuracy and compliance. Here’s a list of things you should and shouldn't do:

Understanding the Consumer Use Tax Return in Nevada can be tricky, and misconceptions can lead to mistakes. Here are some common misunderstandings:

Being informed helps you navigate the process smoothly. If you're unsure, consider reaching out to a tax professional or the Nevada Department of Taxation for guidance.

Here are key takeaways regarding the Consumer Use Tax Return form for Nevada: