The Colorado 104 form, officially known as the Colorado Individual Income Tax Return, serves as a crucial document for residents and non-residents alike who need to report their annual income for state tax purposes. This form accommodates full-year residents, part-year residents, and even non-residents. It collects essential personal information such as names, Social Security numbers, and marital status right at the top. Subsequently, individuals must calculate their federal taxable income and make necessary adjustments with additions or subtractions specific to Colorado tax laws. Taxpayers will enter their total income and report various additions, including state income tax deductions or business interest expense deductions. The form also requires individuals to address possible credits, ensuring that taxpayers can maximize their potential tax benefits. After calculating the net tax amount due or refundable, the form concludes with sections for reporting and requesting direct deposits, providing a seamless experience for receiving refunds. It’s important to ensure all relevant supporting documents accompany the form, particularly if claiming certain credits or deductions, to facilitate accurate and timely processing by the Colorado Department of Revenue.

*200104==19999*

DR 0104 (10/19/20)

COLORADO DEPARTMENT OF REVENUE

Tax.Colorado.gov

Page 1 of 4

(0013)

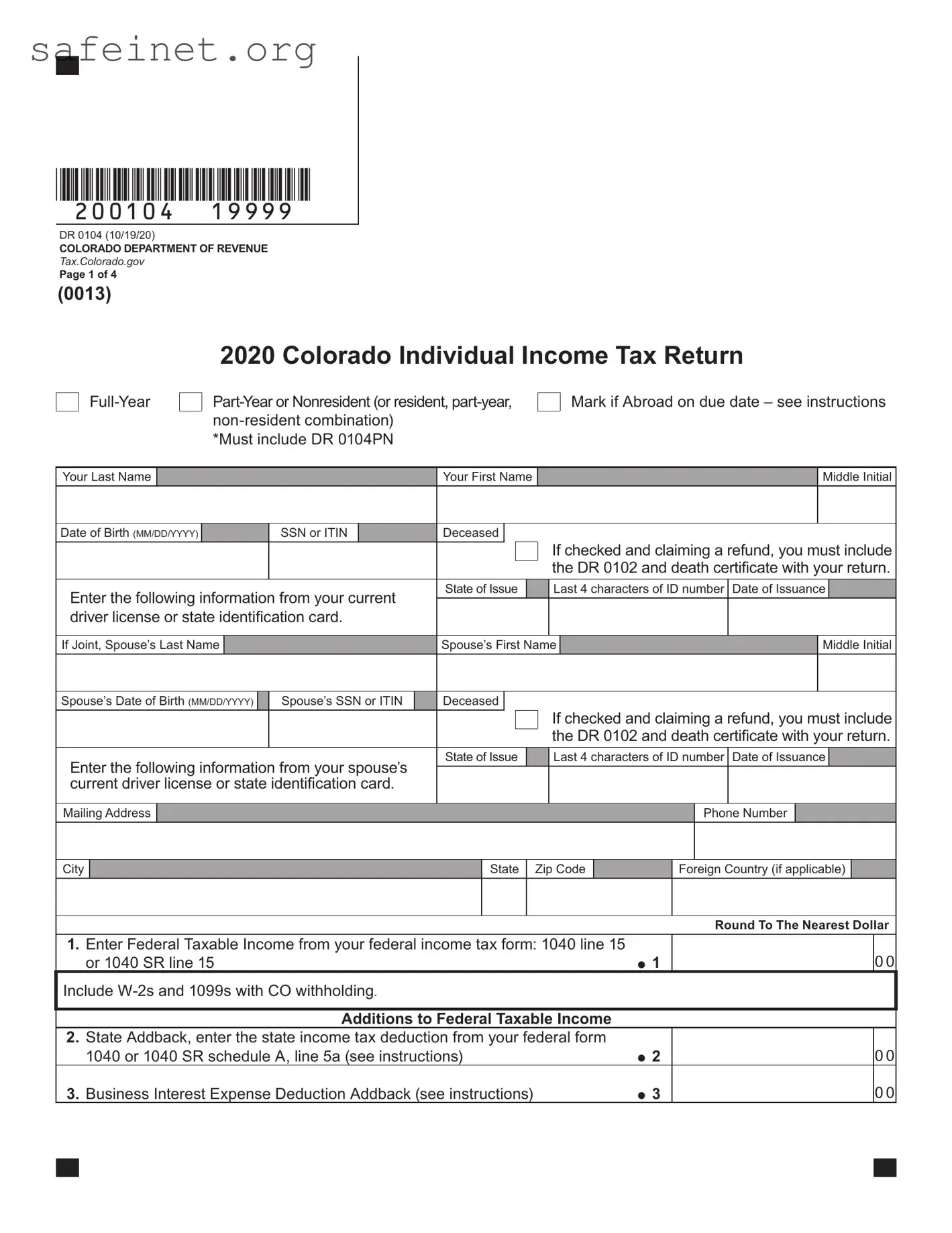

2020 Colorado Individual Income Tax Return

*Must include DR 0104PN

Mark if Abroad on due date – see instructions

Your Last Name |

|

|

|

|

|

|

|

Your First Name |

|

|

|

|

Middle Initial |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Date of Birth (MM/DD/YYYY) |

|

|

SSN or ITIN |

|

|

Deceased |

|

|

|

|

If checked and claiming a refund, you must include |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

the DR 0102 and death certificate with your return. |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Enter the following information from your current |

State of Issue |

|

|

Last 4 characters of ID number |

Date of Issuance |

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||

driver license or state identification card. |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If Joint, Spouse’s Last Name |

|

|

|

|

|

Spouse’s First Name |

|

|

Middle Initial |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Spouse’s Date of Birth (MM/DD/YYYY) |

|

Spouse’s SSN or ITIN |

|

Deceased |

|

|

|

|

If checked and claiming a refund, you must include |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

the DR 0102 and death certificate with your return. |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Enter the following information from your spouse’s |

State of Issue |

|

|

Last 4 characters of ID number |

Date of Issuance |

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||

current driver license or state identification card. |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mailing Address

City

|

|

|

|

Phone Number |

State |

|

Zip Code |

|

Foreign Country (if applicable) |

|

|

|||

|

|

|

|

|

Round To The Nearest Dollar

1.Enter Federal Taxable Income from your federal income tax form: 1040 line 15

or 1040 SR line 15 |

1 |

Include

Additions to Federal Taxable Income

2.State Addback, enter the state income tax deduction from your federal form

|

1040 or 1040 SR schedule A, line 5a (see instructions) |

2 |

3. Business Interest Expense Deduction Addback (see instructions) |

3 |

|

|

|

|

|

|

|

0 0

00

00

*200104==29999* |

|

DR 0104 (10/19/20) |

|

|

|

||

|

|

|

|

||||

|

Page 2 of 4 |

|

|

|

|||

|

|

|

|

COLORADO DEPARTMENT OF REVENUE |

|

|

|

|

|

|

|

Tax.Colorado.gov |

|

|

|

|

|

|

|

|

|

||

Name |

|

|

|

|

SSN or ITIN |

||

|

|

|

|

|

|

||

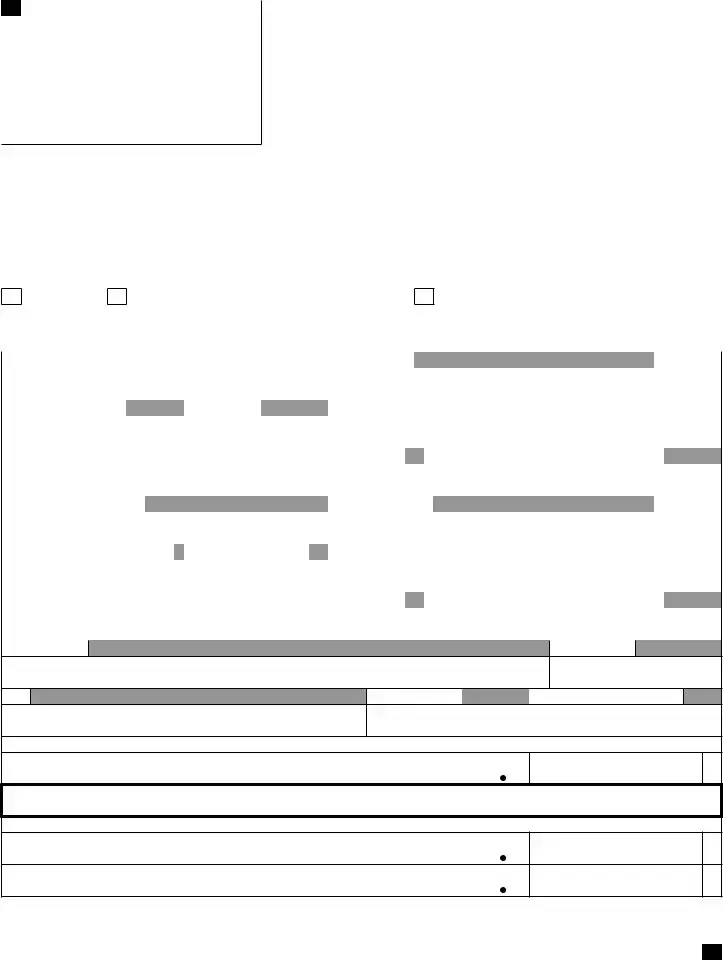

4. |

Excess Business Loss Addback (see instructions) |

4 |

|

|

|||

5. |

Net Operating Loss Addback (see instructions) |

5 |

|

|

|||

6. |

Other Additions, explain (see instructions) |

|

|

6 |

|

|

|

Explain:

7. Subtotal, sum of lines 1 through 6 |

7 |

Colorado Subtractions

8.Subtractions from the DR 0104AD Schedule, line 20, you must submit the

DR 0104AD schedule with your return. |

8 |

9. Colorado Taxable Income, subtract line 8 from line 7 |

9 |

Tax, Prepayments and Credits: see 104 Book for

10.Colorado Tax from tax table or the DR 0104PN line 36, you must submit

the DR 0104PN with your return if applicable. |

10 |

11.Alternative Minimum Tax from the DR 0104AMT line 8, you must submit the

|

DR 0104AMT with your return. |

11 |

12. |

Recapture of prior year credits |

12 |

13. |

Subtotal, sum of lines 10 through 12 |

13 |

14.Nonrefundable Credits from the DR 0104CR line 43, the sum of lines 14, 15, and 16

cannot exceed line 13, you must submit the DR 0104CR with your return. |

14 |

15.Total Nonrefundable Enterprise Zone credits used – as calculated,

or from the DR 1366 line 87, the sum of lines 14, 15, and 16 cannot exceed line 13,

you must submit the DR 1366 with your return. |

15 |

16.Strategic Capital Tax Credit from DR 1330, the sum of lines 14, 15, and 16 cannot

exceed line 13, you must submit the DR 1330 with your return. |

16 |

17. Net Income Tax, sum of lines 14, 15, and 16. Subtract that sum from line 13. |

17 |

18.Use Tax reported on the DR 0104US schedule line 7, you must submit

the DR 0104US with your return. |

18 |

19. Net Colorado Tax, sum of lines 17 and 18 |

19 |

20.CO Income Tax Withheld from

and/or 1099s claiming Colorado withholding with your return. |

20 |

21. |

21 |

22.Estimated Tax Payments, enter the sum of the quarterly payments

|

remitted for this tax year |

|

|

|

|

22 |

|

23. Extension Payment remitted with the DR |

|

|

23 |

||||

24. Other Prepayments: |

|

DR 0104BEP |

|

DR 0108 |

|

DR 1079 24 |

|

|

|

|

|||||

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00

00

00

0 0

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

0 0

*200104==39999* |

|

DR 0104 (10/19/20) |

|

|

|||

|

Page 3 of 4 |

||

|

|

|

COLORADO DEPARTMENT OF REVENUE |

|

|

|

Tax.Colorado.gov |

Name |

|

|

SSN or ITIN |

|

|

||

25.Gross Conservation Easement Credit from the DR 1305G line 33, you must

submit the DR 1305G with your return. |

25 |

26.Innovative Motor Vehicle Credit from the DR 0617, you must submit each

DR 0617 with your return. |

26 |

27.Refundable Credits from the DR 0104CR line 9, you must submit the

DR 0104CR with your return. |

27 |

28. Subtotal, sum of lines 20 through 27 |

28 |

29.Federal Adjusted Gross Income from your federal income tax form: 1040 line 11,

|

or 1040 SR line 11 |

29 |

30. |

Overpayment, if line 28 is greater than line 19 then subtract line 19 from line 28 |

30 |

31. |

Estimated Tax Credit Carryforward to 2021 first quarter, if any. |

31 |

00

00

00

00

00

00

00

If you have an overpayment on line 32 below and would like to donate all or a portion of your overpayment to a qualified Colorado charity, include Form DR 0104CH to contribute.

32. Refund, subtract line 31 from line 30 (see instructions) |

32 |

0 0

Direct Deposit

Routing Number

Account Number

Type:

Checking

Savings

CollegeInvest 529

For questions regarding CollegeInvest direct deposit or to open an account, visit CollegeInvest.org or call

33. |

Net Tax Due, subtract line 28 from line 19 |

33 |

34. |

Delinquent Payment Penalty (see instructions) |

34 |

35. |

Delinquent Payment Interest (see instructions) |

35 |

36.Estimated Tax Penalty, you must submit the DR 0204 with your return.

(see instructions) |

36 |

37. Amount You Owe, sum of lines 33 through 36 |

37 |

00

00

00

00

The State may convert your check to a

*200104==49999*

DR 0104 (10/19/20)

COLORADO DEPARTMENT OF REVENUE

Tax.Colorado.gov

Page 4 of 4

Name

SSN or ITIN

Third Party Designee

Do you want to allow another person to discuss this return and any related information with the Colorado Department of Revenue? See the instructions.

No

Yes. Complete the following:

Designee’s Name |

|

|

|

|

|

|

Phone Number |

|

|

|

||||

|

|

|||||||||||||

Sign Below Under penalties of perjury, I declare that to the best of my knowledge and belief, this return is true, correct and complete. |

||||||||||||||

Your Signature |

|

|

|

|

|

|

|

|

|

Date (MM/DD/YY) |

|

|||

|

|

|

|

|

|

|

|

|

|

|

||||

Spouse’s Signature. If joint return, BOTH must sign. |

|

|

|

|

|

Date (MM/DD/YY) |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|||||

Paid Preparer’s Name |

|

|

|

|

|

Paid Preparer’s Phone |

|

|

||||||

|

|

|

|

|

|

|

|

|||||||

Paid Preparer’s Address |

|

|

City |

|

State |

|

Zip |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

File and pay at: Colorado.gov/RevenueOnline

If you are filing this return with a check or payment, please mail the return to:

COLORADO DEPARTMENT OF REVENUE Denver, CO

If you are filing this return without a check or payment, please mail the return to:

COLORADO DEPARTMENT OF REVENUE Denver, CO

These addresses and zip codes are exclusive to the Colorado Department of Revenue, so a street address is not required.

| Fact Name | Details |

|---|---|

| Form Purpose | The Colorado 104 form is used for filing individual income tax returns for full-year, part-year, or non-resident taxpayers. |

| Governing Law | This form is governed under Colorado Revised Statutes Title 39, Taxation, specifically § 39-22-104, which outlines requirements for individual income tax returns. |

| Supporting Documents | Taxpayers must include various supporting documents, such as W-2s and 1099s, with their form to validate their income. |

| Filing Methods | Individuals can file the form electronically through the Colorado Department of Revenue's website or by mailing it to designated addresses. |

| Signature Requirement | Both spouses must sign the form if filing jointly. This is required for the form to be considered valid. |

The Colorado 104 form is crucial for most residents when filing their state taxes. Completing it accurately is important to ensure proper processing and avoid issues. Here are the steps to fill out the Colorado 104 form:

What is the Colorado 104 form?

The Colorado 104 form, also known as the Colorado Individual Income Tax Return, is used by individuals to report their income and calculate their state income tax obligations. This form accommodates full-year residents, part-year residents, and non-residents. It's essential for anyone who earned income in Colorado during the tax year, including those who may also file a federal income tax return.

Who needs to file the Colorado 104 form?

What information do I need to complete the Colorado 104 form?

How do I calculate my Colorado taxable income?

What are the payment options when filing the Colorado 104 form?

Are there penalties for late filing or payment?

Can I designate someone else to discuss my return with the Colorado Department of Revenue?

Neglecting to include supporting documents: When submitting the Colorado 104 form, it’s essential to attach any necessary W-2s and 1099s, particularly those showing Colorado withholding. Missing documents may delay processing or lead to rejection.

Incorrect income reporting: Federal taxable income must be accurately entered from your federal tax return. Ensuring that this number matches what’s reported on your 1040 is crucial to avoid discrepancies.

Leaving out spouse information on joint returns: If filing jointly, both parties’ details must be provided. Omitting the spouse's information can lead to significant delays or income tax inaccuracies.

Failing to double-check calculations: It's easy to miscalculate totals on the form. Take the time to verify your math, particularly on subtractions and additions, to prevent any errors that could affect your tax liability.

Inaccurate tax credit claims: When claiming credits, ensure that submissions for additional forms (like DR 0104CR for nonrefundable credits) are included. Missing these could result in lost credits and overpayment.

Improper use of estimated taxes: If claiming estimated tax payments, it’s vital to accurately report the sum of these payments. Errors can lead to penalties for underpayment or incorrectly reported amounts owed.

Ignoring the deadline: Be aware of the due date for filing. Missing this deadline could lead to penalties and interest charges. Submit your return as early as possible.

Not signing the return: One of the simplest but most overlooked mistakes is failing to sign the return. A missing signature renders the form invalid, which can cause processing delays or other issues.

The Colorado 104 form is a vital part of filing individual income tax returns in Colorado. However, several other forms and documents often accompany it to ensure thorough reporting of income and tax liabilities. Understanding these documents can aid in a smoother filing process.

Combining these forms with the Colorado 104 form allows for a complete and accurate tax return. Ensure you gather all necessary documents to facilitate your filing process, reducing potential delays or issues with your tax return.

The Colorado 104 form closely resembles the IRS Form 1040, which is the standard individual income tax return used in the United States. Both forms require detailed personal information, such as taxpayer identification numbers, marital status, and income details. Additionally, both forms allow for various adjustments to income and claim deductions or credits. The structure and purpose of the forms are fundamentally similar, as they both facilitate the reporting of income and calculation of tax liability based on federal standards.

Another document comparable to the Colorado 104 form is the state-specific Schedule A for itemized deductions. Like the Colorado 104 form, Schedule A is used to report detailed expenses that may lower taxable income. Both forms require accurate reporting of deductibles based on taxpayer eligibility. In essence, while the Colorado 104 serves a broader purpose of reporting overall income and taxing implications, the Schedule A provides a more nuanced view for itemized deductions that contribute to the final taxable amount.

The Colorado 104 form is also similar to IRS Form 1040NR, which is designed for non-resident aliens. This document, like the Colorado 104, must be completed by individuals who are not fully resident for tax purposes and need to report their U.S.-sourced income. Both forms require information on income received, applicable deductions, and tax credits. The focus on residency status impacts how taxes are calculated, and both forms require accurate representation of income to ensure compliance with respective regulations.

Additionally, the Colorado DR 0104PN form, a part-year resident tax return, parallels the Colorado 104 form in function and structure. When individuals move in or out of Colorado within a tax year, they should file the DR 0104PN to accurately report income earned during the time they resided in the state. This form allows for specific adjustments similar to those on the Colorado 104, facilitating the calculation of state tax based on prorated income and deductions.

The Colorado DR 0104CR, which is used to claim credits against Colorado income tax, shares similarities with the 104 form. Both require comprehensive information regarding credit eligibility and enumeration of refundable and nonrefundable credits. The DR 0104CR must accompany the Colorado 104 to ensure that all applicable tax credits are considered in calculating the income tax owed to Colorado, presenting a cohesive representation of tax liabilities and credits.

The Colorado DR 0104AMT form, which concerns the Alternative Minimum Tax, aligns with the Colorado 104 in its intent to provide a thorough account of tax liabilities. For individuals subject to AMT, the data reported is crucial for calculating additional tax obligations. Both forms demand detailed information, supporting schedules, and adjustments that affect overall tax calculations, ensuring that taxpayers meet their complete tax responsibilities according to state standards.

Lastly, the DR 0104US form, which notes use tax, complements the Colorado 104 form in tracking how tax applies to certain purchases. The inclusion of the DR 0104US is necessary when reporting tax owed on goods purchased outside of Colorado but used within the state. This document aligns with the comprehensive income reporting of the Colorado 104 by capturing an additional layer of tax liability that might otherwise be overlooked in general income reporting.

Things You Should Do When Filling Out the Colorado 104 Form:

Things You Shouldn't Do When Filling Out the Colorado 104 Form:

This form can be used by full-year residents, part-year residents, and non-residents. Each type of filer has specific sections to complete based on their residency status.

Even if filing online, certain supporting documents, like W-2s and any required schedules, must still be submitted as specified in the instructions for the 104 form.

Taxpayers may have different eligibility for deductions and credits based on their individual circumstances, such as income and filing status. It’s important to check which apply.

Taxpayers who anticipate owing taxes can file for an extension. However, it’s important to estimate the owed amount and pay it by the original due date to avoid penalties.

Only certain amounts, specifically those on lines where indicated, should be rounded to the nearest dollar. Be careful to follow instructions on the specific requirements for each line.

While handwritten forms can be submitted, the Colorado Department of Revenue prefers typed entries to reduce errors and improve processing times.

If a refund is claimed for a deceased taxpayer, including a death certificate is mandatory. Failing to submit this document may delay processing.

Filing does not automatically guarantee a refund. The amount depends on the taxpayer's income, deductions, credits claimed, and the total tax owed for the year.

Filing the Colorado 104 form requires precise information to ensure your tax return is accurately processed. Here are some essential points to keep in mind while completing and submitting this form:

By adhering to these guidelines, you enhance the likelihood of a smooth filing process and successful tax return for the state of Colorado.