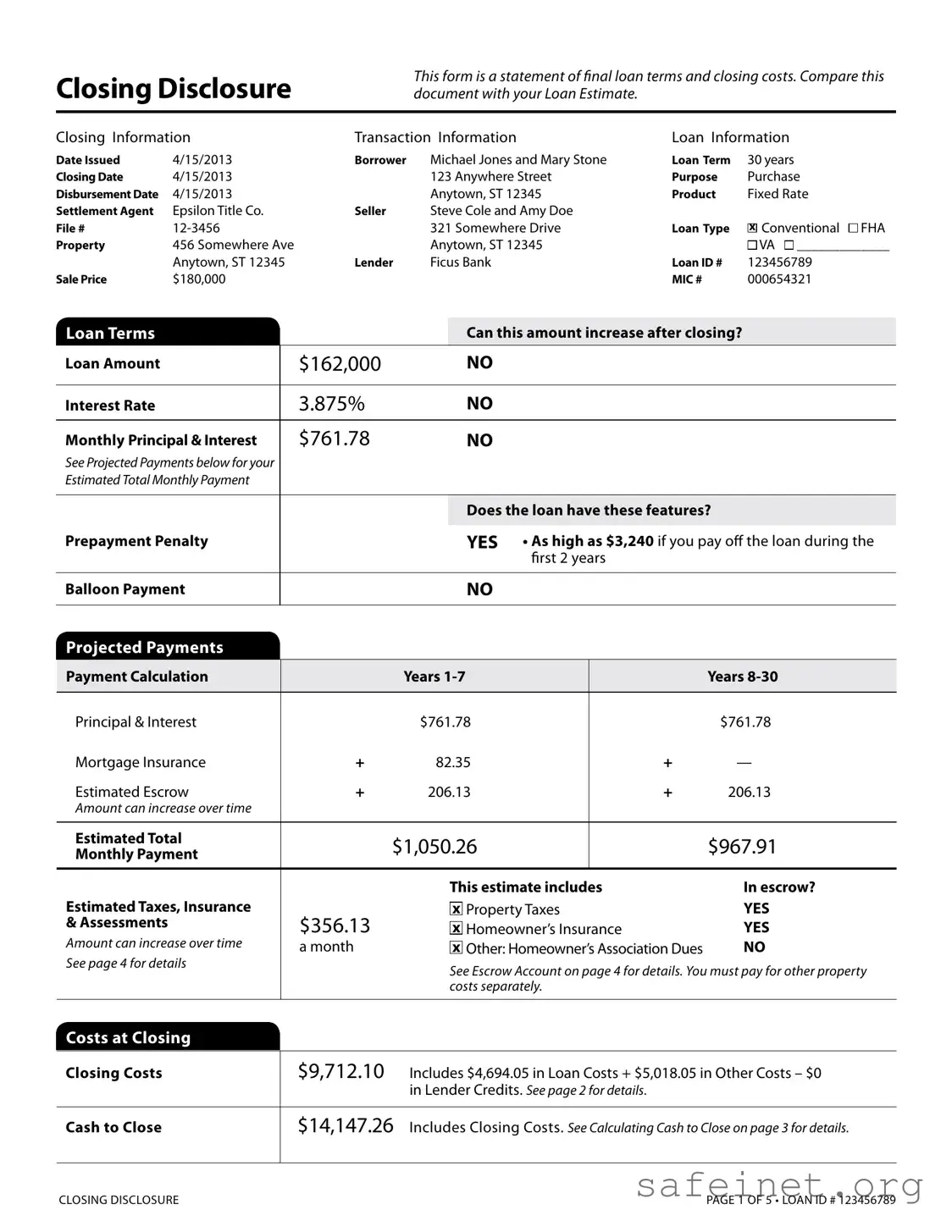

The Closing Disclosure form is a critical document that outlines the final terms of a mortgage loan and the associated closing costs. This form must be provided to borrowers at least three days before closing, allowing time to review and compare it with the Loan Estimate received earlier in the process. Key components of the Closing Disclosure include transaction details, loan information, and a breakdown of closing costs. It specifies the loan amount, interest rate, and monthly payments, while also highlighting any potential changes in costs after closing. Additionally, it details the cash required to close, including closing costs and any prepaids. The form also provides insight into the borrower’s transaction, summarizing what is due at closing and what has already been paid. Understanding this document is essential for making informed decisions and ensuring a smooth closing process.

| Fact Name | Details |

|---|---|

| Purpose | The Closing Disclosure form outlines the final loan terms and closing costs for a mortgage transaction. |

| Comparison | This document should be compared with the Loan Estimate received earlier in the mortgage process. |

| Closing Costs | The total closing costs listed on the form amount to $9,712.10, which includes various fees associated with the loan. |

| Cash to Close | The cash required to close on the loan is $14,147.26, which incorporates closing costs and other adjustments. |

| Loan Information | The form specifies key loan details, including the loan amount of $162,000 and an interest rate of 3.875%. |

| Prepayment Penalty | There is a prepayment penalty of up to $3,240 if the loan is paid off within the first two years. |

| Escrow Account | The loan will have an escrow account to manage property costs, including taxes and insurance. |

| Loan Type | This mortgage is a fixed-rate conventional loan with a term of 30 years. |

| Governing Law | The Closing Disclosure form is governed by the Truth in Lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA). |

After receiving the Closing Disclosure form, you will need to carefully fill it out to ensure that all information is accurate and complete. This form outlines your final loan terms and closing costs, so accuracy is crucial. Follow these steps to fill out the form correctly.

What is the Closing Disclosure form?

The Closing Disclosure form is a detailed document that outlines the final terms of your loan and the closing costs associated with it. It serves as a comparison tool against your initial Loan Estimate, helping you understand what you will pay at closing. The form includes essential information such as the loan amount, interest rate, monthly payments, and any applicable fees. It is important to review this document carefully to ensure all terms are accurate before finalizing your mortgage agreement.

When should I receive the Closing Disclosure?

You should receive the Closing Disclosure at least three business days before your closing date. This timeline allows you to review the document thoroughly and ask any questions or raise concerns with your lender. If you notice any discrepancies or have questions about specific charges, it is advisable to address them as soon as possible to avoid any surprises on closing day.

What should I look for when reviewing my Closing Disclosure?

When reviewing your Closing Disclosure, pay close attention to several key areas. First, check the loan terms, including the loan amount, interest rate, and monthly payments. Next, examine the closing costs section to understand what you will be responsible for paying. Look for any fees that seem higher than expected or were not disclosed previously. Additionally, review the projected payments, which provide insight into how your monthly expenses may change over time. If anything seems unclear or incorrect, don’t hesitate to reach out to your lender for clarification.

Can the terms in the Closing Disclosure change before closing?

While the Closing Disclosure provides the final terms of your loan, some elements may change before closing. However, any changes must be communicated to you, and you should receive a revised Closing Disclosure if significant adjustments occur. For instance, if your loan amount or interest rate changes, you will be notified. It's crucial to stay in contact with your lender and ask for updates to ensure that you are fully informed about any changes that could affect your closing experience.

Ignoring the Comparison with the Loan Estimate: One of the most common mistakes is failing to compare the Closing Disclosure with the Loan Estimate. This document outlines the final loan terms and closing costs, and discrepancies can indicate potential issues or misunderstandings.

Overlooking Closing Costs: Many people focus solely on the loan amount and interest rate, neglecting to scrutinize the closing costs. These costs can significantly impact the total amount due at closing, so it’s crucial to review them carefully.

Misunderstanding the Escrow Account: Some borrowers may not fully grasp the implications of having an escrow account. This account is used to pay property taxes and insurance, and failing to understand its purpose can lead to unexpected financial burdens later.

Not Asking Questions: Lastly, many individuals hesitate to ask questions about the form. Whether it's about specific fees or terms, seeking clarification is essential. Ignoring this step can lead to confusion and financial missteps down the line.

The Closing Disclosure form is a critical document in the home buying process, detailing the final terms of a loan and the associated closing costs. However, several other forms and documents are often used in conjunction with it to ensure a smooth transaction. Here’s a brief overview of these essential documents.

Each of these documents plays a vital role in the home buying process, ensuring that all parties are protected and informed. Understanding them can help buyers navigate the complexities of closing with confidence.

The Loan Estimate is a key document that provides borrowers with an overview of the estimated costs associated with a mortgage. This document is issued early in the mortgage process and includes details such as loan terms, projected monthly payments, and estimated closing costs. Similar to the Closing Disclosure, the Loan Estimate helps borrowers compare different loan offers and understand their financial obligations. Both documents serve to ensure transparency, but while the Loan Estimate outlines expected costs, the Closing Disclosure presents the final terms and costs right before closing.

The HUD-1 Settlement Statement is another important document that resembles the Closing Disclosure. Historically used in real estate transactions, the HUD-1 provided a detailed breakdown of all costs associated with closing a mortgage. Like the Closing Disclosure, it itemized fees and charges, allowing buyers and sellers to see where their money was going. However, the HUD-1 has largely been replaced by the Closing Disclosure for most residential transactions, as the latter is designed to be more user-friendly and easier to understand for borrowers.

The Good Faith Estimate (GFE) was previously used to inform borrowers about the costs associated with obtaining a mortgage. Similar to the Loan Estimate, the GFE provided an estimate of closing costs and loan terms. However, the GFE has been phased out in favor of the Loan Estimate and Closing Disclosure, which are more standardized and easier to compare. Both the GFE and the Loan Estimate aim to give borrowers a clearer picture of their financial commitments, but the newer documents are intended to be more precise and informative.

The Truth in Lending Disclosure (TIL) is a document that details the costs of borrowing money, including the annual percentage rate (APR) and total finance charges. While the TIL focuses more on the cost of credit rather than specific closing costs, it shares a common goal with the Closing Disclosure: to inform borrowers about their financial obligations. Both documents are essential in helping consumers understand what they are agreeing to when they take out a loan, ensuring they are well-informed before making a commitment.

The Promissory Note is a legal document that outlines the borrower's promise to repay the loan under specified terms. While it differs from the Closing Disclosure in that it is not a cost breakdown, it is similar in that it serves as a crucial component of the mortgage process. The Promissory Note details the loan amount, interest rate, and repayment schedule, providing clarity on the borrower's obligations. Both documents are integral to the mortgage transaction, establishing the framework for repayment and the costs associated with the loan.

The Mortgage or Deed of Trust is another document that is closely related to the Closing Disclosure. This legal instrument secures the loan by giving the lender a claim to the property should the borrower default. While the Closing Disclosure focuses on the financial aspects of the transaction, the Mortgage or Deed of Trust outlines the rights and responsibilities of both parties. Both documents are essential for a complete understanding of the mortgage process, as they work together to define the terms of the loan and the security for the lender.

When filling out the Closing Disclosure form, it is essential to approach the process with care. Here are four important do's and don'ts to consider:

This is not accurate. The Closing Disclosure outlines the final terms and costs of your loan, while the Loan Estimate provides an initial overview of the estimated costs. The two documents serve different purposes and should be compared carefully.

In reality, the Closing Disclosure is important for both buyers and sellers. It details all the financial aspects of the transaction, including costs associated with the sale, which affect both parties.

This is misleading. While some fees are set and non-negotiable, others can be discussed. Buyers and sellers should feel empowered to ask questions and negotiate where possible.

This is incorrect. The Closing Disclosure is a legally binding document that outlines the terms of the loan and the closing costs. Signing it indicates your agreement to these terms.

While it is true that signing the document indicates acceptance, there are circumstances under which you can still withdraw or renegotiate your loan. It is advisable to communicate with your lender if you have concerns.

The Closing Disclosure form is an essential document in the home buying process. Here are some key takeaways to help you understand its significance and how to use it effectively:

By keeping these points in mind, you can navigate the closing process with greater confidence and ensure that you are fully informed about your loan and its terms.