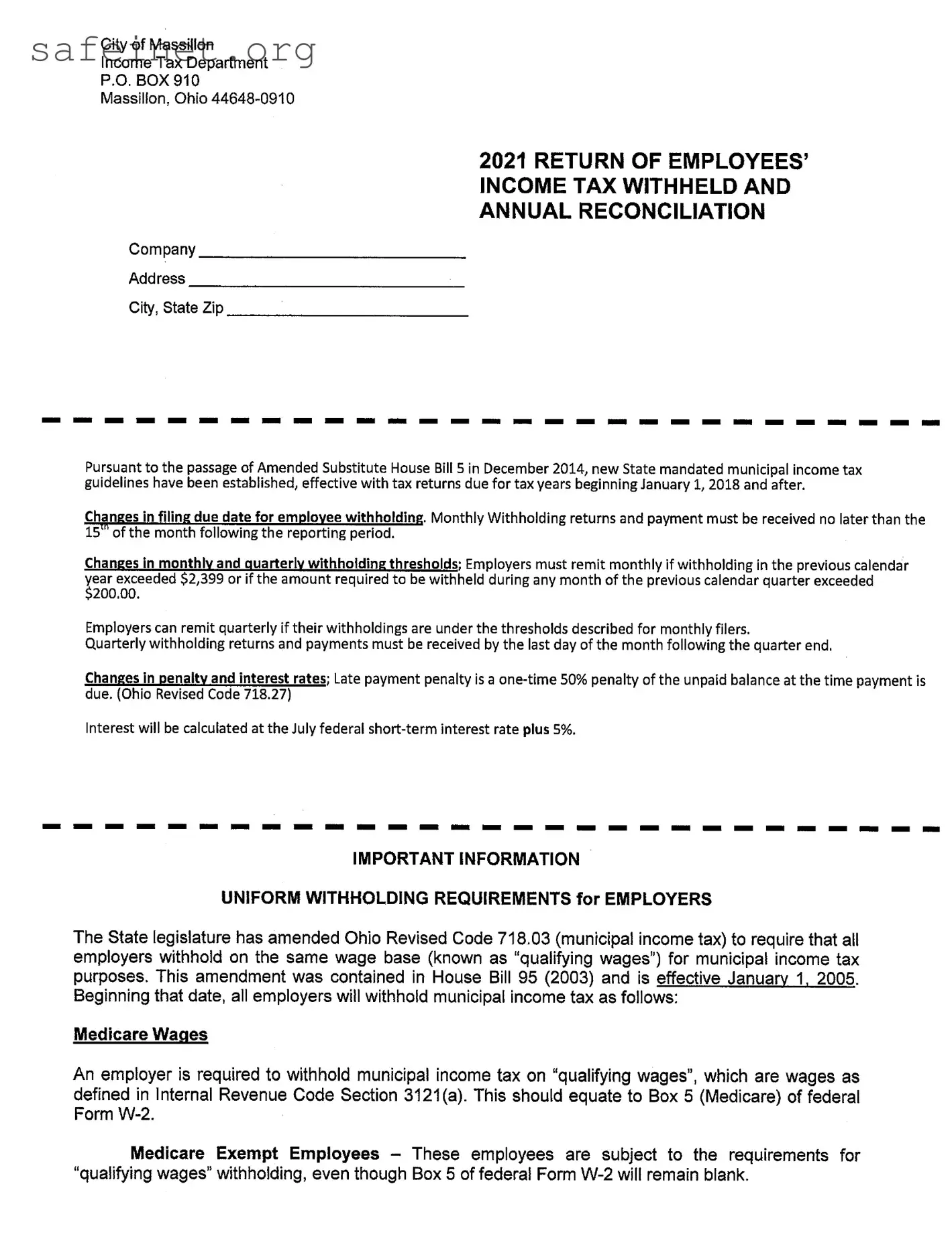

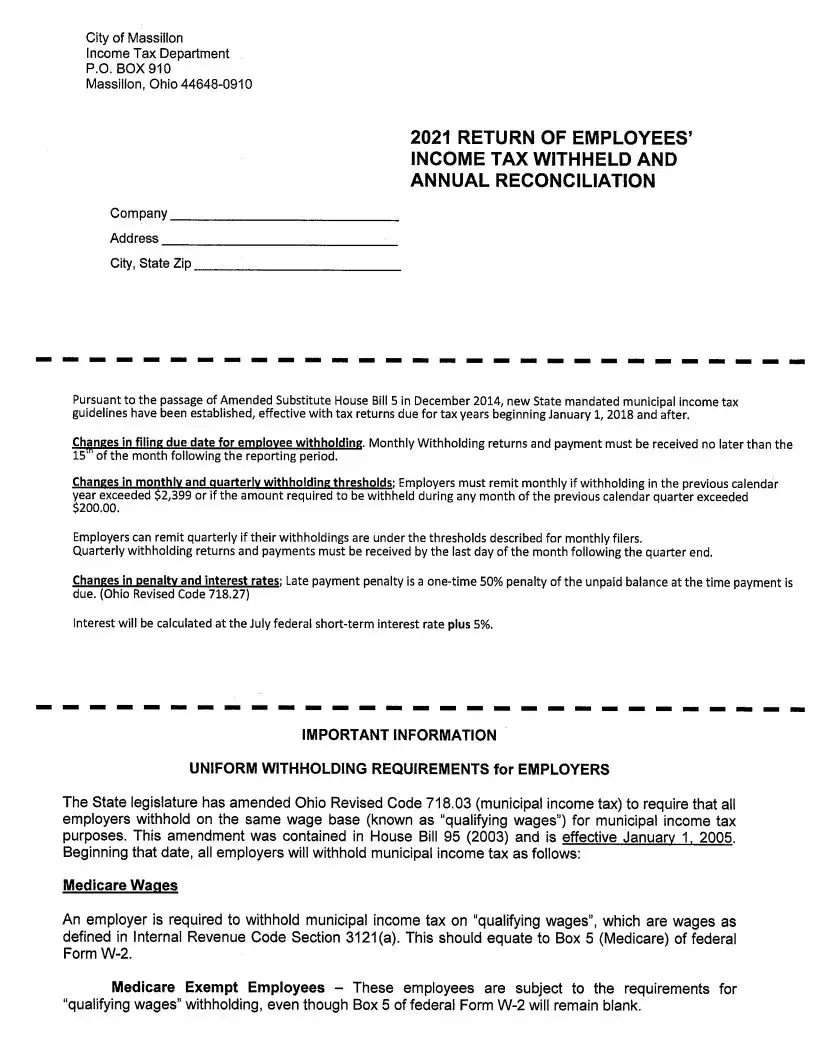

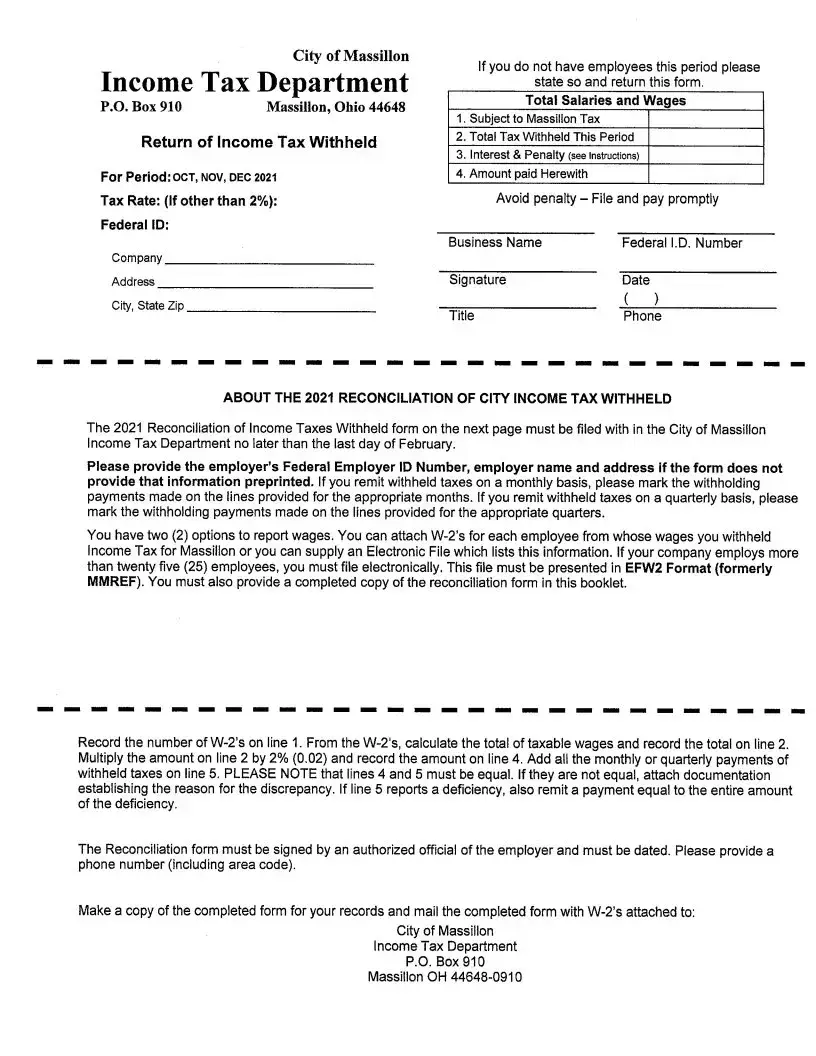

For employers in Massillon, Ohio, timely compliance with the City of Massillon Income Tax form is crucial. This form serves as both the Return of Employees’ Income Tax Withheld and the Annual Reconciliation document. Since changes implemented in 2014 have significantly altered the landscape of municipal income tax guidelines, understanding the responsibilities tied to this form is essential. Employers must navigate new filing deadlines, ensuring monthly withholding returns are submitted by the 15th of the following month when applicable. Certain thresholds dictate if taxes can be remitted quarterly, with specific requirements based on previous withholding amounts. This form also outlines the need to withhold municipal income tax on qualifying wages, which encompasses various forms of employee compensation. Importantly, a tax rate of 2% applies, with penalties for late payments clearly defined. Each aspect of the form—from the required information to submission instructions—plays a vital role in maintaining compliance and supporting local city services. Furthermore, employers must ensure they keep their records updated and follow up on any discrepancies to prevent unnecessary penalties. This article serves as a comprehensive guide to navigating the intricacies of the City of Massillon Income Tax form, emphasizing the urgency of adherence to deadlines and accuracy in reporting.

| Fact Name | Description |

|---|---|

| Tax Rate | The City of Massillon has a municipal income tax rate of 2% applied to qualifying wages. |

| Filing Frequency | Employers must file monthly or quarterly based on the amount of income tax withheld in the previous calendar year. |

| Due Dates | Monthly returns are due by the 15th of the following month; quarterly returns are due by the last day of the month after the quarter ends. |

| Penalty for Late Payment | A late payment incurs a one-time penalty of 50% of the unpaid balance, as per Ohio Revised Code 718.27. |

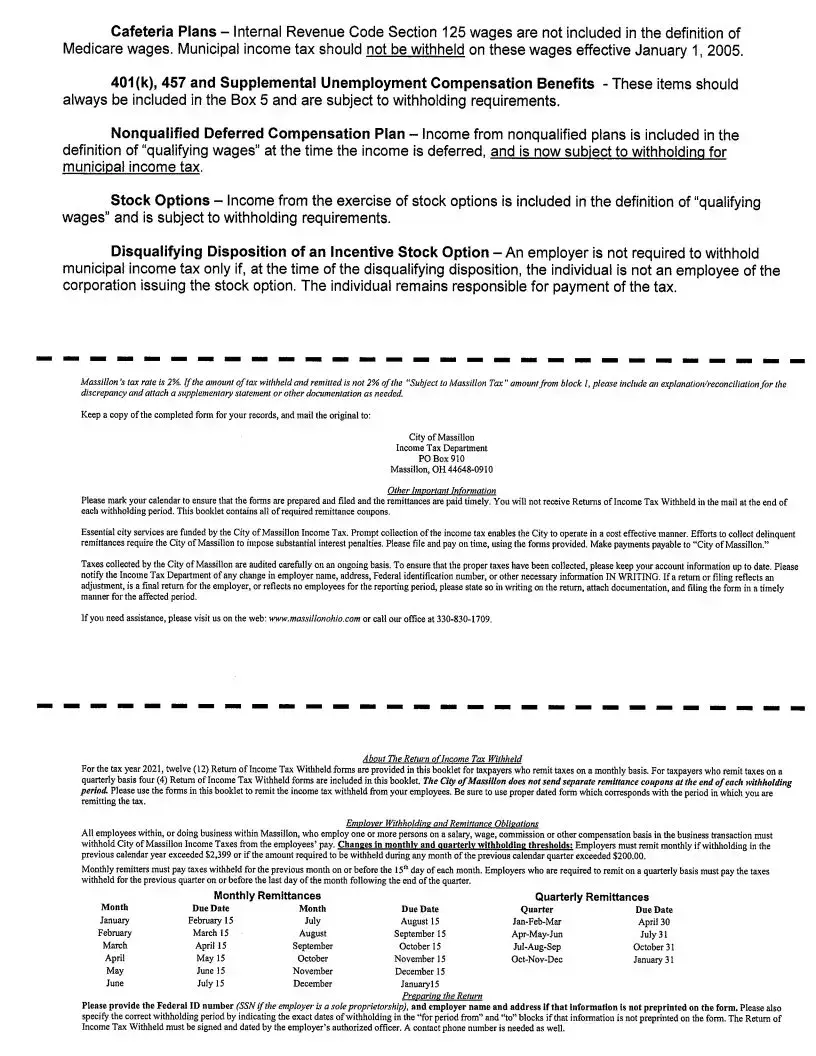

| Qualifying Wages | Employers are required to withhold tax on “qualifying wages,” which are defined under Internal Revenue Code Section 3121(a). |

| Remittance Guidelines | Employers must remit income tax withheld using the forms provided, ensuring they correspond to the correct reporting period. |

| Documentation Requirements | Employers must maintain accurate records and notify the Income Tax Department of any changes in employer information in writing. |

Once you have gathered all necessary information, filling out the City of Massillon Income Tax form is a straightforward process. Ensure that you have all relevant details at hand, such as your Federal ID number, company address, employee wages, and the total tax withheld. Follow these steps to complete the form accurately.

By completing these steps carefully, you can ensure that your submission is timely and accurate, helping to support essential city services. Staying organized and following through with deadlines is key to a smooth process.

What is the City of Massillon Income Tax rate?

The tax rate for the City of Massillon is currently set at 2%. Employers are required to withhold this rate from the wages of employees who are subject to Massillon’s income tax. It is important for employers to ensure that the correct amount is withheld and reported to avoid discrepancies.

When are the due dates for withholding tax remittances?

Employers must remit withholding taxes on a monthly or quarterly basis, depending on their annual withholding amounts. Monthly filers must submit payments by the 15th of the month following the reporting period. For quarterly filers, payments are due by the last day of the month following the end of the quarter. Adhering to these deadlines is crucial for avoiding penalties.

What happens if an employer does not pay on time?

Late payments incur a one-time penalty of 50% of the unpaid balance at the time the payment is due. Additionally, interest accrues at a rate determined by the July federal short-term interest rate plus 5%. Timely filing and payments help avoid such penalties and ensure compliance with tax obligations.

How should employers prepare the Return of Income Tax Withheld?

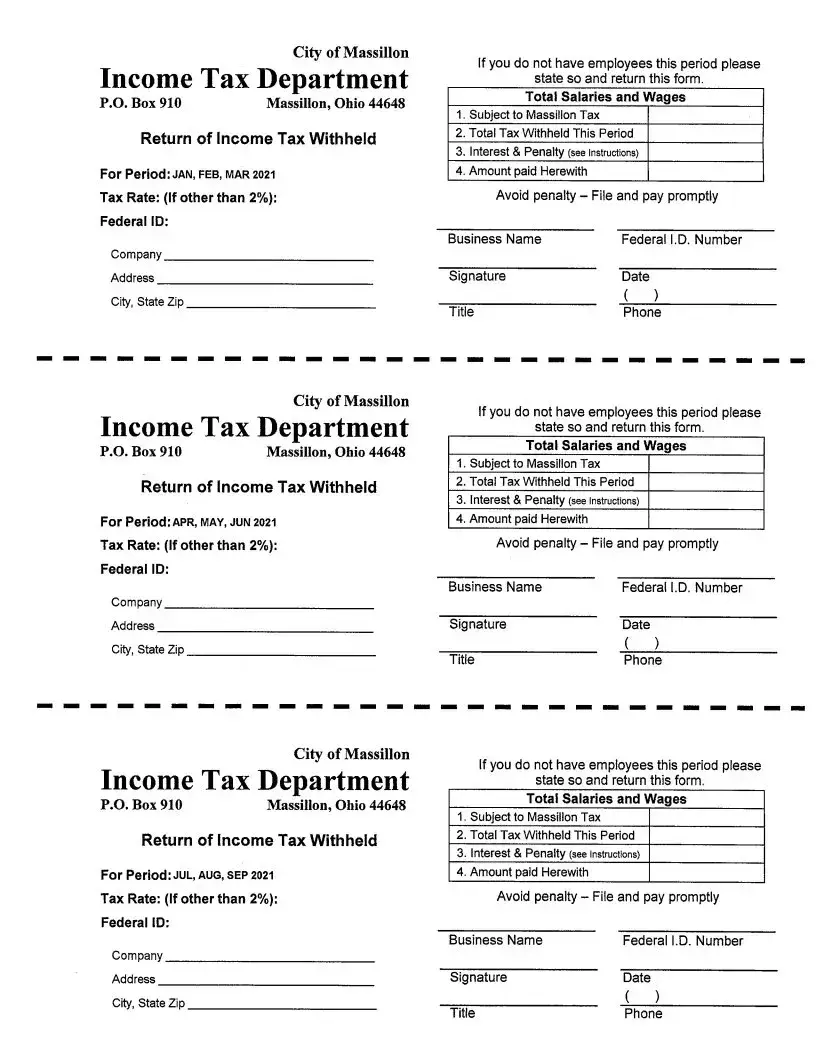

Employers should provide their Federal ID number, or Social Security Number if a sole proprietorship, along with the name and address of the business. The return must be signed and dated by an authorized officer. In cases where there are no employees during a specific period, it is necessary to indicate this on the form and submit it accordingly.

Are there different forms for monthly and quarterly filings?

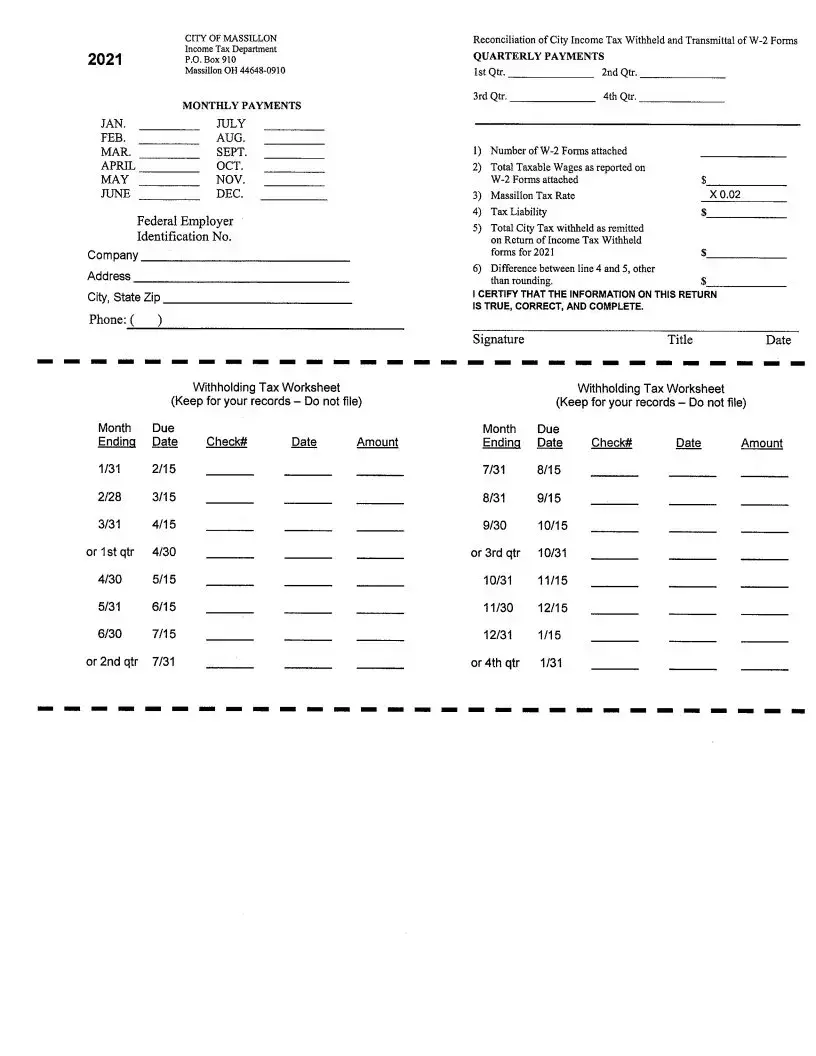

Yes, the City of Massillon provides twelve Return of Income Tax Withheld forms for monthly filers and four forms for quarterly filers in the tax booklet. Employers must ensure they are using the correct forms that correspond to the filing frequency required for their business.

What should an employer do if their employer information changes?

Employers need to notify the City of Massillon Income Tax Department in writing about any changes to their name, address, Federal identification number, or any other relevant information. Keeping the account information current is essential for accurate tax reporting and compliance.

Failing to use the correct tax rate. The City of Massillon tax rate is 2%. Using a different rate may result in underpayment.

Not providing the appropriate Federal ID number. This number is essential for processing the return. If the employer is a sole proprietor, a Social Security Number (SSN) should be used if no Federal ID is available.

Omitting the employer's name and address. The form requires complete information for proper identification and record-keeping.

Neglecting to indicate the correct withholding period. Employers must state the specific dates for which taxes are being remitted, particularly if this information is not preprinted on the form.

Forgetting to sign and date the return. An authorized officer of the employer must sign the document for it to be valid.

Not including a contact phone number. This information is crucial for any follow-up questions or clarifications that may arise regarding the return.

Not marking the form if there are no employees during the reporting period. If there are no employees, stating this explicitly on the form is necessary to avoid confusion.

Missing the remittance deadlines. Monthly remitters must submit taxes by the 15th of the following month, while quarterly remitters must adhere to specific deadlines to avoid late payment penalties.

When filing the City of Massillon Income Tax form, employers often need to submit additional documents to ensure compliance with local tax regulations. Below is a brief overview of relevant forms and documents commonly used alongside the income tax form.

By preparing and submitting these forms, employers can facilitate smoother interactions with the City of Massillon Income Tax Department, ensuring timely and accurate tax filings. Compliance not only avoids penalties but also upholds the integrity of local tax revenues.

The W-2 form, officially known as the Wage and Tax Statement, bears striking similarities to the City of Massillon Income Tax form. Both documents report earnings and taxes withheld from employees' pay. The W-2 is provided by employers to employees at the end of each tax year, summarizing their earnings and tax deductions. Similarly, the Massillon Income Tax form requires employers to report amounts withheld for municipal tax, creating a direct correlation between the two as they both are essential for accurate tax reporting and compliance with local and federal laws.

The 1099-MISC form also shares common ground with the Massillon Income Tax form. While the W-2 is designated for salaried employees, the 1099-MISC is utilized for reporting income earned by independent contractors and freelancers. Just like the Massillon form, the 1099-MISC must detail the amounts paid to individuals and any taxes withheld. This document is crucial for ensuring that all types of income are accurately reported to the IRS, reinforcing the concept that thorough reporting is vital for tax obligations.

Employers face similar requirements when dealing with the IRS Form 941, the Employer’s QUARTERLY Federal Tax Return. This form, like the Massillon Income Tax form, requires detailed reporting of wages paid and taxes withheld. While Form 941 covers federal payroll taxes, it aligns with local income tax requirements by providing a snapshot of an employer's tax liabilities over a specified period. The deadlines for filing are structured consistently across both forms, reflecting a common commitment to rigorous tax compliance.

The Ohio Department of Taxation’s Annual Tax Reconciliation form also presents similarities to the Massillon Income Tax document. This form aggregates various tax figures throughout the year and provides a summary for state tax officials. Akin to the Massillon form's reconciliatory nature, the annual reconciliation outlines withheld amounts that may need correction or adjustment, ensuring that employers meet state tax obligations accurately and comprehensively.

The Employer Registration form serves as another related document, which establishes an employer’s obligation to withhold taxes from employee wages. While the City of Massillon Income Tax form reports amounts withheld, the Employer Registration form lays the framework for these withholdings by outlining the employer's role in the tax process. In both cases, proper registration and adherence to local tax laws are crucial for businesses operating within the city.

Lastly, the local business tax registration forms resonate closely with the Massillon Income Tax form. These forms facilitate the establishment of the business within a municipality and mandate compliance with local tax regulations. Just as the Massillon form enforces monthly or quarterly remittance of taxes withheld from employees, local business tax registration is essential for maintaining a clear record of a business’s earnings and corresponding obligations to the city.

When filling out the City of Massillon Income Tax form, it is crucial to adhere to the following guidelines:

Conversely, avoid these common pitfalls:

Many people have misunderstandings about the City of Massillon Income Tax form. Below are some common misconceptions, along with clarifications to help ensure proper compliance and understanding.

This is false. Any employer must file this form if they employ even one person within the city and have any compensation that falls under the municipal tax regulations.

This is incorrect. Employers must proactively prepare and file the form themselves. The City does not send individual returns automatically.

This is not true. The City of Massillon has set a fixed tax rate of 2% for all employers, regardless of their size or the nature of their business.

No, these deadlines are strict. Monthly filings are due by the 15th of the following month, while quarterly submissions are due by the last day of the following month after the quarter ends.

This is a misconception. Local municipal income taxes are separate obligations. Employers must comply with both state and local tax regulations.

That is incorrect. The amount withheld must reflect the established tax rate of 2%. If there is any discrepancy, an explanation must accompany the form when submitted.

This is misleading. In addition to a one-time penalty of up to 50% of the unpaid balance, interest accrues based on the federal short-term rate plus an additional 5%, which can significantly increase the amount owed.

Understanding the City of Massillon Income Tax form can streamline your filing process and help ensure compliance with local tax regulations. Here are some key takeaways to keep in mind:

Paying attention to these aspects helps ensure your business remains compliant while supporting essential city services.