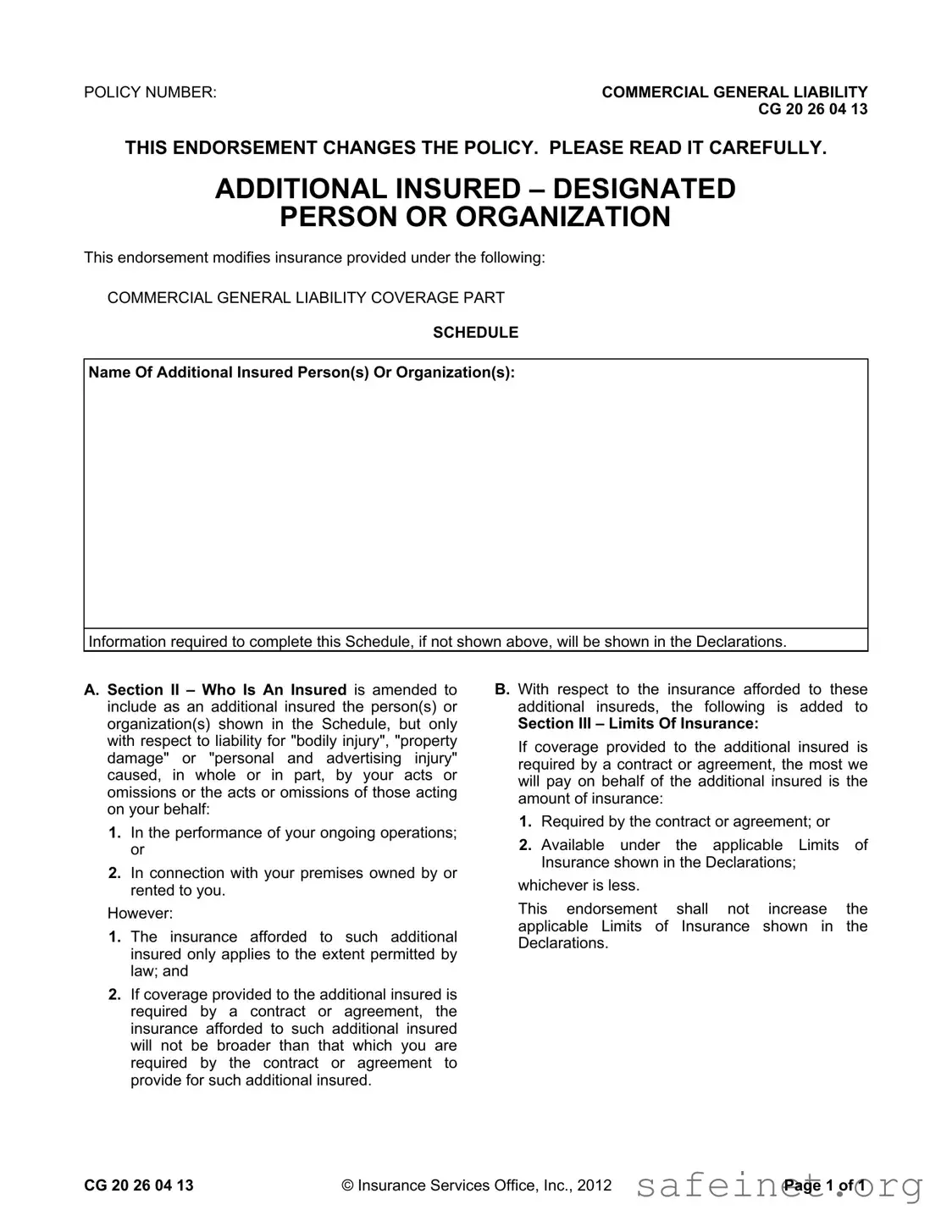

The CG 20 26 04 13 form is an important endorsement that modifies a Commercial General Liability (CGL) policy, specifically addressing the inclusion of additional insured parties. This endorsement allows for certain individuals or organizations to be recognized as additional insureds under the policy, which can be crucial for businesses that often engage in contracts requiring such coverage. By listing these additional insured parties, the form outlines the specific liabilities for which they are covered, including bodily injury, property damage, and personal and advertising injury. The coverage applies only to incidents arising from the named insured's operations or the premises they own or rent. Importantly, the form stipulates that the extent of coverage for these additional insureds is limited to what is legally permissible and may not exceed the obligations outlined in any existing contracts. Furthermore, it clarifies the limits of insurance, ensuring that the payout for additional insureds is capped at either the amount required by the contract or the limits specified in the policy declarations, whichever is lower. This structure not only protects the interests of the additional insureds but also maintains the integrity of the original policy limits, making it a vital component of risk management for businesses.

| Fact Name | Description |

|---|---|

| Policy Number | The form is identified by the policy number CG 20 26 04 13. |

| Purpose | This endorsement adds designated persons or organizations as additional insureds under a Commercial General Liability policy. |

| Coverage Scope | It covers liability for bodily injury, property damage, or personal and advertising injury related to ongoing operations or premises owned or rented by the insured. |

| Contractual Limitations | The insurance for additional insureds will not exceed the coverage required by a contract or the limits specified in the policy declarations, whichever is less. |

| Governing Law | The form is governed by state-specific laws, which may vary. It is essential to refer to the applicable state regulations for precise requirements. |

To complete the CG 20 26 04 13 form, you will need to provide specific details regarding the additional insured person or organization. Ensure that all information is accurate and complete, as this will affect the coverage provided under your policy.

What is the purpose of the CG 20 26 04 13 form?

The CG 20 26 04 13 form serves as an endorsement to a Commercial General Liability (CGL) policy. Its primary function is to add specific individuals or organizations as additional insured parties. This means that these additional insureds are protected under the policy for certain liabilities arising from your operations or premises. It’s important to read this form carefully to understand the extent of coverage provided.

Who can be listed as an additional insured on this form?

You can list any person or organization that you have a contractual obligation to include as an additional insured. This could include clients, landlords, or partners. The specific names of these individuals or organizations should be included in the Schedule section of the form. If they are not listed, you must refer to the Declarations for more information.

What types of liabilities are covered for additional insureds?

The coverage for additional insureds includes liabilities for bodily injury, property damage, or personal and advertising injury. However, this coverage only applies if the injury or damage is caused, in whole or in part, by your actions or the actions of those working on your behalf. This makes it essential to ensure that the additional insureds are aware of their coverage limitations.

Are there any limitations to the coverage provided to additional insureds?

Yes, there are limitations. The coverage for additional insureds is only as broad as required by the contract or agreement. Additionally, the insurance will not exceed the limits specified in your policy’s Declarations. If the contract stipulates a lower limit, that will apply. This ensures that you are not held liable for coverage beyond what is contractually obligated.

Does the CG 20 26 04 13 form increase the limits of insurance?

No, this endorsement does not increase the applicable limits of insurance shown in the Declarations. The coverage provided to additional insureds will fall within the existing limits of your policy. It’s crucial to understand that while additional insureds gain coverage, it does not expand the overall limits of your insurance policy.

How does this form affect ongoing operations and premises?

The endorsement specifically covers liabilities that arise from your ongoing operations or the premises you own or rent. This means that if an incident occurs related to these areas, the additional insureds may be protected under your policy, provided that the liability is connected to your actions or omissions.

What should I do if I have more questions about this form?

If you have further questions or need clarification regarding the CG 20 26 04 13 form, it is advisable to consult with your insurance agent or a legal professional who specializes in insurance matters. They can provide tailored advice and help ensure that you understand your coverage and obligations fully.

Incomplete Information: Failing to provide all necessary details, such as the name of the additional insured, can lead to delays or denial of coverage.

Incorrect Policy Number: Entering an incorrect policy number can result in the form being invalidated. Always double-check this information.

Misunderstanding Coverage Limits: Not understanding the limits of insurance can lead to expectations that exceed what is actually provided under the policy.

Omitting Required Declarations: If the required declarations are not included, the form may not be processed correctly. Ensure all relevant documents are attached.

Ignoring Legal Requirements: Each state may have specific legal requirements regarding additional insured endorsements. Ignoring these can result in non-compliance.

Assuming Automatic Coverage: Believing that all additional insureds automatically receive coverage without proper documentation can lead to misunderstandings.

Failing to Review Contracts: Not reviewing contracts or agreements that require additional insured status can result in providing less coverage than needed.

The CG 20 26 04 13 form is an important document in the realm of commercial general liability insurance. It specifically addresses the inclusion of additional insured parties, which can be crucial for businesses and organizations engaged in various operations. Alongside this form, there are several other documents and forms that are often utilized to complement its provisions. Below is a list of these related documents, each serving a unique purpose in the insurance process.

Understanding these documents can enhance one’s grasp of the insurance landscape and its implications for liability coverage. Each document plays a significant role in ensuring that businesses are adequately protected and compliant with contractual obligations.

The CG 20 26 04 13 form serves a specific purpose in the realm of commercial general liability insurance by adding additional insureds to a policy. A similar document is the CG 20 10 form, which also functions as an endorsement to the commercial general liability policy. This form extends coverage to additional insured parties but does so in a more general manner. It typically includes coverage for liability arising from ongoing operations, but it does not specify the conditions under which the additional insured must be protected. This can lead to broader coverage compared to the CG 20 26 04 13, which is more tailored to specific contractual obligations.

Another comparable document is the CG 20 37 form, which is known as the Additional Insured – Owners, Lessees, or Contractors – Scheduled Person or Organization endorsement. This form is particularly useful for construction projects, as it allows contractors or owners to be added as additional insureds. Like the CG 20 26 04 13, it provides coverage for bodily injury and property damage, but it is more focused on the relationships between contractors and property owners. The CG 20 37 form emphasizes the contractual obligations that may arise during construction activities, ensuring that all parties are adequately protected.

The CG 20 33 form is another relevant endorsement that adds additional insured status but is specifically tailored for completed operations. This form provides coverage to additional insureds for liability that arises after the work has been completed. Unlike the CG 20 26 04 13, which covers ongoing operations, the CG 20 33 form addresses potential claims that may arise once a project has concluded. This distinction is crucial for businesses that want to protect themselves from future liabilities that could arise after the completion of their work.

The CG 20 11 form, known as the Additional Insured – Managers or Lessors of Premises endorsement, is similar in that it adds coverage for specific parties, such as property managers or lessors. This form extends liability protection to those who manage or lease the premises where the insured operates. It is particularly relevant for businesses that rent or lease space, as it ensures that the property owner is protected from claims related to the insured's operations. While the CG 20 26 04 13 focuses on the insured's actions, the CG 20 11 emphasizes the relationship between the insured and the property owner.

Lastly, the CG 20 31 form, which is the Additional Insured – State or Governmental Agency endorsement, provides coverage to state or governmental entities. This form is essential for contractors working on public projects, as it ensures that government agencies are protected from liabilities arising from the contractor’s operations. The CG 20 31 form is similar to the CG 20 26 04 13 in that it adds additional insureds, but it specifically addresses the unique needs and requirements of public entities. This endorsement is crucial for compliance with contractual obligations when working with government contracts.

When filling out the CG 20 26 04 13 form, attention to detail is crucial. Here are some important dos and don’ts to keep in mind:

By following these guidelines, you can help ensure that the form is completed correctly and efficiently, minimizing the risk of complications down the line.

Understanding the CG 20 26 04 13 form can be a bit confusing, especially with the various myths surrounding it. Here are seven common misconceptions to help clarify what this form really entails:

By debunking these misconceptions, you can better navigate the complexities of the CG 20 26 04 13 form and ensure that you have the appropriate coverage in place.

Here are some key takeaways regarding the CG 20 26 04 13 form, which pertains to additional insured coverage under a Commercial General Liability policy: