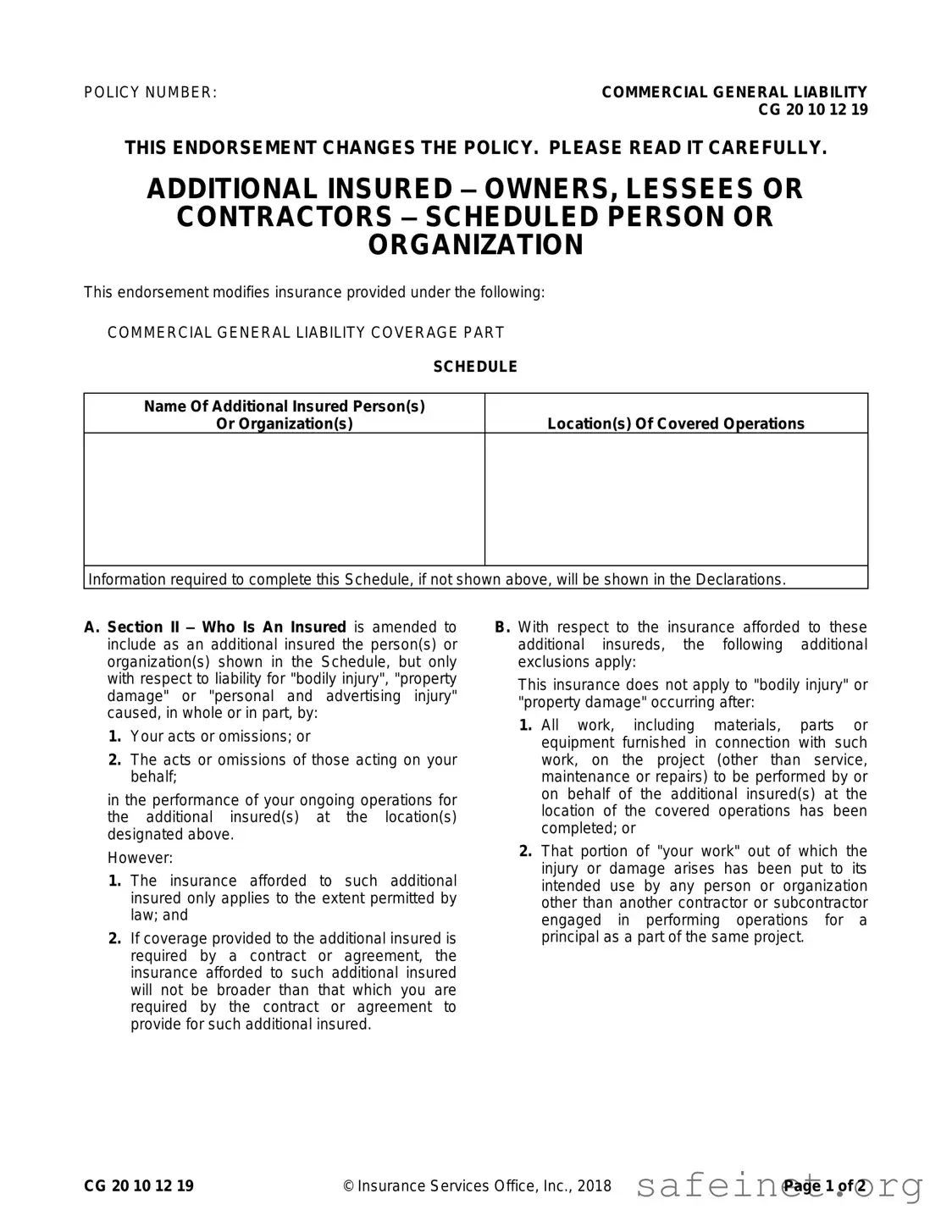

The CG 20 10 07 04 Liability Endorsement form plays a crucial role in commercial general liability insurance policies. This endorsement specifically addresses the inclusion of additional insured parties, such as owners, lessees, or contractors, as detailed in the scheduled section of the form. It modifies the insurance coverage to provide protection for these additional insureds against claims of bodily injury, property damage, or personal and advertising injury. Such coverage is applicable only when the liability arises from the acts or omissions of the named insured or their representatives while performing operations for the additional insured at specified locations. However, the endorsement includes important limitations. For instance, coverage does not extend to injuries or damages occurring after the completion of the work, nor does it increase the overall limits of the policy. The amount payable on behalf of the additional insured is capped at the lesser of the contractual requirement or the policy limits. Understanding these aspects is essential for both policyholders and additional insureds to navigate their insurance responsibilities effectively.

| Fact Name | Details |

|---|---|

| Policy Number | CG 20 10 12 19 |

| Type of Coverage | This endorsement modifies insurance provided under the Commercial General Liability Coverage Part. |

| Purpose | It adds additional insured status for owners, lessees, or contractors as specified in the schedule. |

| Liability Coverage | Covers bodily injury, property damage, or personal and advertising injury caused by the insured's acts or omissions. |

| Exclusions | Does not apply to bodily injury or property damage occurring after all work has been completed or the work has been put to intended use. |

| Limits of Insurance | The coverage limit for additional insureds is the lesser of the amount required by contract or the available policy limits. |

| Governing Law | Specific governing laws may vary by state; consult local regulations for applicability. |

Filling out the CG 20 10 07 04 Liability Endorsement form is an important task that requires careful attention to detail. This endorsement modifies your existing insurance policy to add additional insured parties. Completing the form accurately ensures that the necessary parties are covered under your commercial general liability insurance. Follow these steps to fill out the form correctly.

After completing the form, keep a copy for your records. Submit the original form to your insurance provider as directed. This will ensure that the additional insured parties are properly covered under your policy.

What is the purpose of the CG 20 10 07 04 Liability Endorsement form?

This form serves to add specific individuals or organizations as additional insured parties under a Commercial General Liability policy. It provides coverage for liabilities related to bodily injury, property damage, or personal and advertising injury that may arise from the actions of the insured or those acting on their behalf. This endorsement is particularly useful in situations where contractors or service providers are working on behalf of another entity, ensuring that both parties are protected under the policy.

Who qualifies as an additional insured under this endorsement?

The additional insureds are specified in a schedule included with the endorsement. This can include owners, lessees, or contractors who are involved in the operations at designated locations. However, the coverage applies only to liabilities that arise from the ongoing operations of the insured for the additional insureds at those specific locations. It's important to note that the coverage is limited to the extent permitted by law and does not exceed what is required by any contracts or agreements.

What limitations are included in the coverage for additional insureds?

There are several important limitations to be aware of. First, the endorsement does not cover bodily injury or property damage that occurs after all work on the project has been completed. This includes any materials, parts, or equipment used in connection with the work. Additionally, if the portion of work that caused the injury or damage has been put to its intended use by someone other than another contractor or subcontractor, coverage will not apply. These limitations help define the scope of the insurance protection provided.

How does this endorsement affect the limits of insurance?

The endorsement specifies that the coverage for additional insureds does not increase the overall limits of the insurance policy. If coverage is required by a contract, the maximum amount payable on behalf of the additional insured will be the lesser of the amount specified in that contract or the applicable limits of the insurance policy. This ensures that the coverage remains within the bounds of what was originally agreed upon in the policy.

Is there any additional information required to complete the endorsement?

Yes, the endorsement includes a schedule that must specify the names of the additional insured persons or organizations and the locations of the covered operations. If this information is not included in the endorsement itself, it will be provided in the Declarations section of the policy. Ensuring that this information is accurate and complete is crucial for the endorsement to be effective.

Failing to include the policy number at the top of the form can lead to confusion and delays in processing.

Not specifying the name of the additional insured accurately may result in coverage issues.

Leaving out the location(s) of covered operations can create ambiguity about where the coverage applies.

Neglecting to check if all required information is included in the Declarations can lead to incomplete submissions.

Misunderstanding the scope of liability for the additional insured can result in insufficient coverage.

Not reviewing the exclusions listed in the endorsement may lead to unexpected denials of claims.

Forgetting to confirm that the coverage aligns with the contractual obligations can cause legal complications.

Overlooking the limits of insurance stated in the endorsement can lead to underinsurance.

Failing to sign and date the form can delay the endorsement's effectiveness.

The CG 20 10 07 04 Liability Endorsement form is a crucial document in the realm of commercial general liability insurance. It serves to add additional insured parties to a policy, ensuring that they are covered for specific liabilities. Along with this endorsement, several other forms and documents are often utilized to provide comprehensive coverage and clarify obligations. Here’s a list of some commonly associated documents:

Understanding these documents and how they interrelate with the CG 20 10 07 04 Liability Endorsement form is essential for ensuring that all parties are adequately protected and that contractual obligations are met. Each document plays a role in clarifying responsibilities and coverage, contributing to a smoother operational process.

The CG 20 10 07 04 Liability Endorsement form shares similarities with the Additional Insured Endorsement (CG 20 10). This form extends coverage to additional parties, such as contractors or owners, for liabilities arising from the named insured's operations. Both documents aim to protect additional insureds against claims of bodily injury or property damage, ensuring they are covered as long as the claims relate to the named insured's work. The primary difference lies in the specific language and conditions under which coverage is granted, but the overall intent remains the same: to broaden the scope of protection in commercial liability situations.

Another similar document is the Additional Insured – Completed Operations Endorsement (CG 20 37). This endorsement specifically covers claims that arise after the insured's work has been completed. Like the CG 20 10 07 04, it protects additional insured parties from liabilities related to the insured's operations. The key distinction is that the CG 20 37 focuses on completed work rather than ongoing operations, making it essential for projects where the risk of claims may arise after the work is finished.

The Primary and Non-Contributory Endorsement (CG 20 01) is also comparable. This endorsement ensures that the insurance coverage for additional insureds is primary, meaning it will respond first in the event of a claim, before any other insurance. This is similar to the CG 20 10 07 04, which also provides coverage for additional insureds but does not specifically address the order of coverage. The primary and non-contributory aspect is crucial for parties wanting to avoid disputes over which insurance should cover a claim.

The Waiver of Subrogation Endorsement (CG 24 04) is another document that bears resemblance to the CG 20 10 07 04. This endorsement prevents the insurance company from seeking reimbursement from the additional insured after paying a claim. While the CG 20 10 07 04 focuses on extending coverage, the Waiver of Subrogation emphasizes protecting the additional insured from future claims by the insurer. Both documents work together to provide a comprehensive safety net for additional insured parties.

The Additional Insured – Owners, Lessees, or Contractors Endorsement (CG 20 10 11 85) is similar in that it also provides coverage to additional insureds for liability arising out of the named insured’s operations. However, this version specifically addresses owners, lessees, or contractors. The CG 20 10 07 04 focuses on any person or organization, making it slightly broader in its application while still maintaining the core purpose of protecting additional parties from liability claims.

The Contractual Liability Endorsement (CG 21 39) is another relevant document. It allows the insured to cover liabilities assumed in a contract, which may include indemnification agreements. While the CG 20 10 07 04 focuses on extending coverage to additional insureds, the Contractual Liability Endorsement specifically deals with liabilities that arise from contractual obligations. Both forms are essential for ensuring comprehensive coverage in various business arrangements.

The Excess Liability Policy is also similar in that it provides additional coverage above the limits of the primary policy, including the CG 20 10 07 04. While the endorsement offers specific protections for additional insureds under the primary policy, an Excess Liability Policy kicks in when those limits are exhausted. This layered approach to coverage ensures that additional insureds are protected even in high-stakes situations.

The Umbrella Liability Policy is another document that complements the CG 20 10 07 04. An Umbrella Policy provides broader coverage and higher limits, often including additional insureds. While the CG 20 10 07 04 specifically addresses the coverage for additional parties under a general liability policy, the Umbrella Policy extends that protection further, allowing for more comprehensive coverage in case of severe claims.

Finally, the Professional Liability Endorsement (CG 21 46) is similar in that it provides coverage for claims related to professional services. While the CG 20 10 07 04 focuses on general liability, the Professional Liability Endorsement is tailored for professionals, such as consultants or service providers. Both documents serve to protect against claims, but they cater to different aspects of liability exposure, ensuring that various risks are covered appropriately.

When filling out the CG 20 10 07 04 Liability Endorsement form, it is essential to pay attention to detail. Here are some important dos and don'ts to consider:

This endorsement does not grant unlimited coverage. It only covers liability for specific injuries or damages related to your operations for the additional insured, as outlined in the policy.

Coverage is limited to the activities specified in the endorsement. If the claim is unrelated to your operations, it may not be covered.

This endorsement does not increase the limits of insurance. The coverage for additional insureds is capped at the lesser of the contract requirements or the existing policy limits.

The endorsement specifically addresses "bodily injury," "property damage," and "personal and advertising injury." Other types of claims may not be covered.

Coverage is not applicable once all work related to the project is completed. If the injury occurs after the project is finished, the endorsement does not apply.

Only those named in the schedule can be added as additional insureds. This must be clearly stated in the policy.

Coverage is limited to what is required by the contract. If the contract specifies less coverage, that is all that will be provided.

Coverage is restricted to the locations and operations specified in the endorsement. If a location is not listed, it is not covered.

When filling out and using the CG 20 10 07 04 Liability Endorsement form, consider the following key takeaways: