When navigating the landscape of state taxes and business compliance, the BOS DTF-802 form serves as a critical document for businesses and individuals alike. This form is essential for those who need to report and manage their tax obligations accurately within the state of New York. The BOS DTF-802 involves several key elements, including reporting the sales and use tax for certain transactions, updating taxpayer information, and ensuring adherence to tax regulations. By completing the form, taxpayers can avoid penalties and ensure their business operations remain compliant with state laws. It's important to pay close attention to the various sections of the form, as they require specific details about sales, exemptions, and other tax-related matters. Understanding the nuances of this form can significantly influence your financial responsibilities and help maintain smooth business operations.

Department of Taxation and Finance

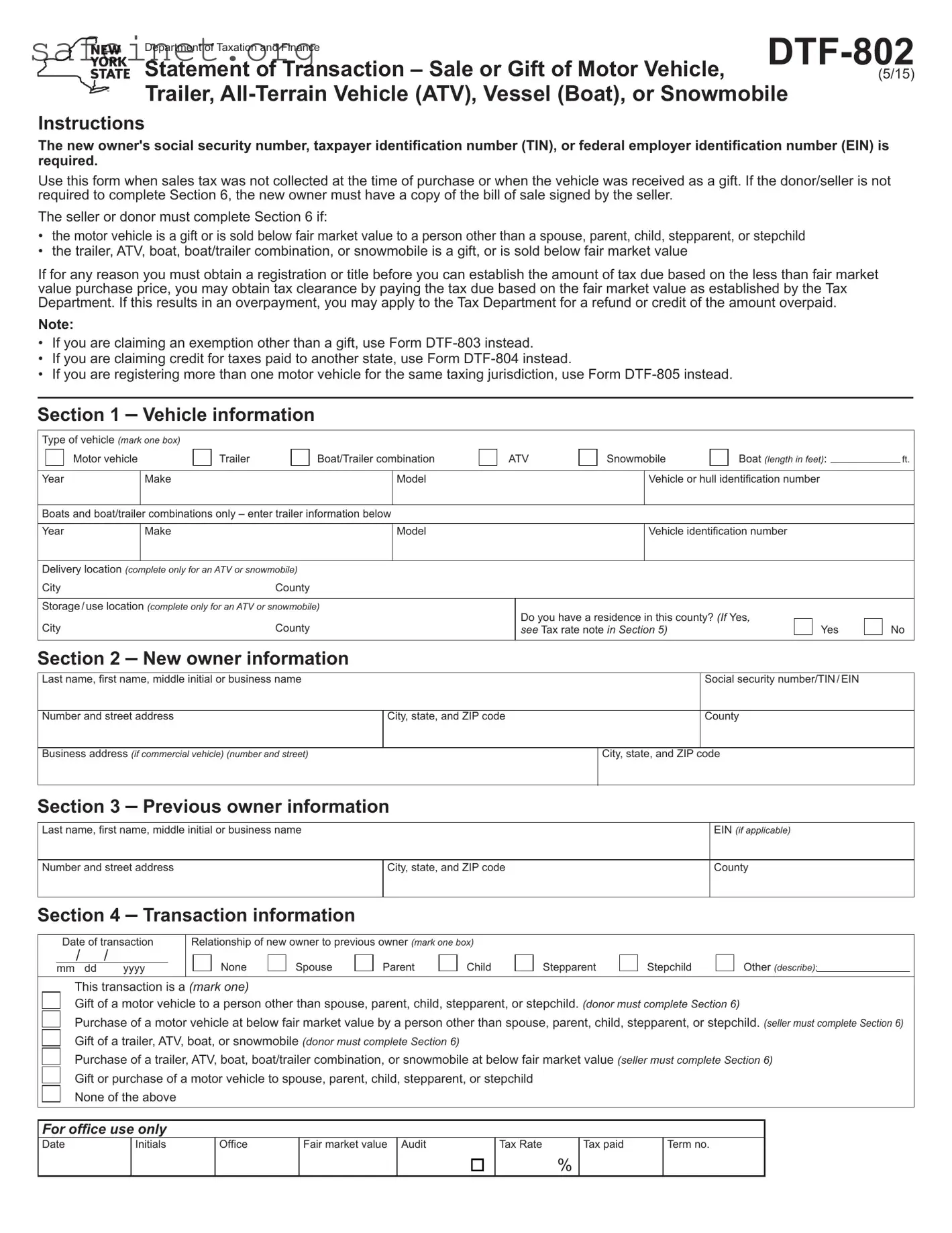

Statement of Transaction – Sale or Gift of Motor Vehicle,

Trailer,

Instructions

The new owner's social security number, taxpayer identification number (TIN), or federal employer identification number (EIN) is required.

Use this form when sales tax was not collected at the time of purchase or when the vehicle was received as a gift. If the donor/seller is not required to complete Section 6, the new owner must have a copy of the bill of sale signed by the seller.

The seller or donor must complete Section 6 if:

•the motor vehicle is a gift or is sold below fair market value to a person other than a spouse, parent, child, stepparent, or stepchild

•the trailer, ATV, boat, boat/trailer combination, or snowmobile is a gift, or is sold below fair market value

If for any reason you must obtain a registration or title before you can establish the amount of tax due based on the less than fair market value purchase price, you may obtain tax clearance by paying the tax due based on the fair market value as established by the Tax Department. If this results in an overpayment, you may apply to the Tax Department for a refund or credit of the amount overpaid.

Note:

•If you are claiming an exemption other than a gift, use Form

•If you are claiming credit for taxes paid to another state, use Form

•If you are registering more than one motor vehicle for the same taxing jurisdiction, use Form

Section 1 – Vehicle information

Type of vehicle (mark one box) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

Motor vehicle |

|

Trailer |

|

|

Boat/Trailer combination |

|

|

ATV |

|

Snowmobile |

|

|

Boat (length in feet): |

|

|

ft. |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year |

|

Make |

|

|

|

|

|

|

Model |

|

|

|

|

Vehicle or hull identification number |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Boats and boat/trailer combinations only – enter trailer information below |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year |

|

Make |

|

|

|

|

|

|

Model |

|

|

|

|

Vehicle identification number |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Delivery location (complete only for an ATV or snowmobile) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

City |

|

|

|

County |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Storage/use location (complete only for an ATV or snowmobile) |

|

Do you have a residence in this county? (If Yes, |

|

|

|

|

|

|

|||||||||||||||||||

City |

|

|

|

County |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

see Tax rate note in Section 5) |

|

|

|

|

Yes |

|

No |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Section 2 – New owner information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Last name, first name, middle initial or business name |

|

|

|

|

|

|

|

|

|

|

Social security number/TIN/EIN |

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Number and street address |

|

|

|

|

|

City, state, and ZIP code |

|

|

|

|

|

County |

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Business address (if commercial vehicle) (number and street) |

|

|

|

|

|

|

|

|

City, state, and ZIP code |

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

Section 3 – Previous owner information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Last name, first name, middle initial or business name |

|

|

|

|

|

|

|

|

|

|

|

EIN (if applicable) |

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Number and street address |

|

|

|

|

|

City, state, and ZIP code |

|

|

|

|

|

|

County |

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Section 4 – Transaction information

Date of transaction

/ /

mm dd yyyy

Relationship of new owner to previous owner (mark one box)

None |

|

Spouse |

|

Parent |

|

Child |

Stepparent

Stepchild

Other (describe):

This transaction is a (mark one)

Gift of a motor vehicle to a person other than spouse, parent, child, stepparent, or stepchild. (donor must complete Section 6)

Purchase of a motor vehicle at below fair market value by a person other than spouse, parent, child, stepparent, or stepchild. (seller must complete Section 6) Gift of a trailer, ATV, boat, or snowmobile (donor must complete Section 6)

Purchase of a trailer, ATV, boat, boat/trailer combination, or snowmobile at below fair market value (seller must complete Section 6) Gift or purchase of a motor vehicle to spouse, parent, child, stepparent, or stepchild

None of the above

For office use only

Date

Initials

Office

Fair market value Audit

Tax Rate

%

Tax paid

Term no.

Page 2 of 2

Section 5 – Purchase information

1 Purchase price |

|

Value |

|

a. Amount of cash payment |

1a |

$ |

|

b. Balance of payments assumed |

1b |

$ |

|

c. Value of property given, traded, or swapped, or services performed instead of cash payment... |

1c |

$ |

|

.......................................................................................................d. Purchase price (total of lines 1a, 1b, and 1c) |

|

1d |

$ |

Boats and boat/trailer combinations: For purchases or uses on or after June 1, 2015, tax only applies to the first $230,000 of the purchase price. Do not enter more than $230,000 on line 1d.

2Was this transaction the purchase or gift of a motor vehicle

|

from your spouse, parent, child, stepparent, or stepchild? |

|

|

Yes (enter 0 on line 4; no tax is due) |

|

No (continue to line 3) |

||

3 |

Tax rate* (enter as a decimal) |

|

|

|

|

|

|

|

|

|

|

|

3 |

|

|||

4 |

..................................................................................................................Sales tax due (multiply line 1d by line 3) |

|

|

|

|

4 |

$ |

|

5Is the amount on line 1d lower than fair market value?

* |

|

|

Yes (seller/donor must complete Section 6) |

|

No (sign certification below) |

|

N/A (Sale of boat for more than $230,000) |

Tax rate note: For a motor vehicle, trailer, boat, or boat/trailer combination use the tax rate of the new owner's place of residence. If the purchaser is a resident in two |

|||||||

or more counties in the state, use the rate in effect in the place where the motor vehicle, trailer, boat, or boat/trailer combination will be principally used or garaged. If the new owner is a business, use the tax rate of the place of business. If the business has locations in two or more counties in the state, use the rate in effect in the place where the motor vehicle, trailer, or boat will be principally used or garaged. For an ATV or snowmobile, use the higher rate of where the new owner took delivery, or where the vehicle is stored or used if new owner has a residence in storage/use locality.

Purchaser certification – I certify that the above statements are true and complete; and I make these statements with the knowledge that willfully issuing a false or fraudulent statement with the intent to evade tax is a misdemeanor under Tax Law section 1817(b), and Penal Law section 210.45, punishable by a fine up to $10,000 for an individual and $20,000 for a corporation.

Signature

Date

If this form is submitted by someone other than the new owner/lessee, provide the following:

Name/business name

Social security number, TIN, or federal EIN

Address

Section 6 – Affidavit of sale or gift of a motor vehicle, trailer, ATV, vessel (boat), or snowmobile

The seller or donor must complete if:

•the motor vehicle is a gift to a person other than a spouse, parent, child, stepparent, or stepchild

•the motor vehicle is sold below fair market value to a person other than a spouse, parent, child, stepparent, or stepchild

•the trailer, ATV, boat, or snowmobile is a gift

•the trailer, ATV, boat, boat/trailer combination, or snowmobile is sold below fair market value

6 Cash payment received |

6 |

$ |

7If, as a condition for the sale or gift of the vehicle or boat, the purchaser/recipient did any of the following in addition to, or in lieu of, a cash payment, mark an X in the appropriate box and indicate the value of the service or goods you received.

Value

a Performed any service |

Yes |

No |

7a $ |

|

b Assumed any debt |

Yes |

No |

7b $ |

|

c Traded/swapped a vehicle or other property |

Yes |

No |

7c $ |

|

d Total selling price (total of lines 6, 7a, 7b and 7c) |

|

|

|

|

|

7d $ |

|||

8Complete only if a corporation or business is the seller/donor

a |

Was or is the purchaser/recipient an employee, officer, or stockholder of the company/corporation? |

Yes |

b |

Was the transaction part of any terms of employment, employment contract, or termination agreement? |

Yes |

9If you answered Yes to any part of line 7 or line 8, provide an explanation:

No No

Seller/Donor certification – I have reviewed the information on Form

Signature

Name (printed or typed)

Date

Privacy notification – See our Web site at www.tax.ny.gov or Publication 54, Privacy Notification.

| Fact Name | Description |

|---|---|

| Form Purpose | The BOS DTF-802 form is used to document and manage business tax obligations in the state. |

| Governing Law | This form is governed by New York State tax laws, specifically under Title 1 of Article 22 of the New York State Tax Law. |

| Eligibility | Only businesses registered in New York are eligible to submit this form. |

| Submission Deadline | The form must be submitted by the end of the fiscal year to ensure compliance with state regulations. |

Completing the BOS DTF-802 form is straightforward, and following the steps carefully will ensure that your form is filled out correctly. This form may require specific details about your situation, so it’s important to have all necessary information on hand before you start.

What is the BOS DTF-802 form?

The BOS DTF-802 form is used for specific tax-related purposes in the state of New York. It allows taxpayers to claim certain exemptions, and it is often needed when dealing with business transactions or purchases that qualify for tax reductions or exemptions. Having this form completed correctly ensures compliance with state tax laws.

Who needs to fill out the BOS DTF-802 form?

Any individual or business entity that qualifies for a tax exemption or reduction under specific circumstances must fill out this form. This typically includes certain nonprofit organizations, businesses engaged in qualifying activities, or residents applying for specific tax benefits.

Where can I obtain the BOS DTF-802 form?

You can download the BOS DTF-802 form from the New York State Department of Taxation and Finance website. It may also be available at local tax offices or through authorized state tax agents. Ensure that you are using the most recent version of the form to avoid any issues.

How do I fill out the BOS DTF-802 form?

Filling out the BOS DTF-802 form involves entering your personal or business information, details about the exemption you are claiming, and any other required information. Carefully read the instructions provided with the form to complete it accurately. If you're unsure about any section, consider seeking guidance from a tax professional.

When is the BOS DTF-802 form due?

The due date for submitting the BOS DTF-802 form varies depending on the specific tax situation it relates to. Generally, it should be submitted alongside your tax filings, but it’s essential to check the New York State Department of Taxation and Finance website for specific deadlines related to your circumstances.

Are there any fees associated with submitting the BOS DTF-802 form?

No fees are typically associated with submitting the BOS DTF-802 form itself. However, certain tax transactions or exemptions may have associated costs, so it’s wise to review the relevant details to understand any other potential expenses involved.

What happens after I submit the BOS DTF-802 form?

After submitting your BOS DTF-802 form, it will be reviewed by the appropriate tax authority. You may receive confirmation or additional requests for documentation if needed. It's important to keep a copy of the submitted form for your records and to stay alert for any responses from the authorities.

What if I make a mistake on the BOS DTF-802 form?

If you realize that you made a mistake on the BOS DTF-802 form after submission, it's important to correct it as soon as possible. You might need to resubmit the form with the corrections and include a note explaining the changes. Contacting the New York State Department of Taxation and Finance can provide guidance on how to proceed with an amendment.

Not providing accurate personal information. Information such as name, address, and taxpayer identification number must be precise. Any error can delay processing.

Missing signatures. A common oversight is failing to sign the form. Each required signature ensures the validity of the submission.

Incorrectly reporting income. Make sure to accurately reflect all sources of income. Inconsistencies can trigger audits or further inquiries.

Failing to include necessary documentation. Supporting documents must accompany the form. Missing documents can lead to denial or suspension of benefits.

Using outdated forms. Always verify that you are using the most current version of the BOS DTF-802. Older versions may not be accepted.

Ignoring deadlines. Submit the form within the specified time frame. Late submissions can result in penalties or loss of eligibility.

Overlooking local regulations. Each state may have its own requirements. Confirm compliance with your local jurisdiction to avoid complications.

Providing incomplete information. Fill out every section of the form thoroughly. Leaving sections blank can lead to incomplete processing.

Incorrectly calculating amounts. Double-check all figures, especially income and deductions. Simple math errors can impact your results significantly.

Not keeping a copy of the submission. Make a copy of the completed form for your records. This can serve as proof of submission if needed later.

The BOS DTF-802 form is commonly associated with various processes in the United States, particularly in contexts involving business and tax matters. Alongside this form, several other documents play crucial roles in ensuring accurate reporting and compliance. Below is a list of forms and documents that complement the BOS DTF-802, each serving a specific purpose.

Each of these documents interacts with the BOS DTF-802 form in specific ways, contributing to a comprehensive framework of tax compliance and business reporting. Understanding their function and necessity is vital for both individuals and organizations, ensuring that they remain informed and compliant with the applicable regulations.

The BOS DTF-802 form, often a vital part of the tax process, shares similarities with several other documentation types related to financial reporting and compliance. Each of these documents serves specific purposes but also intersects with the functions and requirements outlined in the DTF-802. Understanding these connections can help individuals and businesses navigate their obligations more effectively.

One particularly similar document is the IRS Form 1040, which individual taxpayers use to report their income and calculate their tax liability. Like the BOS DTF-802, the Form 1040 requires detailed financial information about income, deductions, and credits. Both documents ultimately aim to ensure accuracy in tax reporting and compliance, though the 1040 is focused on personal income tax while the DTF-802 may pertain to broader financial analysis or reporting requirements.

The W-2 form, issued by employers to employees, captures wages and tax withholding information. This document is crucial for accurate income reporting, just as the DTF-802 is essential for certain tax calculations or compliance tasks within businesses. Both forms involve reporting crucial financial information to tax authorities and are used to verify income and tax obligations.

Another similar document is the 1099 form, which is used for various types of income other than wages, salaries, or tips. Freelancers and independent contractors often receive a 1099 to report their earnings. This form shares the aspect of detailing specific income streams and their tax implications, akin to certain sections of the BOS DTF-802 that may request similar information from businesses or individuals.

The Schedule C (Form 1040) allows self-employed individuals to report income or loss from their business. This document, like the BOS DTF-802, enables a clear presentation of financial activity, helping to capture the essence of a business's performance. Both forms are integral for accurately reporting earnings and expenses, informing tax authorities about a taxpayer's financial health.

Another document is the Form 941, the Employer's Quarterly Federal Tax Return. Employers use this form to report income taxes, Social Security tax, and Medicare tax withheld from employee paychecks. Just as the DTF-802 collects pertinent financial data for evaluating tax situations, Form 941 helps ensure that employers are accurately reporting payroll taxes and complying with federal requirements.

The K-1 form, used to report income, deductions, and credits from partnerships, shares a common objective with the BOS DTF-802. Each document serves to inform the tax authority about the financial results of a partnership or business entity. Both K-1 and DTF-802 require detailed financial information, ensuring accurate reflection of earnings and losses attributed to each member or stakeholder.

The Sales Tax Return form is designed for businesses to report sales tax they have collected from customers. Like the DTF-802, this return provides tax authorities with essential information about a business's financial dealings, specifically concerning taxation. Both documents are critical in ensuring compliance with tax obligations and contribute to the overall financial health of a business.

Finally, the Form 990 assists non-profit organizations in reporting their financial information to the IRS. Similar to the DTF-802, the Form 990 provides transparency about financial activities to ensure compliance with regulatory requirements. Both documents aim to foster accurate financial reporting and accountability, whether for a profit or non-profit entity.

When completing the BOS DTF-802 form, attention to detail is crucial. The following list outlines essential dos and don'ts to ensure accuracy and compliance.

The BOS DTF-802 form can often confuse taxpayers and businesses alike. Here are 9 common misconceptions about this form:

When dealing with the BOS DTF-802 form, there are several important points to keep in mind. These takeaways will help you understand how to fill out and use the form effectively.