In Arkansas, a Promissory Note serves as a vital financial document, outlining the terms of a loan between a borrower and a lender. This form typically includes essential details such as the principal amount, interest rate, repayment schedule, and any applicable fees. It is designed to protect both parties by clearly stating their rights and obligations. While the Promissory Note can be customized to fit specific agreements, it generally requires signatures from both the borrower and the lender to validate the contract. Understanding the components of this form is crucial for anyone involved in lending or borrowing money, as it lays the groundwork for a transparent financial relationship. Whether for personal loans, business financing, or real estate transactions, a well-crafted Promissory Note can help prevent misunderstandings and disputes down the line.

Arkansas Promissory Note Template

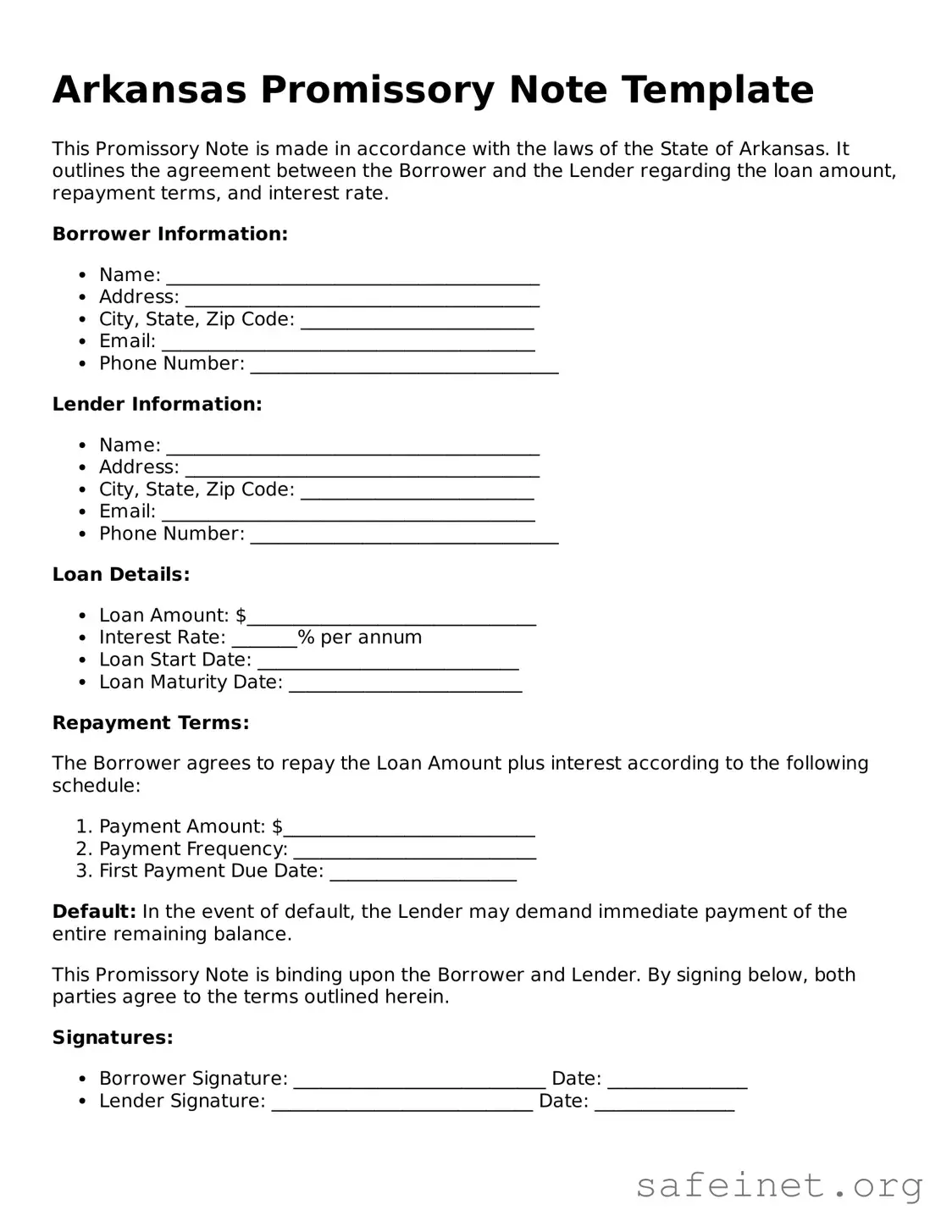

This Promissory Note is made in accordance with the laws of the State of Arkansas. It outlines the agreement between the Borrower and the Lender regarding the loan amount, repayment terms, and interest rate.

Borrower Information:

Lender Information:

Loan Details:

Repayment Terms:

The Borrower agrees to repay the Loan Amount plus interest according to the following schedule:

Default: In the event of default, the Lender may demand immediate payment of the entire remaining balance.

This Promissory Note is binding upon the Borrower and Lender. By signing below, both parties agree to the terms outlined herein.

Signatures:

| Fact Name | Description |

|---|---|

| Definition | An Arkansas promissory note is a written promise to pay a specific amount of money to a designated person or entity at a specified time or on demand. |

| Governing Law | Promissory notes in Arkansas are governed by the Uniform Commercial Code (UCC), specifically Article 3, which pertains to negotiable instruments. |

| Essential Elements | The note must include the principal amount, interest rate, payment terms, and the signatures of the parties involved. |

| Interest Rates | Arkansas does not impose a specific cap on interest rates for promissory notes, but they must comply with general usury laws. |

| Enforcement | If the borrower fails to repay, the lender can enforce the note through legal proceedings, seeking repayment or damages. |

| Transferability | Promissory notes in Arkansas can be transferred or assigned to another party, making them negotiable instruments under the UCC. |

After obtaining the Arkansas Promissory Note form, you will need to fill it out carefully. Ensure that all required information is accurate and complete to avoid any potential issues later. Follow these steps to fill out the form correctly.

What is a promissory note in Arkansas?

A promissory note is a written promise to pay a specific amount of money to a designated person or entity at a specified time or on demand. In Arkansas, it serves as a legal document that outlines the terms of the loan, including the principal amount, interest rate, and repayment schedule.

What are the essential elements of an Arkansas promissory note?

To be valid, a promissory note in Arkansas must include the following elements: the names of the borrower and lender, the principal amount, the interest rate, the repayment terms, and the date of the agreement. Additionally, it should be signed by the borrower to confirm their commitment to repay the loan.

Do I need a lawyer to create a promissory note in Arkansas?

No, you do not necessarily need a lawyer to create a promissory note in Arkansas. However, consulting a legal professional can help ensure that the document complies with state laws and protects your interests. A well-drafted note can prevent misunderstandings and disputes in the future.

Can a promissory note be modified after it is signed?

Yes, a promissory note can be modified after it is signed, but both parties must agree to the changes. It is advisable to document any modifications in writing and have both parties sign the amended agreement to avoid potential disputes later.

What happens if the borrower defaults on the promissory note?

If the borrower defaults, the lender has the right to take legal action to recover the owed amount. This may involve filing a lawsuit or pursuing other collection methods. The specific remedies available will depend on the terms outlined in the note and applicable Arkansas laws.

Is a promissory note enforceable in Arkansas?

Yes, a properly executed promissory note is enforceable in Arkansas. Courts generally uphold these agreements as long as they meet the legal requirements and do not violate any laws. If a dispute arises, the note can serve as evidence in court.

Are there any specific laws governing promissory notes in Arkansas?

While there are no specific statutes solely dedicated to promissory notes in Arkansas, general contract law governs their creation and enforcement. It is essential to ensure that the note complies with state contract laws to be valid and enforceable.

Can a promissory note be used for personal loans?

Yes, promissory notes are commonly used for personal loans between individuals. They provide a clear record of the loan terms and can help both parties understand their rights and obligations. Whether borrowing from a friend or family member, a written note can prevent misunderstandings.

Not including the date at the top of the form. This is essential for tracking the timeline of the loan.

Failing to clearly state the amount borrowed. This should be written both in numbers and words to avoid confusion.

Omitting the interest rate. If there is an interest charge, it must be specified to ensure both parties understand the total repayment amount.

Not defining the payment schedule. Indicate when payments are due, whether monthly, weekly, or otherwise, to prevent misunderstandings.

Leaving out the borrower’s and lender’s names. Full legal names should be used to identify who is involved in the agreement.

Not including a default clause. This outlines what happens if the borrower fails to make payments, providing clarity for both parties.

Forgetting to add signatures. Both the borrower and lender must sign the document for it to be legally binding.

Neglecting to keep a copy of the signed note. Both parties should have a copy for their records to reference in the future.

When dealing with a promissory note in Arkansas, several other forms and documents may be necessary to ensure clarity and legality in the transaction. These documents help define the terms, secure the loan, and provide necessary disclosures. Here are some commonly used forms alongside the Arkansas Promissory Note.

Using these additional documents alongside the Arkansas Promissory Note can help clarify expectations and protect the interests of both the lender and the borrower. Proper documentation is essential for a smooth transaction.

The Arkansas Promissory Note form shares similarities with a Loan Agreement. Both documents outline the terms of a loan, including the amount borrowed, the interest rate, and the repayment schedule. A Loan Agreement may include additional details such as collateral, which can provide further security for the lender. However, a Promissory Note is generally simpler and focuses primarily on the borrower's promise to repay the loan.

Another document that resembles the Arkansas Promissory Note is the IOU. An IOU is a more informal acknowledgment of a debt, typically lacking the detailed terms found in a Promissory Note. While an IOU states that one party owes money to another, it does not usually specify repayment terms or interest rates, making it less formal and enforceable than a Promissory Note.

A Personal Loan Agreement is also similar to the Arkansas Promissory Note. Like a Promissory Note, it outlines the terms of a loan between individuals. However, a Personal Loan Agreement often includes additional provisions, such as the purpose of the loan or conditions for default, which can provide more clarity and protection for both parties involved.

The Mortgage Note is another document that has a close relationship with the Promissory Note. A Mortgage Note is specifically used in real estate transactions, where the borrower promises to repay a loan secured by property. While both documents serve to confirm a borrower's obligation to repay, the Mortgage Note includes terms related to the property and the consequences of default, such as foreclosure.

A Commercial Promissory Note is similar in nature to the Arkansas Promissory Note but is specifically designed for business transactions. This type of note outlines the loan terms for a business, including interest rates and repayment schedules, and can be used for various purposes, such as purchasing equipment or funding operations. The key difference lies in its application to commercial rather than personal loans.

Another related document is the Secured Promissory Note. This document not only includes the borrower's promise to repay but also specifies collateral that secures the loan. By doing so, it provides the lender with additional protection in case of default, making it a more secure option compared to an unsecured Promissory Note.

The Demand Note is also akin to the Arkansas Promissory Note, with a crucial distinction. A Demand Note allows the lender to request repayment at any time, making it more flexible than a standard Promissory Note, which typically has a set repayment schedule. This type of note is often used in situations where the lender may need immediate access to funds.

A Certificate of Deposit (CD) can be compared to a Promissory Note as both involve a promise to pay. However, a CD is a financial product offered by banks, where the depositor agrees to leave money in the bank for a specified period in exchange for interest. Unlike a Promissory Note, which is a promise from a borrower to a lender, a CD represents a bank's promise to return the deposit with interest.

The Loan Note is another document similar to the Arkansas Promissory Note. It serves as a written agreement between a borrower and lender, detailing the loan amount, interest rate, and repayment terms. While both documents fulfill the same purpose, a Loan Note may also include additional clauses that address the rights and responsibilities of both parties, providing a more comprehensive understanding of the loan agreement.

Finally, the Repayment Agreement can be likened to the Arkansas Promissory Note. This document outlines the terms under which a borrower agrees to repay a debt, similar to a Promissory Note. However, a Repayment Agreement may be used in various contexts, such as settling debts or restructuring payment terms, and can include more extensive conditions and timelines than a standard Promissory Note.

When filling out the Arkansas Promissory Note form, it is crucial to approach the task with care. Below are some important do's and don'ts to consider:

Understanding the Arkansas Promissory Note form can be challenging. Here are ten common misconceptions about this important financial document.

Clarifying these misconceptions can help individuals navigate the process of creating and using a promissory note effectively.

When dealing with the Arkansas Promissory Note form, it’s essential to understand its components and implications. Here are some key takeaways to keep in mind: