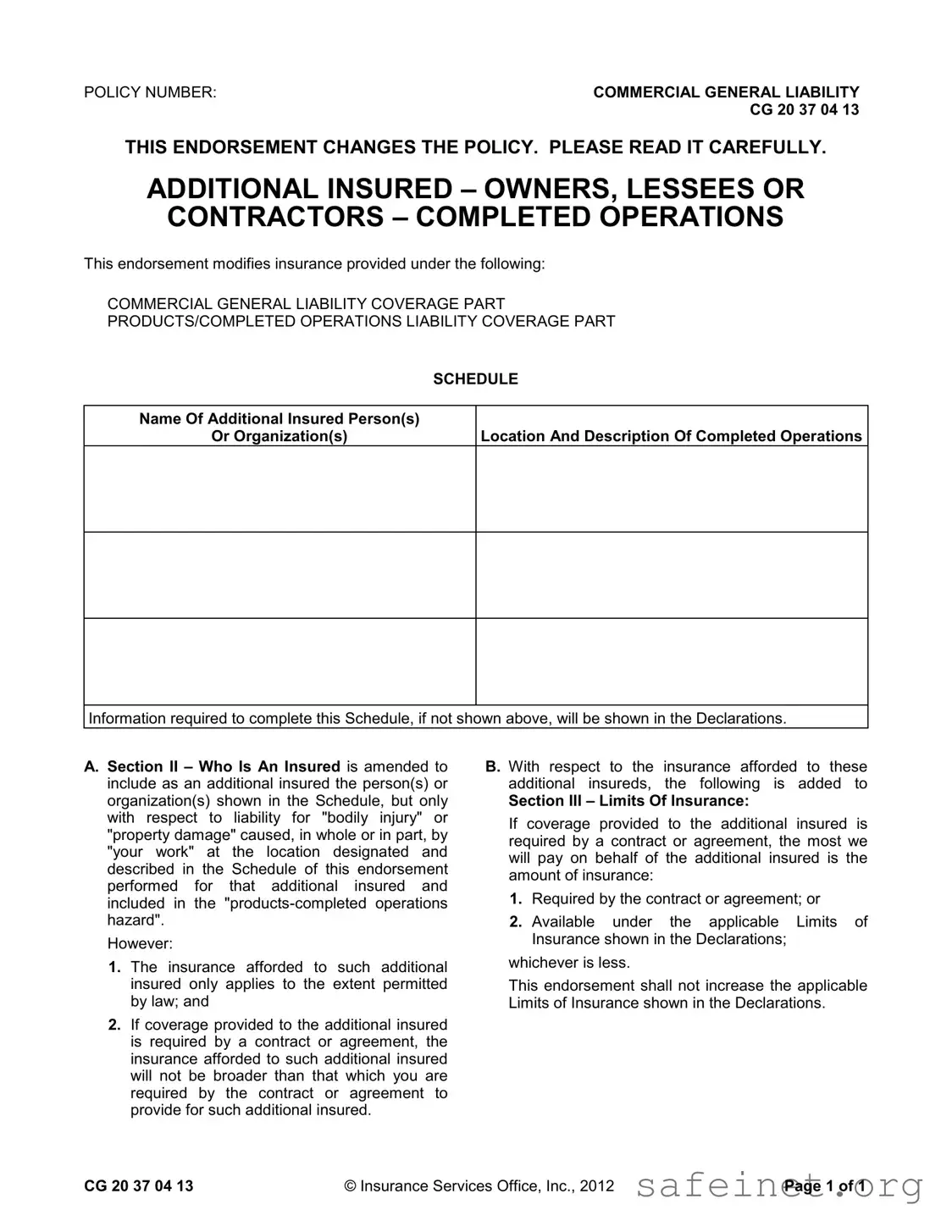

The Additional Insured form is a crucial document in the realm of commercial general liability insurance, particularly for businesses engaged in contracting or subcontracting work. It allows a third party, such as an owner or contractor, to be added as an insured party under an existing insurance policy. This endorsement is specifically designed to provide coverage for liabilities arising from completed operations, ensuring that the additional insured is protected against claims related to bodily injury or property damage caused by the work performed. When completing this form, it is essential to specify the names of the additional insured parties and the locations where the work was done, as this information directly influences the scope of coverage. The form also outlines important limitations, such as ensuring that the insurance provided does not exceed what is required by any underlying contract. Furthermore, it clarifies that the coverage for the additional insured is subject to the same limits as stated in the policy declarations, ensuring that there are no surprises when it comes to the extent of protection offered. Understanding these key aspects can help businesses navigate their insurance needs more effectively, fostering better relationships with clients and contractors alike.

| Fact Name | Details |

|---|---|

| Purpose | The Additional Insured form provides liability coverage to third parties, such as owners or contractors, for specific operations performed by the insured. |

| Modification | This form modifies the existing Commercial General Liability policy to include additional insured parties. |

| Coverage Scope | Coverage is limited to liability for bodily injury or property damage arising from the insured's work. |

| Contractual Requirement | If coverage is required by a contract, it will not exceed the terms specified in that contract. |

| Limits of Insurance | The maximum amount payable to an additional insured is the lesser of the contract requirement or the policy limits. |

| Governing Law | State-specific laws govern the application of this form, which may vary by jurisdiction. |

| Completed Operations | This form specifically covers completed operations as defined in the policy. |

| Schedule Requirement | Details about additional insured parties and operations must be listed in the Schedule or Declarations. |

| Limitations | The endorsement does not increase the overall limits of insurance stated in the policy. |

Filling out the Additional Insured form is a straightforward process that requires careful attention to detail. This form is essential for ensuring that specific parties are covered under your insurance policy for certain liabilities. By completing it correctly, you help protect both yourself and the entities involved in your operations.

What is the purpose of the Additional Insured form?

The Additional Insured form is designed to extend liability coverage to individuals or organizations that are not the primary policyholder but may be exposed to liability due to the actions of the policyholder. This is particularly relevant in construction and service contracts where subcontractors or service providers may need to protect the interests of the owners or general contractors. By adding these parties as additional insureds, the policy ensures that they are covered for any bodily injury or property damage that arises from the work performed by the primary insured at the specified location.

Who qualifies as an additional insured under this endorsement?

The endorsement specifically includes individuals or organizations listed in the schedule section of the form. These additional insureds must be connected to the completed operations of the primary insured. Their coverage is limited to liability for bodily injury or property damage caused, in whole or in part, by the work of the primary insured. It is crucial that the work be performed for the additional insured and fall under the products-completed operations hazard to qualify for coverage.

Are there limitations to the coverage provided to additional insureds?

Yes, there are important limitations. First, the coverage provided to additional insureds is only applicable to the extent permitted by law. Second, if the coverage is mandated by a contract or agreement, it cannot exceed what is specified in that contract. This means that if a contract requires a certain level of coverage, the insurance provided will not be broader than what the contract stipulates. Additionally, the endorsement does not increase the overall limits of insurance available under the policy.

How does the endorsement affect the limits of insurance?

The endorsement outlines that the most the insurer will pay on behalf of the additional insured is determined by two factors: the amount required by the contract or agreement, and the limits of insurance available as stated in the policy declarations. The lower of these two amounts will apply. Importantly, the endorsement does not enhance the overall limits of insurance outlined in the declarations, meaning that the primary insured must still operate within those existing limits.

What should policyholders consider before adding someone as an additional insured?

Policyholders should carefully review the terms of the contract or agreement that necessitates adding an additional insured. Understanding the specific coverage requirements and limitations is essential. Additionally, it is advisable to assess the risks associated with the operations being performed and how they might impact both the policyholder and the additional insured. Consulting with an insurance professional can provide clarity on the implications of adding additional insureds and ensure compliance with contractual obligations.

Neglecting to Include Complete Information: Failing to provide the full name of the additional insured can lead to confusion and coverage issues. Always ensure that the name is accurate and complete.

Omitting Location Details: Not specifying the location where the completed operations took place is a common mistake. This information is crucial for determining the scope of coverage.

Incorrect Policy Number: Entering an incorrect policy number can render the form invalid. Double-check this detail to avoid complications later.

Misunderstanding the Scope of Coverage: Many people fail to grasp that the coverage provided is limited to what is specified in the contract. Be clear on the terms to avoid misunderstandings.

Ignoring Contractual Obligations: If the additional insured status is required by a contract, ensure that the coverage does not exceed what is stipulated. This can prevent unnecessary liability.

Failing to Review Limits of Insurance: It’s essential to understand the limits of insurance that apply. Not doing so can lead to unexpected gaps in coverage.

Not Keeping Copies: Failing to keep a copy of the completed form for your records can lead to disputes later. Always retain a copy for your files.

Submitting Without a Review: Rushing to submit the form without a thorough review can result in errors. Take the time to check all entries for accuracy.

The Additional Insured form is a critical document in the world of insurance, particularly in the context of commercial general liability coverage. When businesses engage in contracts, they often need to ensure that additional parties are protected under their insurance policies. However, this form is typically accompanied by other important documents that serve various purposes in the insurance process. Here are six key forms and documents that are commonly used alongside the Additional Insured form.

Understanding these documents is essential for anyone involved in contracting or insurance. Each plays a unique role in ensuring that all parties are adequately protected and that the terms of coverage are clear. By familiarizing oneself with these forms, businesses can navigate the complexities of insurance with greater confidence and clarity.

The Additional Insured form is similar to the Certificate of Insurance (COI). A COI serves as proof that a business or individual has insurance coverage. It typically includes details about the policy, such as the type of coverage, limits, and the insured party's name. Like the Additional Insured form, a COI can provide assurance to third parties that they are protected under the insured's policy, though it does not extend coverage in the same way. Instead, it simply confirms the existence of coverage without modifying the terms of the policy.

Another document that shares similarities with the Additional Insured form is the Waiver of Subrogation. This waiver prevents an insurance company from pursuing a claim against a third party after compensating the insured for a loss. Both documents serve to protect specific parties involved in a contract or agreement. While the Additional Insured form expands coverage to another party, the Waiver of Subrogation ensures that the insurer cannot seek reimbursement from that party, thereby fostering better relationships between the involved parties.

The Indemnity Agreement is also comparable to the Additional Insured form. An indemnity agreement involves one party agreeing to compensate another for certain damages or losses. This document, like the Additional Insured form, aims to allocate risk between parties. While the Additional Insured form extends insurance coverage to another party, an indemnity agreement may require one party to cover losses that the other party incurs, thus providing a different mechanism for managing liability.

The Additional Insured form is similar to the Additional Named Insured endorsement. Both documents expand the coverage provided by an insurance policy, but they do so in different ways. The Additional Named Insured endorsement adds a new party to the policy as an insured, granting them the same rights as the original insured. In contrast, the Additional Insured form provides limited coverage to the additional insured, typically only for specific risks or liabilities. Both serve to clarify the relationships and responsibilities of the parties involved.

The Primary and Non-Contributory endorsement also bears resemblance to the Additional Insured form. This endorsement establishes that the insurance policy will respond first in the event of a claim, without seeking contribution from other insurance policies. Like the Additional Insured form, it is often used in contracts to define how coverage applies between parties. Both documents aim to clarify the extent of coverage and the order in which policies will respond to claims, thereby minimizing disputes over liability.

The Contractual Liability endorsement is another document that shares characteristics with the Additional Insured form. This endorsement allows for coverage of liabilities assumed under a contract. Similar to how the Additional Insured form extends coverage to another party based on contractual obligations, the Contractual Liability endorsement ensures that the insured's policy will cover certain liabilities that arise from their agreements with others. Both documents emphasize the importance of contractual relationships in determining insurance coverage.

The Professional Liability Insurance form is akin to the Additional Insured form in that it provides coverage for specific risks associated with professional services. While the Additional Insured form extends general liability coverage to additional parties, the Professional Liability Insurance form is tailored for professionals, protecting them against claims of negligence or malpractice. Both documents highlight the need for specialized coverage based on the nature of the work being performed.

The Umbrella Insurance policy is another document that can be compared to the Additional Insured form. An Umbrella policy provides additional coverage beyond the limits of underlying policies, including general liability. While the Additional Insured form extends coverage to additional parties under existing policies, an Umbrella policy offers broader protection that can cover various risks. Both serve to enhance the overall insurance coverage available to the insured, albeit in different ways.

Finally, the General Liability Insurance policy itself is fundamentally related to the Additional Insured form. The Additional Insured form modifies the General Liability policy to include additional parties as insureds under specific conditions. Both documents are integral to understanding the coverage landscape for businesses and individuals, as they define who is protected and under what circumstances. The relationship between them is essential for ensuring that all parties involved in a contract have the necessary insurance protections in place.

When filling out the Additional Insured form, attention to detail is crucial. Here are six important do's and don'ts to keep in mind:

By following these guidelines, you can ensure that the Additional Insured form is filled out correctly, protecting both yourself and the additional insured party effectively.

Understanding the Additional Insured form is crucial for anyone involved in contracts or insurance policies. Unfortunately, several misconceptions surround this important document. Here are five common misunderstandings:

By clarifying these misconceptions, individuals and organizations can better navigate their insurance needs and understand the implications of being named as an additional insured.

Understanding the Additional Insured form is crucial for anyone involved in contracts that require liability coverage. Here are some key takeaways:

By keeping these points in mind, you can navigate the complexities of the Additional Insured form more effectively and ensure proper coverage for all parties involved.