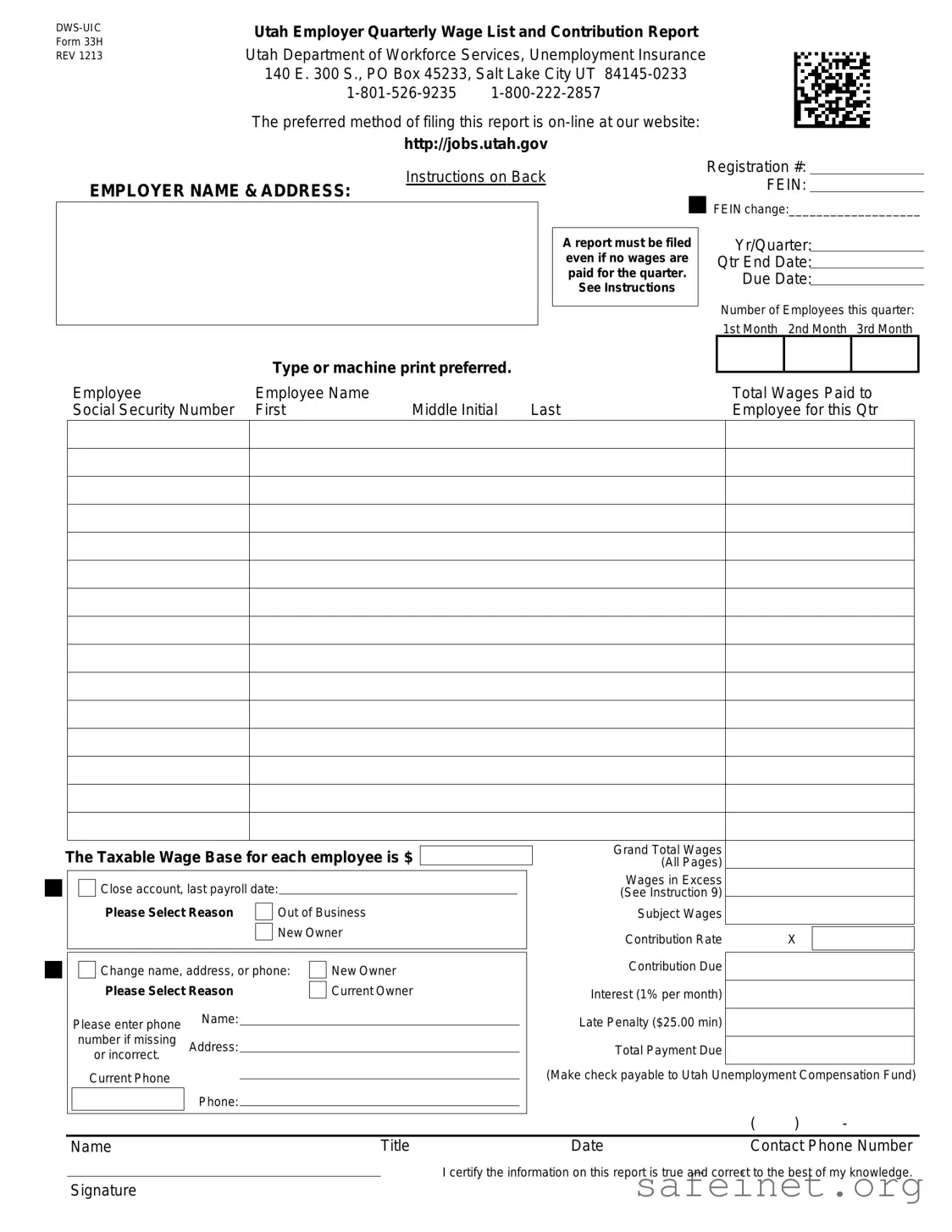

The 33H form, officially known as the DWS-UIC Utah Employer Quarterly Wage List and Contribution Report, serves a crucial role for employers in Utah. It is essential for tracking employee wages and ensuring compliance with unemployment insurance requirements. Every employer must submit this report, even in quarters where no wages are paid, highlighting its importance in maintaining accurate records. The form requires detailed information, including the employer's name, address, and registration number, as well as the total wages paid to each employee during the quarter. Additionally, it collects data on the number of employees and provides a breakdown of taxable wages, contribution rates, and any applicable penalties for late submissions. Employers can file this report online, making the process more accessible and efficient. The form also includes a certification section, where employers affirm the accuracy of the information provided. Understanding the nuances of the 33H form is vital for employers, as it not only impacts their compliance status but also their financial obligations to the Utah Unemployment Compensation Fund.

| Fact Name | Details |

|---|---|

| Form Title | DWS-UIC Utah Employer Quarterly Wage List and Contribution Report Form 33H |

| Governing Agency | Utah Department of Workforce Services |

| Contact Information | 140 E. 300 S., PO Box 45233, Salt Lake City UT 84145-0233, 1-801-526-9235, 1-800-222-2857 |

| Filing Method | The preferred method of filing is online at http://jobs.utah.gov. |

| Filing Requirement | A report must be filed even if no wages are paid for the quarter. |

| Employer Information | Employers must provide their name, address, registration number, and Federal Employer Identification Number (FEIN). |

| Quarterly Information | Employers need to specify the year, quarter end date, and due date for the report. |

| Wage Reporting | Employers must report total wages paid to employees for each month of the quarter. |

| Payment Details | Employers are required to calculate and report total payments due, including contributions and penalties, if applicable. |

Filling out the 33H form is a crucial step for employers in Utah to report wages and contributions for unemployment insurance. It’s important to ensure that all information is accurate and complete to avoid any potential issues. Here’s how to fill out the form step-by-step.

Once the form is completed, ensure that you review all entries for accuracy. It is recommended to submit the form online for efficiency, but you can also mail it to the address provided. Keep a copy for your records as well.

What is the 33H form?

The 33H form, officially known as the DWS-UIC Utah Employer Quarterly Wage List and Contribution Report Form, is used by employers in Utah to report wages paid to employees during a specific quarter. This form also includes information regarding unemployment insurance contributions. It is essential for compliance with state regulations regarding unemployment benefits.

Who needs to file the 33H form?

Any employer in Utah who has employees and pays wages must file the 33H form. This requirement holds even if no wages were paid during the quarter. Filing ensures that the state has accurate records for unemployment insurance purposes.

When is the 33H form due?

The due date for the 33H form coincides with the end of each quarter. Employers should be aware of these deadlines to avoid any late penalties. It’s advisable to check the specific due date for each quarter to ensure timely filing.

How can I file the 33H form?

The preferred method for filing the 33H form is online through the Utah Department of Workforce Services website. This method simplifies the process and allows for quicker processing. However, paper submissions are also accepted if necessary.

What information is required on the 33H form?

When completing the 33H form, employers must provide details such as their name and address, registration number, Federal Employer Identification Number (FEIN), total wages paid to each employee, and the number of employees for the quarter. Additionally, employers must certify that the information provided is accurate.

What happens if I miss the filing deadline?

If an employer misses the filing deadline for the 33H form, they may incur a late penalty, which is a minimum of $25. Additionally, interest may accrue on any unpaid contributions. It is crucial to file on time to avoid these extra costs.

Where can I find more information about the 33H form?

For additional details about the 33H form, including filing instructions and updates, employers can visit the Utah Department of Workforce Services website. They also provide contact information for assistance, should any questions arise during the filing process.

Neglecting to File a Report: Some employers mistakenly believe they do not need to file if no wages were paid during the quarter. However, a report must still be submitted even if there are no wages to report.

Incorrect Employer Information: Failing to provide accurate employer name and address can lead to delays or complications. Always double-check this information before submission.

Missing Registration Number: The registration number is crucial for identifying your business. Forgetting to include this can result in processing issues.

Errors in Employee Information: Inaccuracies in employee names or Social Security numbers can cause significant problems. Ensure all details are correct and clearly written.

Omitting Total Wages: It’s essential to calculate and report total wages accurately. Missing this information can lead to penalties or audits.

Incorrect Contribution Rate: Using the wrong contribution rate can affect your payment amount. Verify the current rate before finalizing the form.

Ignoring Late Penalties: If the form is submitted after the due date, a late penalty applies. Being aware of this can help avoid unnecessary fees.

Failure to Sign the Report: A signature is required to certify that the information provided is true and correct. Omitting this step can invalidate the report.

The Form 33H is a crucial document for employers in Utah, as it serves as the quarterly wage list and contribution report for unemployment insurance. However, several other forms and documents are often used in conjunction with this form to ensure compliance with state regulations. Below is a list of these documents, along with brief descriptions of their purposes.

Understanding these documents is essential for employers to maintain compliance with both state and federal regulations. Each form plays a specific role in the overall reporting and tax process, and keeping them organized will help streamline administrative tasks related to payroll and employee management.

The Form 941 is similar to the 33H form as it serves as a quarterly report for employers. It is used to report income taxes, Social Security tax, and Medicare tax withheld from employee wages. Employers must file Form 941 even if no wages were paid during the quarter. The information required includes the number of employees, total wages, and taxes withheld, making it a crucial document for tax compliance.

The W-2 form, also known as the Wage and Tax Statement, is another document that shares similarities with the 33H form. Employers use the W-2 to report annual wages and the taxes withheld from employees' paychecks. While the 33H focuses on quarterly reporting, the W-2 summarizes the entire year's earnings and tax contributions. Both documents are essential for ensuring accurate tax reporting and compliance with federal regulations.

The Form 940 is an annual report that employers file to report their Federal Unemployment Tax Act (FUTA) tax. Like the 33H, it requires employers to provide information about wages paid and the number of employees. While the 33H is quarterly, Form 940 is filed once a year, but both documents contribute to the overall understanding of an employer's payroll obligations.

The Utah State Tax Commission's TC-941 is another form that parallels the 33H. This form is used to report state income tax withholding for employees in Utah. Similar to the 33H, it requires details about wages and employee counts. Both forms are critical for ensuring compliance with state tax regulations and help maintain accurate records of employee compensation.

The Form 1099-MISC is a document that reports payments made to independent contractors and freelancers. While the 33H focuses on employee wages, the 1099-MISC serves a similar purpose in tracking payments for services rendered. Both forms are essential for tax reporting, ensuring that all income is documented for tax purposes.

The I-9 form, or Employment Eligibility Verification, is another document that complements the 33H. While the 33H reports wages and contributions, the I-9 verifies an employee's eligibility to work in the United States. Both forms are necessary for employers to maintain compliance with federal regulations, though they serve different functions within the employment process.

The Form 7004 is an application for an automatic extension of time to file certain business tax returns. Similar to the 33H, it is related to tax obligations for employers. While the 33H is a report of wages and contributions, Form 7004 allows businesses additional time to prepare their tax filings, ensuring they meet their financial responsibilities without incurring penalties.

The Form 1095-C is used by applicable large employers to report health insurance coverage offered to employees. This form is similar to the 33H in that it collects information about employee counts and benefits provided. Both forms contribute to compliance with federal regulations, with the 1095-C focusing on healthcare reporting and the 33H on wage and unemployment contributions.

The Form W-3 is a summary of all W-2 forms issued by an employer. Like the 33H, it consolidates information about employee wages and tax withholdings. While the 33H is a quarterly report, the W-3 is submitted annually to the Social Security Administration, ensuring accurate reporting of total wages and taxes for the year.

Lastly, the Form 1065 is used by partnerships to report income, deductions, gains, and losses. While the 33H focuses on employee wages and contributions, the 1065 serves a similar purpose for partnerships, summarizing financial performance for tax purposes. Both forms are vital for maintaining compliance with tax laws and ensuring accurate financial reporting.

When filling out the 33H form, it's important to follow specific guidelines to ensure accuracy and compliance. Here are five things you should and shouldn't do:

By adhering to these guidelines, you can help ensure a smooth and efficient filing process for the 33H form.

Misconceptions about the 33H form can lead to confusion and errors in filing. Here are seven common misunderstandings:

Understanding these misconceptions can help ensure accurate and timely filing of the 33H form, avoiding potential penalties and compliance issues.

Filling out the 33H form, known as the Utah Employer Quarterly Wage List and Contribution Report, is essential for employers in Utah. Here are some key takeaways to ensure a smooth process:

By following these key points, employers can navigate the 33H form with confidence and ensure compliance with Utah's unemployment insurance requirements.