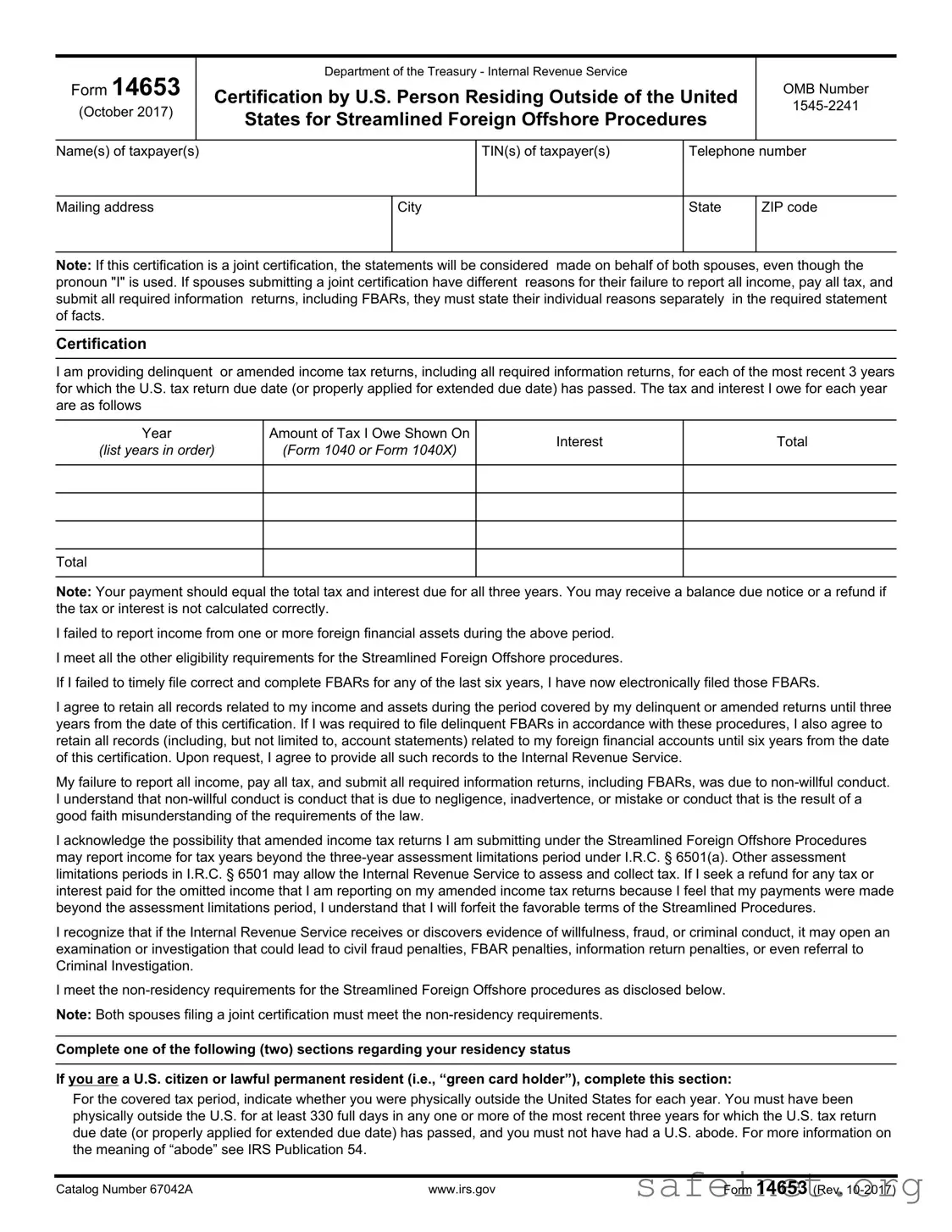

The 14653 form is an essential document for U.S. citizens and residents living abroad who wish to rectify their tax filings under the Streamlined Foreign Offshore Procedures. This form serves as a certification for individuals who have failed to report income from foreign financial assets, ensuring compliance with U.S. tax laws. It requires taxpayers to provide their personal information, including names, taxpayer identification numbers, and contact details. A key aspect of the 14653 form is the requirement to submit delinquent or amended income tax returns for the past three years, along with a detailed account of any tax owed and interest accrued. The form also emphasizes the need for a narrative statement explaining the reasons behind the failure to report income, which must include both favorable and unfavorable facts. Furthermore, it outlines the non-residency requirements that applicants must meet to qualify for the streamlined procedures, ensuring that both spouses in a joint certification adhere to these criteria. By completing this form, taxpayers agree to retain all relevant records and acknowledge the importance of transparency in their financial dealings with the Internal Revenue Service (IRS).

| Fact Name | Details |

|---|---|

| Form Purpose | Form 14653 is used by U.S. persons residing outside the United States to certify their eligibility for Streamlined Foreign Offshore Procedures. |

| Governing Law | The form operates under U.S. tax laws, specifically I.R.C. § 6501 and I.R.C. § 7701(b)(3). |

| Eligibility Requirements | Taxpayers must meet specific eligibility criteria, including non-willful conduct regarding tax reporting. |

| Joint Certification | If filing jointly, both spouses must meet the non-residency requirements and provide individual reasons for any discrepancies. |

| Record Retention | Taxpayers must retain records related to their income and foreign financial accounts for three to six years, depending on the circumstances. |

| Submission Requirements | Each submission must include a narrative statement of facts explaining the failure to report income and submit required returns. |

| Tax Years Covered | The form covers the most recent three tax years for which the U.S. tax return due date has passed. |

| OMB Control Number | The OMB Number for this form is 1545-2241, indicating its approval for use in compliance with federal regulations. |

Filling out Form 14653 is an important step for U.S. taxpayers residing outside the United States who need to certify their eligibility for certain tax procedures. Completing this form accurately is essential, as it will help facilitate your compliance with U.S. tax laws. Below are the steps to follow when filling out this form.

After completing the form, review it carefully to ensure all information is accurate and complete. Submitting an incomplete form could delay processing or disqualify you from the streamlined procedures. Once finalized, send it to the appropriate IRS address as indicated in the form instructions.

What is Form 14653 used for?

Form 14653 is used by U.S. persons living outside the United States to certify their eligibility for the Streamlined Foreign Offshore Procedures. This form allows individuals to report previously unreported income, pay any owed taxes, and avoid penalties associated with non-compliance. It simplifies the process for those who have not filed their taxes correctly due to non-willful conduct.

Who needs to file Form 14653?

U.S. citizens and lawful permanent residents who have failed to report all income, pay all taxes, or submit required information returns while residing outside the United States should file this form. It is specifically for individuals who can demonstrate that their failure was due to non-willful conduct, such as negligence or misunderstanding of tax obligations.

What information do I need to provide on Form 14653?

When filling out Form 14653, you need to provide your personal information, including your name, taxpayer identification number (TIN), and contact details. You must also report the years for which you are submitting delinquent or amended tax returns, the amount of tax owed, and any interest due. Additionally, you must explain the reasons for your failure to report income and provide details about your foreign financial accounts.

What happens if I do not provide a narrative statement of facts?

If you do not include a narrative statement explaining your failure to report income, your submission will be considered incomplete. This could result in your application not qualifying for the Streamlined Foreign Offshore Procedures, which means you may not receive the benefits of penalty relief. It's essential to provide a complete story, including both favorable and unfavorable facts.

How long should I keep records related to my income and assets?

You must retain all records related to your income and foreign financial assets for three years from the date of your certification. If you filed delinquent FBARs, keep those records for six years. This includes account statements and any documentation that supports your claims. Be prepared to provide these records to the IRS if requested.

Neglecting to Provide a Complete Narrative Statement: Many individuals fail to include a detailed narrative statement of facts explaining their failure to report income, pay taxes, or submit required information returns. This omission can lead to an incomplete submission, disqualifying them from penalty relief.

Incorrectly Calculating Tax and Interest: Some filers miscalculate the total tax and interest owed for the three years covered. It’s crucial to ensure that the payment matches the total amount listed on the form to avoid receiving a balance due notice or a refund.

Failing to Meet Non-Residency Requirements: Individuals often overlook the requirement that they must have been physically outside the United States for at least 330 full days in one or more of the past three years. Not meeting this criterion can invalidate their submission.

Not Separating Spousal Reasons: When filing jointly, spouses sometimes fail to provide separate reasons for their failures. If each spouse has different explanations, they must clearly state these individually to comply with the requirements.

Ignoring FBAR Filing Requirements: Some filers neglect to electronically file their delinquent FBARs for the required six-year period. This step is essential, as failure to do so can jeopardize their eligibility for the Streamlined Foreign Offshore Procedures.

Providing Incomplete Residency Computations: Non-citizens or non-residents sometimes fail to attach the necessary computations demonstrating they did not meet the substantial presence test. This lack of documentation can result in an incomplete submission.

Misunderstanding Non-Willful Conduct: Individuals may mistakenly believe that any failure to report is considered non-willful. It’s important to understand that non-willful conduct must stem from negligence or misunderstanding, not intentional disregard of the law.

Not Retaining Required Records: Some filers fail to retain all necessary records related to their income and assets for the required periods. Keeping these records is vital, as the IRS may request them to verify the information provided.

The Form 14653 serves as a crucial document for U.S. persons residing outside the United States who wish to participate in the Streamlined Foreign Offshore Procedures. This form is not used in isolation; several other documents are often required to complete the process. Below is a brief overview of six additional forms and documents that may accompany Form 14653, each playing a significant role in ensuring compliance with U.S. tax obligations.

Each of these documents plays a vital role in the Streamlined Foreign Offshore Procedures, providing the necessary context and information to facilitate compliance with U.S. tax laws. Careful attention to detail in completing these forms will help ensure a smoother process and reduce the likelihood of complications. It is essential for individuals to approach this process with diligence and clarity, as the implications of tax compliance are significant for personal and financial well-being.

Form 8854, the Initial and Annual Expatriation Statement, serves a similar purpose to Form 14653. Both forms are utilized by U.S. citizens or residents who are residing outside the United States and need to report their tax status. Form 8854 specifically addresses individuals who have expatriated and must certify their compliance with U.S. tax obligations for the five years preceding their expatriation. Just like Form 14653, it requires detailed information regarding income and tax liabilities, ensuring that expatriates are aware of their responsibilities under U.S. tax law.

Form 1040, the U.S. Individual Income Tax Return, is another document that parallels Form 14653. While Form 1040 is the standard tax return for U.S. citizens and residents, it can be relevant for those using Form 14653 when they are filing delinquent or amended returns. Both forms require taxpayers to disclose their income, deductions, and tax liabilities. However, Form 14653 specifically caters to individuals seeking relief under the Streamlined Foreign Offshore Procedures, making it distinct yet closely related to the general tax filing process.

Form 8938, the Statement of Specified Foreign Financial Assets, is also similar to Form 14653. Taxpayers must use Form 8938 to report their foreign financial assets if they meet certain thresholds. Like Form 14653, it is aimed at U.S. persons living abroad and helps ensure compliance with U.S. tax laws. Both forms emphasize the importance of disclosing foreign income and assets, highlighting the need for transparency in international financial matters.

Form 5471, the Information Return of U.S. Persons With Respect to Certain Foreign Corporations, shares similarities with Form 14653 in that it requires U.S. taxpayers to report foreign entities. This form is specifically for individuals who are officers, directors, or shareholders in certain foreign corporations. Both forms stress the importance of compliance and accurate reporting to avoid penalties, and they serve to help the IRS track foreign financial activities of U.S. taxpayers.

Form 8939, the Allocation of Increase in Basis for Property Acquired from a Decedent, can also be compared to Form 14653. While primarily focused on estate tax matters, both forms require detailed information about assets. For individuals who have inherited foreign assets, the reporting requirements can overlap with those outlined in Form 14653. Both forms underscore the necessity of accurately reporting financial information to the IRS, ensuring compliance with tax obligations.

Form 1040-X, the Amended U.S. Individual Income Tax Return, is another document that relates closely to Form 14653. When taxpayers need to correct errors on their original Form 1040, they utilize Form 1040-X. Similarly, Form 14653 allows individuals to amend their tax filings under the Streamlined Foreign Offshore Procedures. Both forms facilitate the correction of past tax reporting, emphasizing the importance of accurate and timely submissions to the IRS.

Form 8862, the Information to Claim Certain Refundable Credits After Disallowance, also bears similarities to Form 14653. This form is used by taxpayers who have previously had their claims for certain credits denied and wish to reapply. Like Form 14653, it requires detailed information about past tax filings and compliance. Both forms aim to ensure that taxpayers provide complete and accurate information to rectify prior issues with the IRS.

Form 8857, the Request for Innocent Spouse Relief, is relevant in cases where one spouse is seeking relief from joint tax liabilities. While Form 14653 focuses on compliance for those living abroad, it can also apply to joint filers who may have different reasons for their tax issues. Both forms require detailed narratives explaining the taxpayer's situation, ensuring that the IRS has a complete understanding of the circumstances surrounding the tax filings.

Lastly, Form 4506-T, the Request for Transcript of Tax Return, is similar in that it allows individuals to obtain their tax return information from the IRS. For those completing Form 14653, having access to past tax returns can be crucial for accurately reporting income and tax liabilities. Both forms underscore the importance of maintaining accurate records and ensuring compliance with U.S. tax laws, particularly for individuals with foreign financial interests.

Filling out Form 14653 can be a crucial step for U.S. persons residing outside the country who are seeking to comply with tax obligations. Here are some important dos and don’ts to keep in mind while completing this form:

By following these guidelines, you can help ensure a smoother process when submitting Form 14653. Taking the time to be thorough and honest will aid in your compliance with U.S. tax laws.

Form 14653 is an important document for U.S. persons residing outside the United States seeking to participate in the Streamlined Foreign Offshore Procedures. However, several misconceptions about this form can lead to confusion. Here are four common misunderstandings:

Many believe that simply filling out the form suffices. In reality, a thorough narrative statement explaining the reasons for failing to report income and file returns is required. Without this, the submission will be deemed incomplete.

This is incorrect. Both spouses must meet the non-residency requirements and provide individual reasons for their failure to comply. If their situations differ, those differences must be clearly documented.

While the streamlined procedures offer some relief, they do not guarantee protection against penalties. If the IRS discovers evidence of willfulness or fraud, it can lead to severe consequences, including civil and criminal penalties.

This is a critical error. Taxpayers must retain all records related to their income and foreign financial accounts for a specified period. This includes documentation for three years for tax returns and six years for FBARs. Failure to do so can result in complications if the IRS requests documentation later.

Filling out Form 14653 is an important step for U.S. persons living outside the United States who want to participate in the Streamlined Foreign Offshore Procedures. Here are key takeaways to keep in mind:

By keeping these takeaways in mind, you can navigate the complexities of Form 14653 more effectively and increase your chances of a successful submission.