The 1099-NEC form plays a crucial role in the world of taxes, specifically for reporting nonemployee compensation. This form is used primarily by businesses to report payments made to independent contractors or freelancers who have earned $600 or more in a calendar year. Unlike the W-2 form, which is issued to employees, the 1099-NEC does not withhold federal income tax, Social Security, or Medicare taxes. Recipients of this form must report the income on their tax returns, and it is essential for them to understand their tax obligations. The form includes various sections, such as the payer's and recipient's information, total compensation, and any taxes withheld. It's important to note that while Copy A of the form is available online for informational purposes, it must be ordered directly from the IRS for official use, as it needs to be scannable. Additionally, businesses can file this form electronically through the IRS Filing Information Returns Electronically (FIRE) system. Understanding the 1099-NEC is vital for both payers and recipients to ensure compliance and avoid potential penalties.

| Fact Name | Fact Description |

|---|---|

| Purpose | The 1099-NEC form reports nonemployee compensation paid to independent contractors. |

| Filing Requirement | Businesses must file this form if they pay an independent contractor $600 or more in a calendar year. |

| Copies | Copy A is for the IRS, while Copy B is for the recipient. Other copies exist for state tax purposes. |

| Scannability | Only the official printed version of Copy A is scannable. Downloaded versions cannot be filed. |

| Penalties | Filing unscannable forms may result in penalties from the IRS. |

| Electronic Filing | Forms can be filed electronically through the IRS FIRE system or AIR program. |

| State-Specific Forms | States may have their own forms for reporting nonemployee compensation. Check local regulations. |

| Tax Withholding | Federal income tax may not be withheld unless backup withholding applies. |

| Recipient's Responsibility | Recipients must report the income on their tax returns, even if taxes were not withheld. |

| IRS Resources | For more information, visit the IRS website and consult Publications 1141, 1167, and 1179. |

Filling out the 1099-NEC form is a straightforward process, but it requires attention to detail to ensure accuracy. This form is essential for reporting payments made to non-employees, such as independent contractors or freelancers. Once completed, the form must be submitted to the IRS and provided to the recipient of the payments.

Once the 1099-NEC form is filled out and submitted, it is crucial to keep copies for your records. Make sure to stay informed about any updates or changes to the filing process in future tax years.

What is the 1099-NEC form used for?

The 1099-NEC form is primarily used to report nonemployee compensation. If you are an independent contractor, freelancer, or self-employed individual, this form is essential for reporting income you received for services rendered, typically when you earned $600 or more during the year.

Who needs to file a 1099-NEC?

Businesses or individuals who pay nonemployees for services must file a 1099-NEC. This includes payments made to independent contractors, freelancers, and other nonemployee service providers. If you paid someone $600 or more in a calendar year, you are required to issue this form to them and file it with the IRS.

What information is included on the 1099-NEC?

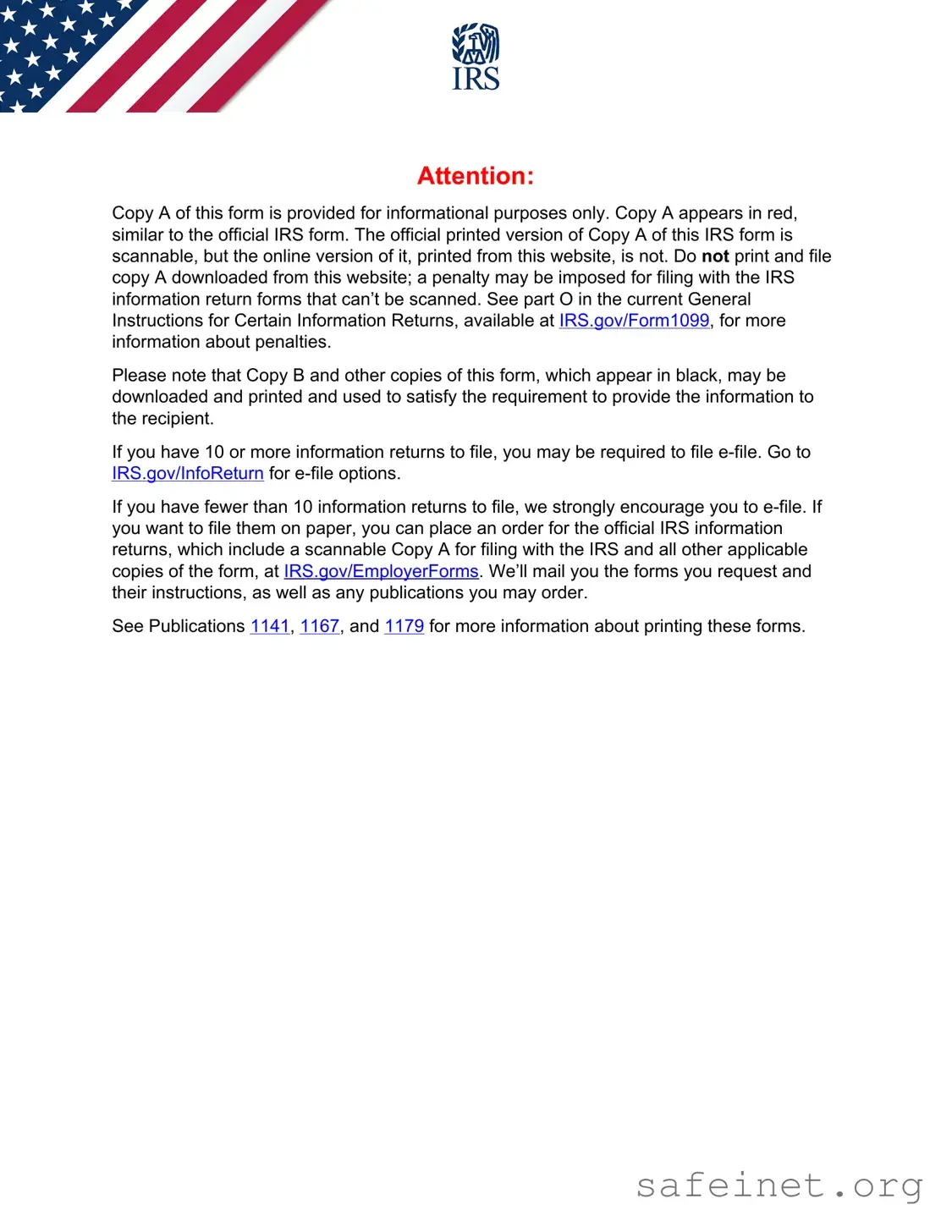

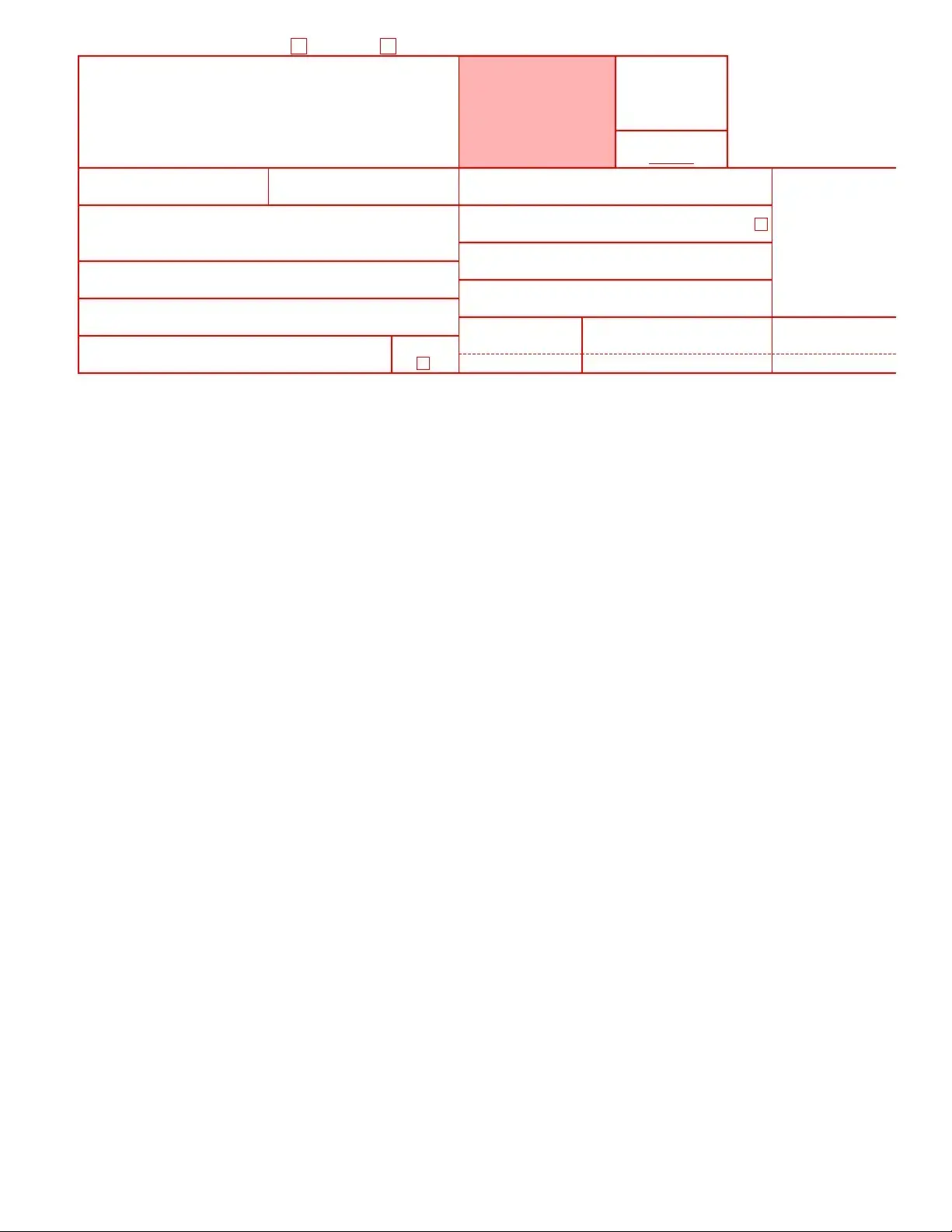

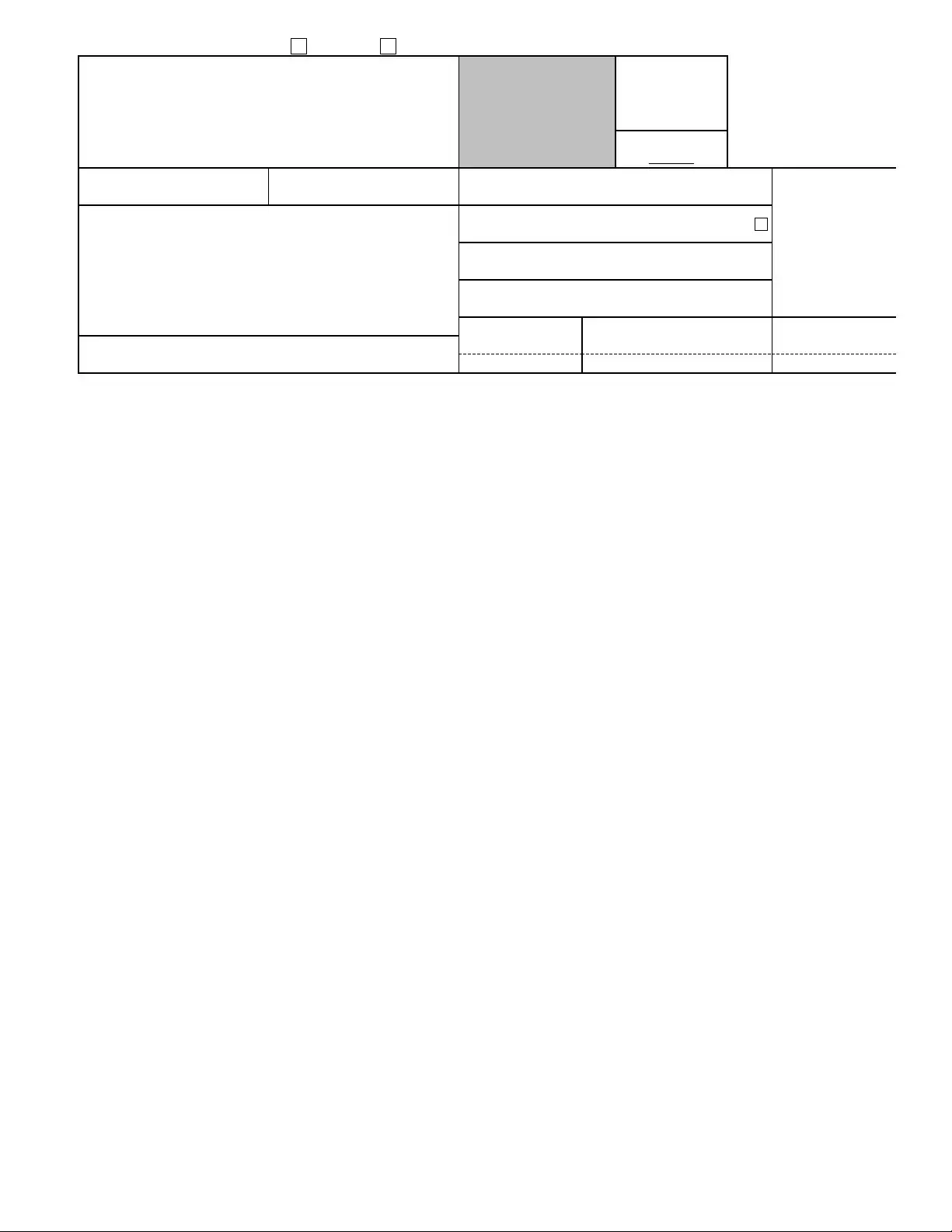

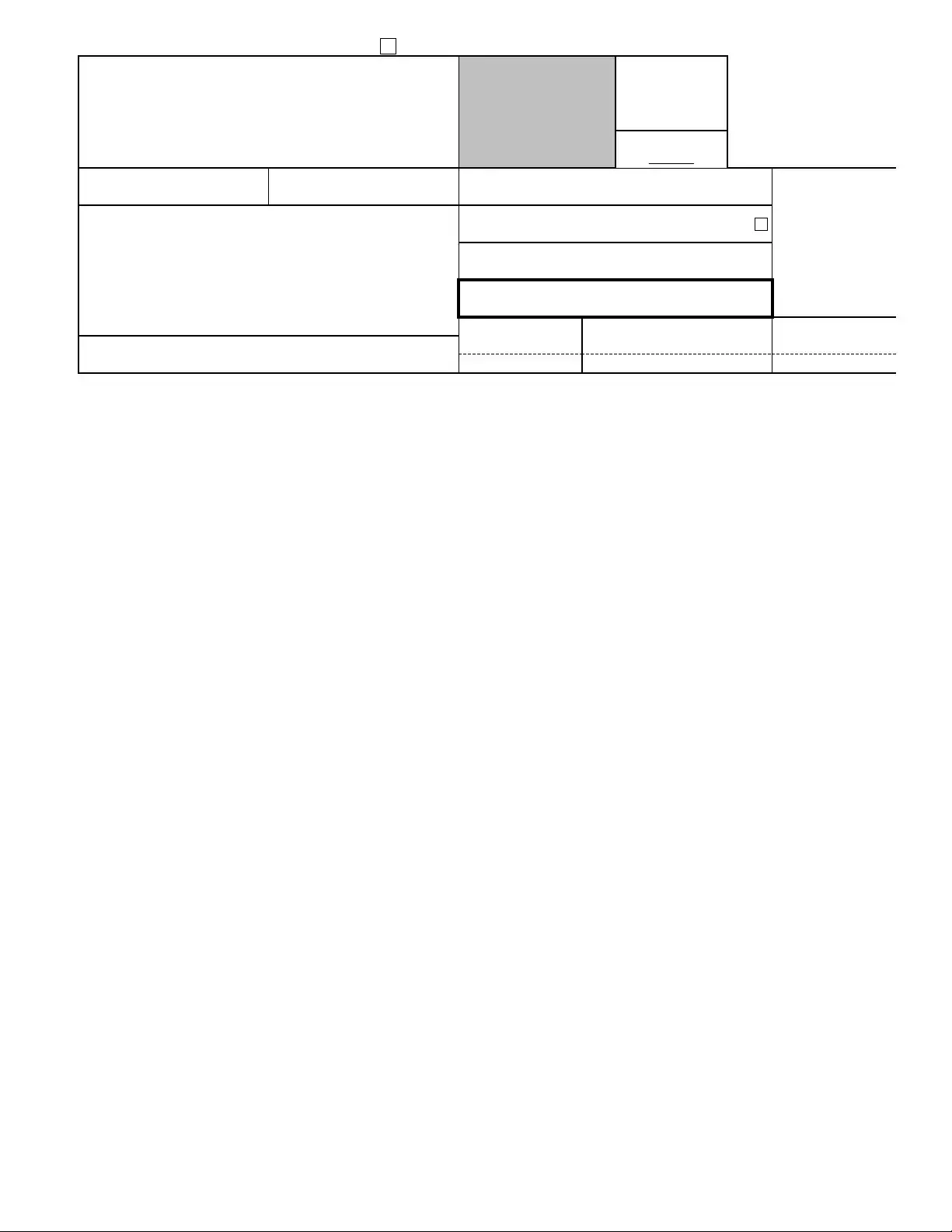

The 1099-NEC form includes several key pieces of information. This includes the payer's name, address, and taxpayer identification number (TIN), as well as the recipient's name, address, and TIN. The form also details the amount of nonemployee compensation paid, any federal income tax withheld, and state tax information if applicable.

How do I obtain a 1099-NEC form?

You can download and print copies of the 1099-NEC form from the IRS website, but be cautious. Only copies B and other forms in black can be printed for distribution. For official filings with the IRS, you must order the official printed version of Copy A, which is scannable. You can order these forms from the IRS website under the Employer and Information Returns section.

What should I do if I believe I am an employee but received a 1099-NEC?

If you received a 1099-NEC but believe you should be classified as an employee, it’s important to address this issue with the payer. If they do not correct the classification, you may need to report the income on your tax return as wages. Additionally, complete Form 8919 and attach it to your return to report any unreported income.

What happens if I file the wrong version of the 1099-NEC?

Filing the incorrect version of the 1099-NEC can result in penalties from the IRS. It is crucial to use the official scannable Copy A for filing with the IRS. If you use a downloaded version that is not scannable, you may face fines. Always ensure you are using the correct form as specified by the IRS guidelines.

Can I file the 1099-NEC electronically?

Yes, you can file the 1099-NEC electronically using the IRS Filing Information Returns Electronically (FIRE) system. This option is convenient and may help streamline the filing process. You can also check out the IRS Affordable Care Act Information Returns (AIR) program for electronic filing options.

What should I do if I notice an error on my 1099-NEC?

If you discover an error on your 1099-NEC, you should request a corrected form from the payer as soon as possible. The payer can issue a corrected 1099-NEC to ensure accurate reporting. It is important to address any discrepancies promptly to avoid issues with the IRS.

Incorrect Tax Identification Numbers (TINs): One of the most common mistakes is entering the wrong TIN for either the payer or the recipient. This can lead to significant delays and potential penalties. Always double-check the numbers for accuracy.

Using the Wrong Copy of the Form: Individuals often mistakenly print and file Copy A downloaded from the IRS website. This copy is not scannable and can result in penalties. Always use the official printed version of Copy A for filing with the IRS.

Omitting Required Information: Failing to complete all necessary fields can lead to issues. Ensure that all relevant information, such as the recipient's name, address, and compensation amount, is accurately filled out. Missing details can trigger audits or penalties.

Not Keeping Copies for Records: After filing, individuals sometimes neglect to keep copies of the submitted forms. It is crucial to retain copies of all filed 1099-NEC forms for your records. This documentation may be necessary for future reference or in case of an audit.

The 1099-NEC form is an important document used to report nonemployee compensation to the IRS. However, it is often accompanied by several other forms and documents that are essential for accurate tax reporting and compliance. Below is a list of these forms, each serving a specific purpose in the tax process.

Understanding these additional forms is crucial for proper tax reporting and compliance. Each document plays a role in ensuring that all income is accurately reported and that any necessary taxes are paid. Be proactive in gathering and completing these forms to avoid potential penalties or issues with the IRS.

The 1099-MISC form is similar to the 1099-NEC in that both are used to report income earned by individuals who are not classified as employees. The 1099-MISC form was traditionally the go-to document for reporting various types of income, including rents, royalties, and other non-employee compensation. However, starting in 2020, the IRS reintroduced the 1099-NEC specifically for reporting nonemployee compensation, which streamlined the process and made it clearer for taxpayers. Both forms require the payer to provide detailed information about the recipient and the amount paid, ensuring that the IRS receives accurate income data for tax purposes.

The 1099-K form also shares similarities with the 1099-NEC, as it is used to report payment transactions made through third-party networks. This form is commonly issued by payment processors when a business receives payments exceeding $20,000 and more than 200 transactions in a calendar year. Like the 1099-NEC, the 1099-K helps the IRS track income that might otherwise go unreported. While the 1099-NEC focuses on nonemployee compensation, the 1099-K covers a broader range of payment types, making it essential for businesses that operate in the gig economy or online marketplaces.

The W-2 form is another document that bears resemblance to the 1099-NEC, but it serves a different purpose. The W-2 is used to report wages and salaries paid to employees, including withheld taxes. While the 1099-NEC is for independent contractors and freelancers, the W-2 is specifically for individuals classified as employees. Both forms require the payer to report the recipient's taxpayer identification number (TIN) and the total amount paid, ensuring that the IRS can track income accurately. The distinction lies in the employment classification, which affects tax withholding and reporting requirements.

Finally, the 1099-INT form is similar to the 1099-NEC in that it is also used to report income to the IRS. However, the 1099-INT is specifically for reporting interest income earned by individuals from banks, financial institutions, or other entities. While the 1099-NEC reports nonemployee compensation, the 1099-INT focuses solely on interest payments. Both forms require the payer to provide essential information about the recipient and the amount paid, ensuring compliance with tax regulations. Understanding these distinctions is crucial for accurate tax reporting and compliance.

When filling out the 1099-NEC form, it is important to follow certain guidelines to ensure accuracy and compliance. Below is a list of things to do and avoid.

Understanding the 1099-NEC form can be challenging, and several misconceptions often arise. Here are nine common misunderstandings about this important tax document:

By clarifying these misconceptions, individuals can better navigate their tax responsibilities and ensure compliance with IRS regulations.

Filling out and using the 1099-NEC form is essential for reporting nonemployee compensation. Here are some key takeaways to keep in mind: