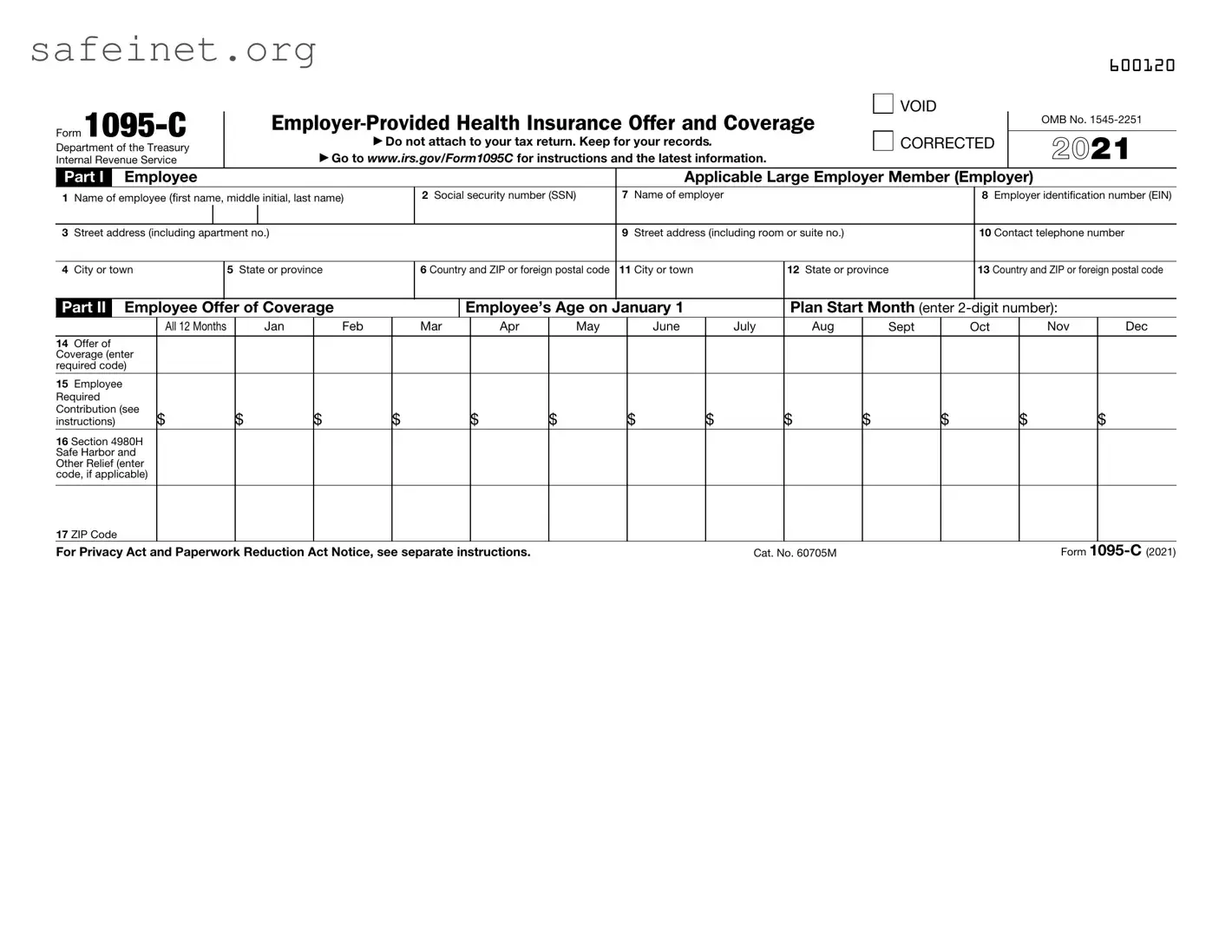

The 1095-C form serves a crucial role in the healthcare landscape for both employers and employees in the United States. This form is issued by Applicable Large Employers, which are businesses that employ 50 or more full-time employees. The primary purpose of the 1095-C is to provide essential details regarding health insurance coverage offered to the employee, their spouses, and dependents. It contains specific information about the type of coverage available, any required contributions from the employee, and codes indicating the nature of the coverage. Additionally, the 1095-C includes sections that identify both the employee and employer, listing Social Security numbers and employer identification numbers for accuracy and record-keeping. For employees, this form is vital when applying for premium tax credits related to health coverage obtained through the Health Insurance Marketplace. If an employee has multiple jobs within the year, they may receive multiple 1095-C forms, each reflecting coverage from different employers. Information about family members may also be included if the employer provides a self-insured health plan. Overall, understanding the 1095-C can help individuals ensure they meet healthcare obligations and leverage available credits while navigating their healthcare options.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

600120 |

Form |

|

|

|

|

▶ |

|

|

|

|

|

|

|

|

VOID |

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

OMB No. |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Department of the Treasury |

|

|

|

|

|

Do not attach to your tax return. Keep for your records. |

|

|

CORRECTED |

|

2021 |

|||||||||||||

Internal Revenue Service |

|

|

|

▶ Go to www.irs.gov/Form1095C for instructions and the latest information. |

|

|

|

|

|

|

||||||||||||||

Part I |

|

Employee |

|

|

|

|

|

|

|

|

|

|

Applicable Large Employer Member (Employer) |

|

|

|||||||||

1 |

Name of employee (first name, middle initial, last name) |

|

|

2 Social security number (SSN) |

7 Name of employer |

|

|

|

|

8 Employer identification number (EIN) |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

3 |

Street address (including apartment no.) |

|

|

|

|

|

|

9 Street address (including room or suite no.) |

|

|

|

10 Contact telephone number |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

4 |

City or town |

|

|

|

5 State or province |

|

|

6 Country and ZIP or foreign postal code |

11 City or town |

12 State or province |

|

13 Country and ZIP or foreign postal code |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

Part II |

Employee Offer of Coverage |

|

|

|

Employee’s Age on January 1 |

|

Plan Start Month (enter |

|

||||||||||||||||

|

|

|

|

All 12 Months |

|

Jan |

Feb |

|

|

Mar |

Apr |

May |

June |

July |

Aug |

|

Sept |

Oct |

Nov |

Dec |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 |

Offer of |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Coverage (enter |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

required code) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

15 |

Employee |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Required |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Contribution (see |

$ |

|

|

$ |

|

$ |

|

$ |

|

$ |

$ |

$ |

$ |

$ |

$ |

$ |

$ |

|

$ |

|||||

instructions) |

|

|

|

|

|

|

|

|||||||||||||||||

16 Section 4980H Safe Harbor and Other Relief (enter code, if applicable)

17 ZIP Code |

|

Form |

For Privacy Act and Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 60705M |

600220

Form |

Page 2 |

Instructions for Recipient

You are receiving this Form

In addition, if you, or any other individual who is offered health coverage because of their relationship to you (referred to here as family members), enrolled in your employer’s health plan and that plan is a type of plan referred to as a

If your employer provided you or a family member health coverage through an insured health plan or in another manner, you may receive information about the coverage separately on Form

Employers are required to furnish Form

Additional information. For additional information about the tax provisions of the Affordable Care Act (ACA), including the individual shared responsibility provisions, the premium tax credit, and the employer shared responsibility provisions, visit www.irs.gov/ACA or call the IRS Healthcare Hotline for ACA questions

Part I. Employee

Lines

Line 2. This is your social security number (SSN). For your protection, this form may show only the last four digits of your SSN. However, the employer is required to report your complete SSN to the IRS.

Part I. Applicable Large Employer Member (Employer)

Lines

Line 10. This line includes a telephone number for the person whom you may call if you have questions about the information reported on the form or to report errors in the information on the form and ask that they be corrected.

Part II. Employer Offer of Coverage, Lines

Line 14. The codes listed below for line 14 describe the coverage that your employer offered to you and your spouse and dependent(s), if any. (If you received an offer of coverage through a multiemployer plan due to your membership in a union, that offer may not be shown on line 14.) The information on line 14 relates to eligibility for coverage subsidized by the premium tax credit for you, your spouse, and dependent(s). For more information about the premium tax credit, see Pub. 974.

1A. Minimum essential coverage providing minimum value offered to you with an employee required contribution for

1B. Minimum essential coverage providing minimum value offered to you and minimum essential coverage NOT offered to your spouse or dependent(s).

1C. Minimum essential coverage providing minimum value offered to you and minimum essential coverage offered to your dependent(s) but NOT your spouse.

1D. Minimum essential coverage providing minimum value offered to you and minimum essential coverage offered to your spouse but NOT your dependent(s).

1E. Minimum essential coverage providing minimum value offered to you and minimum essential coverage offered to your dependent(s) and spouse.

1F. Minimum essential coverage NOT providing minimum value offered to you, or you and your spouse or dependent(s), or you, your spouse, and dependent(s).

1G. You were NOT a

1H. No offer of coverage (you were NOT offered any health coverage or you were offered coverage that is NOT minimum essential coverage).

1I. Reserved for future use.

1J. Minimum essential coverage providing minimum value offered to you; minimum essential coverage conditionally offered to your spouse; and minimum essential coverage NOT offered to your dependent(s).

1K. Minimum essential coverage providing minimum value offered to you; minimum essential coverage conditionally offered to your spouse; and minimum essential coverage offered to your dependent(s).

1L. Individual coverage health reimbursement arrangement (HRA) offered to you only with affordability determined by using employee’s primary residence ZIP code.

1M. Individual coverage HRA offered to you and dependent(s) (not spouse) with affordability determined by using employee’s primary residence ZIP code.

1N. Individual coverage HRA offered to you, spouse, and dependent(s) with affordability determined by using employee’s primary residence ZIP code.

1O. Individual coverage HRA offered to you only using the employee’s primary employment site ZIP code affordability safe harbor.

1P. Individual coverage HRA offered to you and dependent(s) (not spouse) using the employee’s primary employment site ZIP code affordability safe harbor.

1Q. Individual coverage HRA offered to you, spouse, and dependent(s) using the employee’s primary employment site ZIP code affordability safe harbor.

1R. Individual coverage HRA that is NOT affordable offered to you; employee and spouse or dependent(s); or employee, spouse, and dependents.

1S. Individual coverage HRA offered to an individual who was not a

1T. Individual coverage HRA offered to employee and spouse (no dependents) with affordability determined using employee’s primary residence ZIP code.

1U. Individual coverage HRA offered to employee and spouse (no dependents) using employee’s primary employment site ZIP code affordability safe harbor.

1V. Reserved for future use.

1W. Reserved for future use.

1X. Reserved for future use.

1Y. Reserved for future use.

1Z. Reserved for future use.

(Continued on page 4)

600320

Form |

Page 3 |

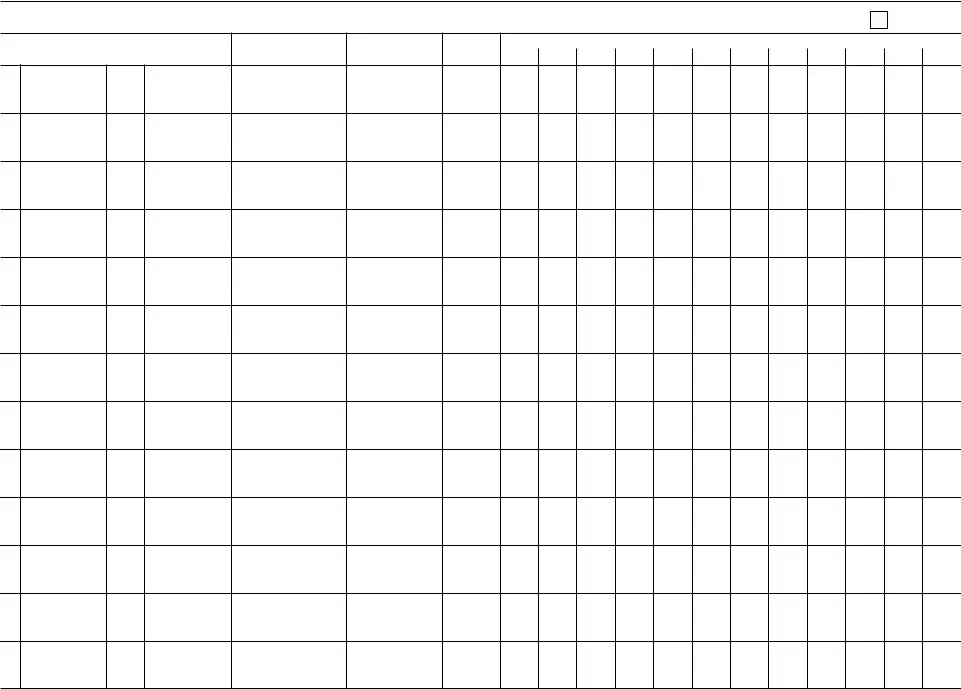

Part III Covered Individuals

If Employer provided

18

19

20

21

22

23

24

25

26

27

28

29

30

(a) Name of covered individual(s) |

(b) SSN or other TIN (c) DOB (if SSN or other |

(d) Covered |

|

|

|

|

|

|

|

|

(e) Months of coverage |

|

|

|

|

|

|

||||||||||||

First name, middle initial, last name |

TIN is not available) |

all 12 months |

|

Jan |

Feb |

Mar |

Apr |

May June July |

Aug Sept |

Oct |

Nov |

Dec |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form

600420

Form |

Page 4 |

Instructions for Recipient (continued)

Line 15. This line reports the employee required contribution, which is the monthly cost to you for the lowest cost

Line 16. This code provides the IRS information to administer the employer shared responsibility provisions. Other than a code 2C, which reflects your enrollment in your employer’s coverage, none of this information affects your eligibility for the premium tax credit. For more information about the employer shared responsibility provisions, visit IRS.gov.

Line 17. This line reports the applicable ZIP code your employer used for determining affordability if you were offered an individual coverage HRA. If code 1L, 1M, 1N, or 1T was used on line 14, this will be your primary residence location. If code 1O, 1P, 1Q, or 1U was used on line 14, this will be your primary employment site. For more information about individual coverage HRAs, visit IRS.gov.

Part III. Covered Individuals, Lines

Part III reports the name, SSN (or TIN for covered individuals other than the employee listed in Part I), and coverage information about each individual (including any

| Fact Name | Detail |

|---|---|

| Purpose of Form | The 1095-C form is used to report information about health insurance offered to employees by applicable large employers as part of the Affordable Care Act (ACA). |

| Applicable Large Employers | Only employers with 50 or more full-time employees or equivalents are required to furnish the 1095-C form. |

| Employee Information | The form contains detailed employee information, including name, Social Security number (SSN), and contact information. |

| Coverage Offer Reporting | Part II of the form details the coverage offered, including monthly employee contribution amounts and availability codes to indicate coverage status. |

| Self-Insured Plans | If a self-insured plan is offered, Part III lists covered individuals like family members and provides their coverage details. |

| Record Keeping Requirement | Employees should keep the 1095-C for their records, though it does not need to be attached to tax returns. |

| State-Specific Forms | Some states may have their governing laws requiring additional forms, such as Massachusetts (M.G.L c. 111M) or New Jersey (N.J.S.A. 54:50-48). |

After gathering the necessary information, you are ready to complete Form 1095-C. This form provides essential details about the health coverage offered by your employer. Follow these steps carefully to ensure accurate completion.

Once you have filled out all necessary sections, review the form for accuracy. Keep a copy for your records, as you do not need to submit it with your tax return, but maintaining documentation is advisable.

What is Form 1095-C?

Form 1095-C is the Employer-Provided Health Insurance Offer and Coverage form. Employers, specifically Applicable Large Employers (ALEs), are required to send this form to employees. It provides information about the health insurance coverage offered to the employee, their spouse, and dependents. This form is important for tax purposes and helps individuals understand their health coverage options under the Affordable Care Act (ACA).

Who receives Form 1095-C?

Form 1095-C is sent to employees of Applicable Large Employers, which are those with 50 or more full-time employees. If an employee worked for multiple ALEs during the year, they may receive more than one Form 1095-C, with each form reflecting coverage from a different employer.

Do I need to attach Form 1095-C to my tax return?

No, Form 1095-C should not be attached to your tax return. Instead, it is intended for your records. You should keep it in a safe place as you may need to refer to it when filing your taxes or if you apply for health coverage through the Health Insurance Marketplace.

What information is included in Form 1095-C?

The form includes details such as your name, Social Security Number (SSN), employer's information, the health coverage offered to you, the employee required contribution for coverage, and any relevant codes indicating which types of coverage were offered to you, your spouse, and dependents.

What should I do if I find an error on my Form 1095-C?

If you notice any discrepancies or errors on your Form 1095-C, you should contact your employer directly. The employer is responsible for correcting and reporting any accurate information to the IRS.

What is the difference between Form 1095-C and Form 1095-B?

Form 1095-C is issued by Applicable Large Employers detailing the health coverage they offered to employees. In contrast, Form 1095-B is typically provided by other types of health coverage providers, such as insurance companies or government programs, and it reports the health coverage that individuals received. Both forms provide essential information for tax filing but come from different sources.

What if I did not receive Form 1095-C?

If you believe you should have received a Form 1095-C from your employer but did not, it is advisable to reach out to your employer’s human resources or payroll department. If the employer is an Applicable Large Employer and you worked there during the filing year, they are obligated to provide this form.

How is the employee required contribution on Form 1095-C determined?

The employee required contribution is the monthly cost for the least expensive self-only minimum essential coverage offered. It may differ from the actual amount you paid if you selected a more comprehensive or family plan. The specifics, such as the determined costs, will be reported in Part II of the form.

What does the code in Line 14 of Form 1095-C signify?

Line 14 contains codes that describe the type of health insurance coverage your employer offered. These codes help determine eligibility for the premium tax credit, should you wish to claim it when filing taxes. Understanding these codes is essential for accurately filing your taxes.

Can my family members receive Form 1095-C?

Form 1095-C is provided only to the employee; however, if the employee's family members were covered under a self-insured plan in which the employee participated, the employee can provide copies to those family members upon request for their records. Each family member covered under the plan should request a copy as needed.

Incorrectly Filling Out Personal Information: It's crucial to enter the full and correct name, including any middle initials. Any variations or omissions in your name can lead to confusion in identification.

Leaving Out the Social Security Number: Ensure you include the entire Social Security Number (SSN). The IRS needs this complete number, even if the form only shows partial digits for privacy reasons.

Ignoring Employer Details: Part I requires accurate information about your employer. Missing or incorrect details, like the Employer Identification Number (EIN), can cause issues during processing.

Choosing Incorrect Coverage Codes: Line 14 must have the correct code that reflects the coverage offered. Misidentifying the coverage type can result in reporting errors.

Neglecting to Include All Covered Individuals: In Part III, all covered individuals must be listed. Omitting a family member who received coverage can create gaps in reported information.

Forgetting to Report Employee Contribution: Make sure to list the correct amount for the Employee Required Contribution (line 15). Neglecting this can affect tax credits and liabilities.

Using Outdated or Incorrect Codes: Codes change over time, so it’s essential to have the most current information when filling out Line 16 and other sections.

Failing to Double-Check for Errors: Errors can easily slip through. Always review your entries before submitting. A small mistake can cause significant complications later.

Not Keeping a Copy: Keep a copy of the completed Form 1095-C for your records. This documentation may be necessary for future tax purposes.

Alongside Form 1095-C, several other documents play a crucial role in health coverage reporting and tax compliance. Each of these forms provides important details regarding health insurance coverage and can be essential for both employees and employers during tax season.

Understanding these forms helps individuals navigate the complexities of health insurance reporting and ensures compliance with taxation requirements. Keeping thorough records of all relevant documents is vital to avoid any issues when filing taxes.

The Form 1095-C is an essential document when it comes to understanding your health insurance coverage area. One document that bears similarities is the Form 1095-A, the Health Insurance Marketplace Statement. This form is issued to individuals who enroll in a qualified health plan through the Health Insurance Marketplace. Like the 1095-C, the 1095-A provides information regarding your health coverage for the year, including details relevant for claiming premium tax credits. Both forms require accurate reporting and can significantly impact tax calculations connected to health care provisions established by the Affordable Care Act (ACA).

Another document that closely resembles the Form 1095-C is Form 1095-B, which reports health coverage information for individuals enrolled in certain types of health plans, typically smaller group plans or those provided by government programs. Like the 1095-C, Form 1095-B serves the purpose of confirming minimum essential coverage offered to individuals and their dependents. However, unlike Form 1095-C that is specifically for applicable large employers, Form 1095-B is generally issued by insurance providers and thus provides a different perspective on your coverage.

Next is the Form W-2, the Wage and Tax Statement, which is commonly associated with salary and income reporting. Both the W-2 and 1095-C provide an overview of the health benefits related to employment. The W-2 includes a box indicating whether health coverage was provided, whereas the 1095-C delves deeper into the nature of that coverage, making it a useful complement when reviewing overall tax documents.

Additionally, Form 1098 is pertinent when discussing educational expenses and student loan interest. While this document does not relate directly to healthcare like the 1095-C, it is similar in that it provides information necessary for tax filing. It itemizes payments made towards student loans and can also affect tax liabilities, similar to how the 1095-C influences your tax credit eligibility tied to health insurance coverage.

The Form 8862, which is used to claim the Earned Income Tax Credit (EITC) after disallowance, also can be seen in a similar light. Although the content differs significantly, both forms play a part in ensuring compliance with tax laws and regulations. The 8862 is called upon following EITC claim issues while the 1095-C acts as a verification for the insurance coverage aspect previously discussed, illustrating how critical documentation is in the realm of tax benefits and credits.

Form 1040, the individual income tax return, is another document that aligns with the characteristics of the 1095-C. Both forms are crucial for accurately filing taxes and can significantly impact tax refunds or liabilities. While the 1040 serves as the primary tax form for individuals, the 1095-C adds depth by specifically focusing on health insurance coverage, making them essential companions when preparing your tax filing.

Another key form in this context is the Schedule A, which is used for itemizing deductions. Although primarily for reporting itemized tax deductions, it mirrors the intent of the 1095-C in its foundational role of shaping the taxpayer's financial picture. Both aim to offer a clearer understanding of financial obligations and benefits the individual has, be it through healthcare coverage or deductible expenses in a given tax year.

Last but not least is the Form 8962, which is utilized to claim the Premium Tax Credit. This document directly relates to Form 1095-C as it helps establish eligibility for assistance based on coverage offered. When you're applying for the credit, the information from the 1095-C—especially the employer’s offer of coverage—becomes vital. Thus, both forms work together to provide necessary data that guide tax benefits associated with health insurance.

When filling out the 1095-C form, here are some important dos and don'ts to keep in mind:

Understanding the 1095-C form can be challenging, and there are several misconceptions about it. Here are ten common misconceptions clarified for better comprehension.

Being aware of these misconceptions can help navigate health coverage and tax implications more effectively. Always consult with a tax professional for personalized advice.

Understanding the 1095-C form is essential for both employees and employers, especially when it comes to health insurance coverage. Here are four key takeaways about filling out and using this form:

By being aware of these points, you can approach the 1095-C form with confidence and ensure you’re making informed decisions about your health coverage.